Global: More stable growth, but still fragile

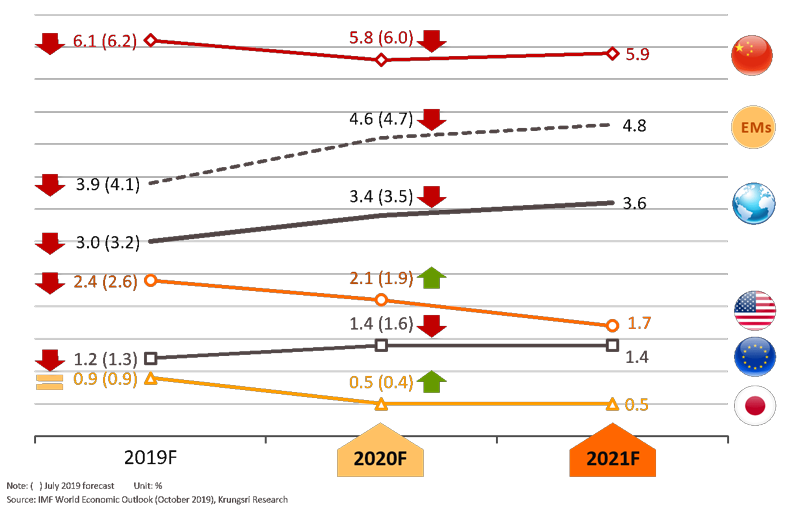

Global growth: Modest recovery amid headwinds after posting weakest growth since financial crisis

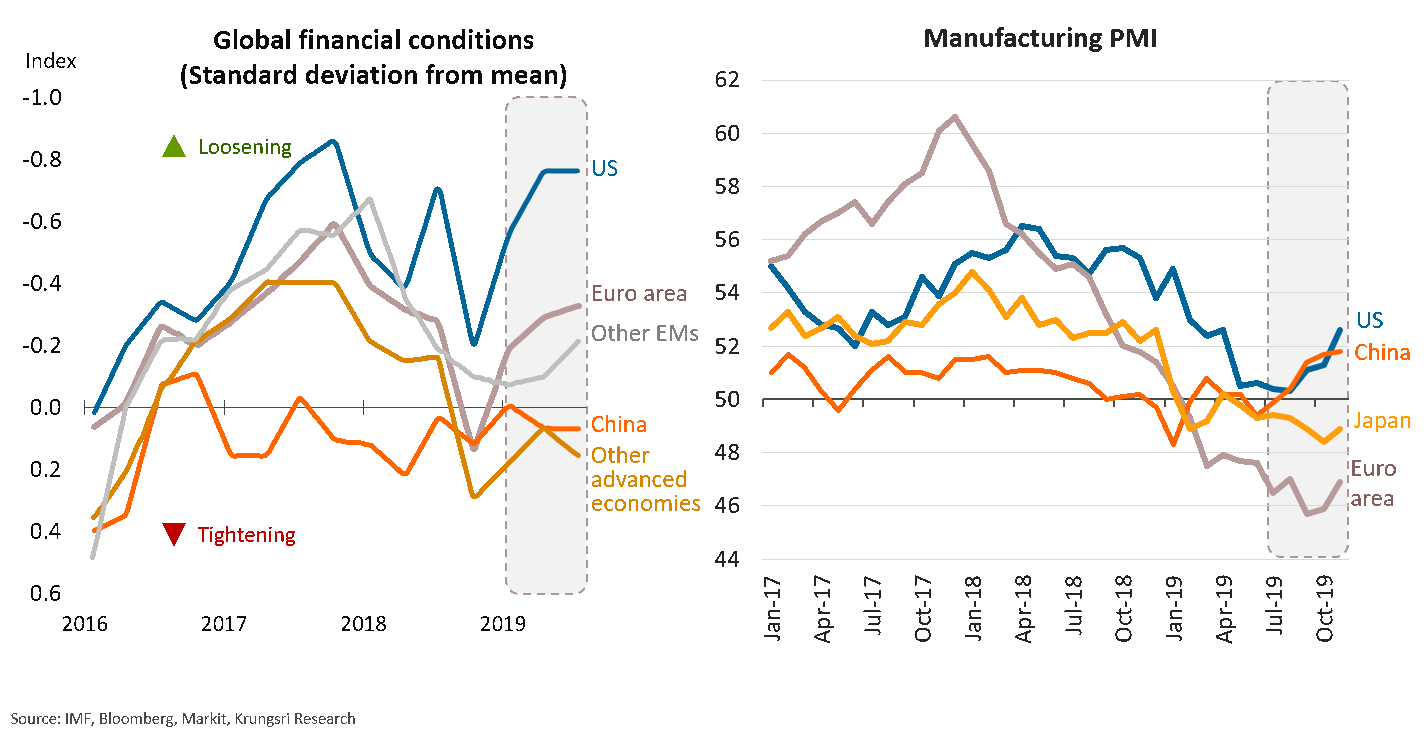

Easing financial conditions will limit downside risks; global manufacturing is recovering

Falling interest rates have helped to ease financial conditions in advanced economies since mid-2019, according to the IMF. In the US, financial conditions remain more accommodative than before. Conditions are marginally tighter in China but have generally eased in major emerging markets (excluding China). Easing financial conditions will limit near-term downside risks. Against the backdrop of more relaxed monetary policies worldwide and easing trade tensions, cyclical headwinds are easing and there are signs of a recovery in the manufacturing sector.

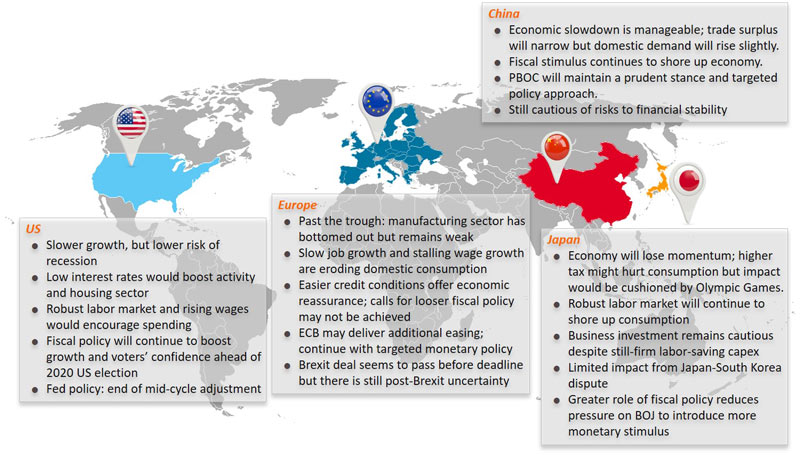

US: Slower growth, but lower risk of recession and consumption is recovering

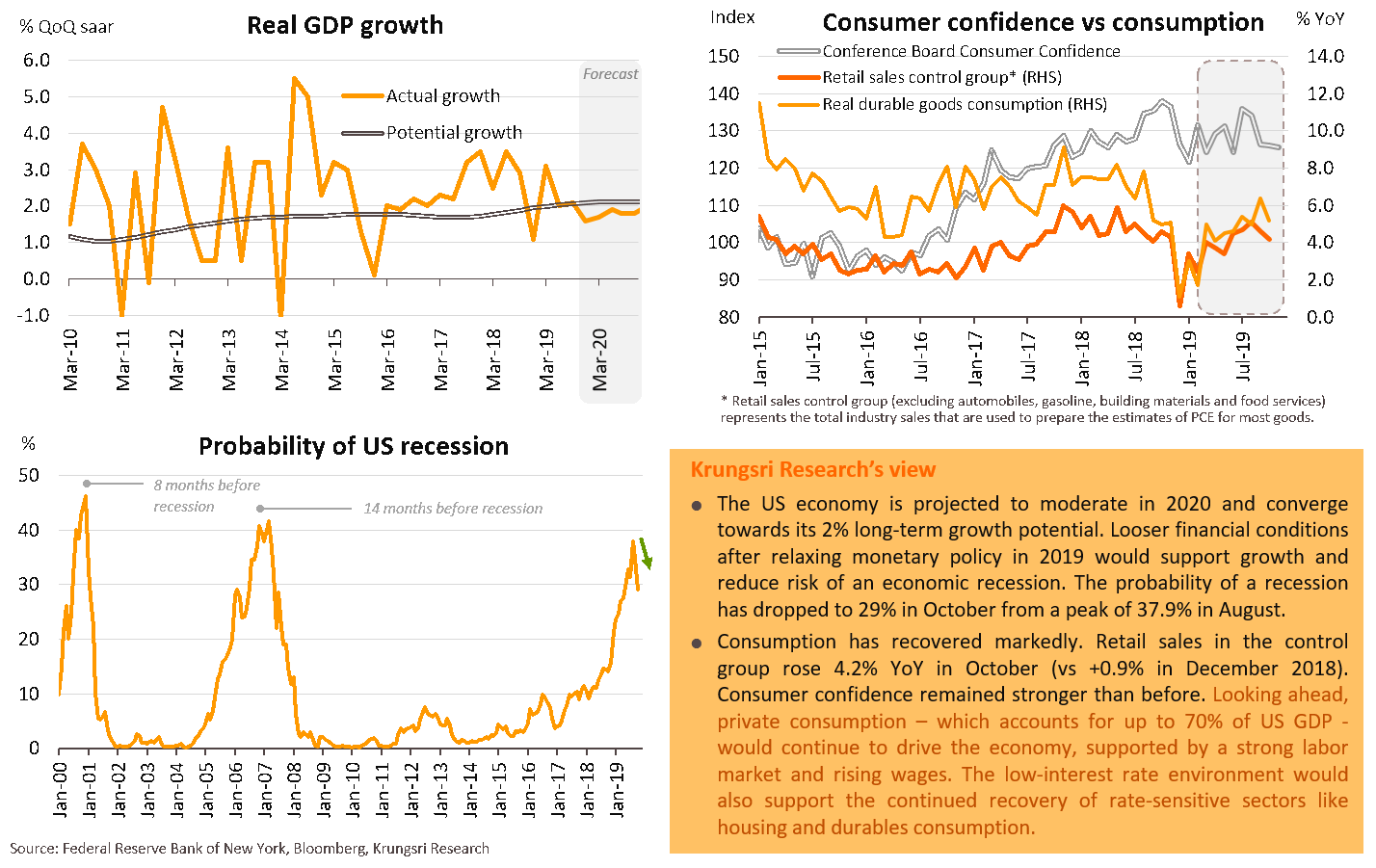

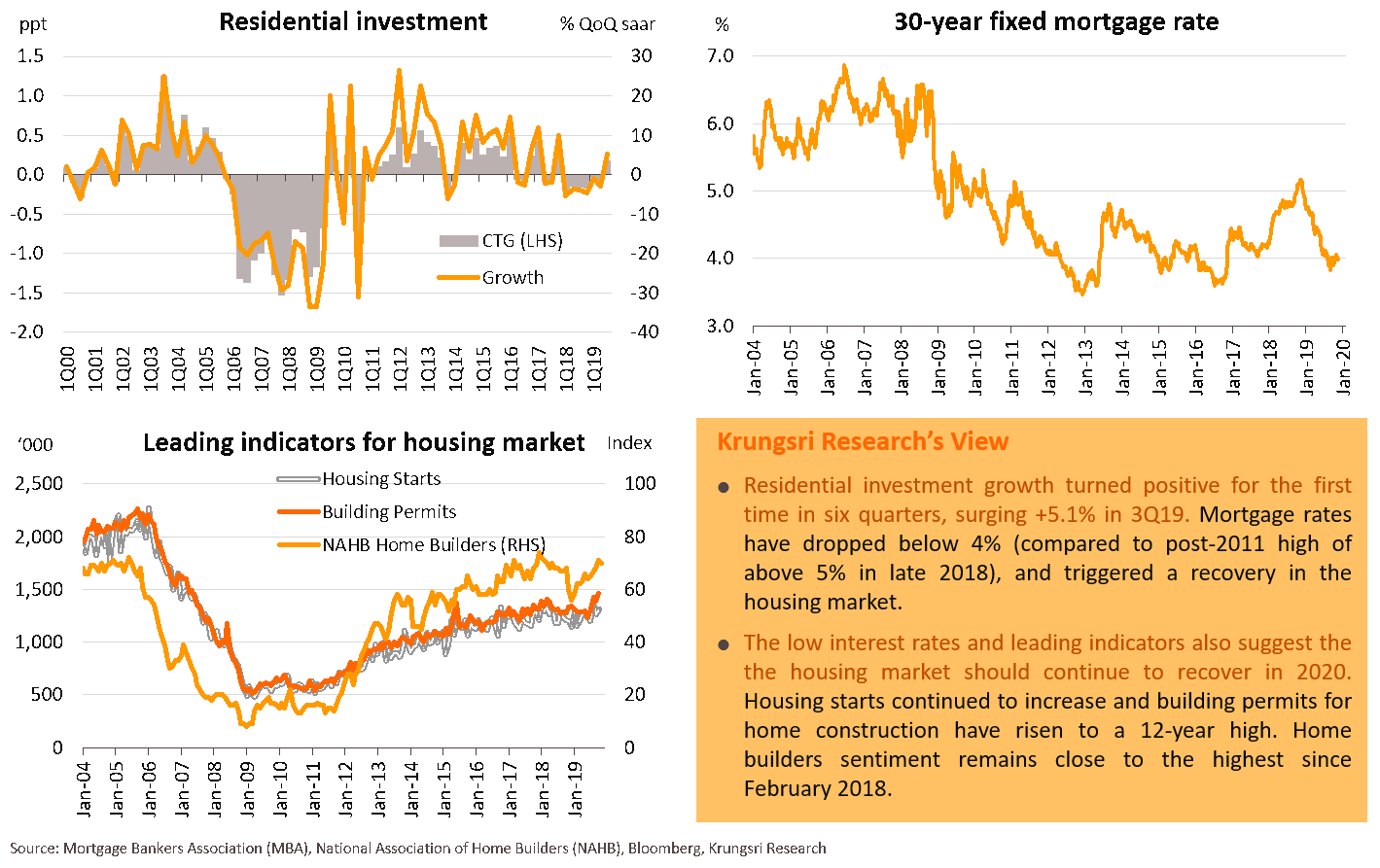

Recovering housing market is a tailwind as low interest rates would boost activity and home builders' sentiment

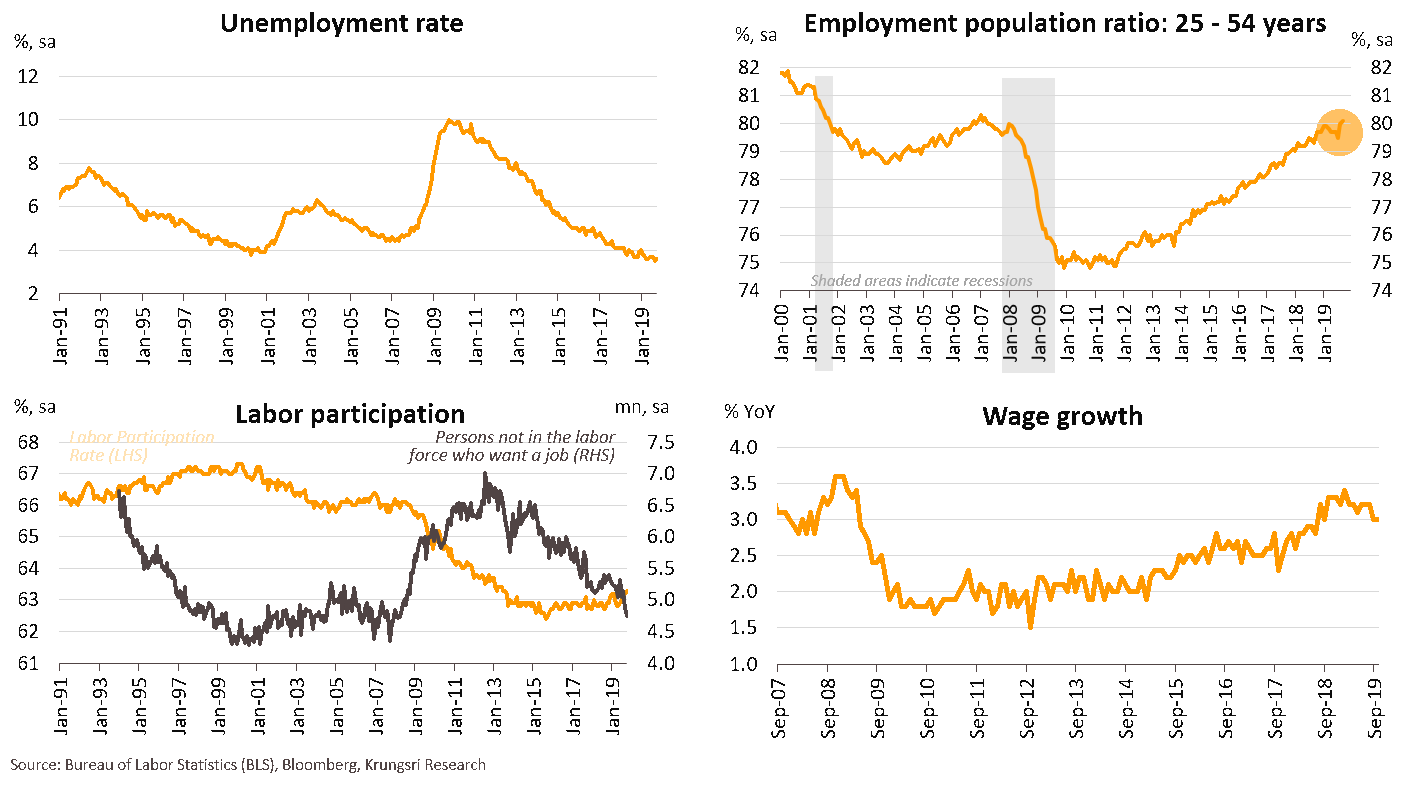

Robust labor market and rising wages would encourage spending; room for labor

Unemployment rate remains near a 50-year low and there is still room for the labor market to strengthen. The broader prime-age employment to population ratio suggests labor market conditions are not as tight as in the past decade. Labor participation rate remains low and there is no sign it will return to pre-crisis levels within the next few years. In addition, wage growth has accelerated gradually in recent years to close to 3%. The robust labor market coupled with rising wages will continue to encourage private consumption and drive overall growth.

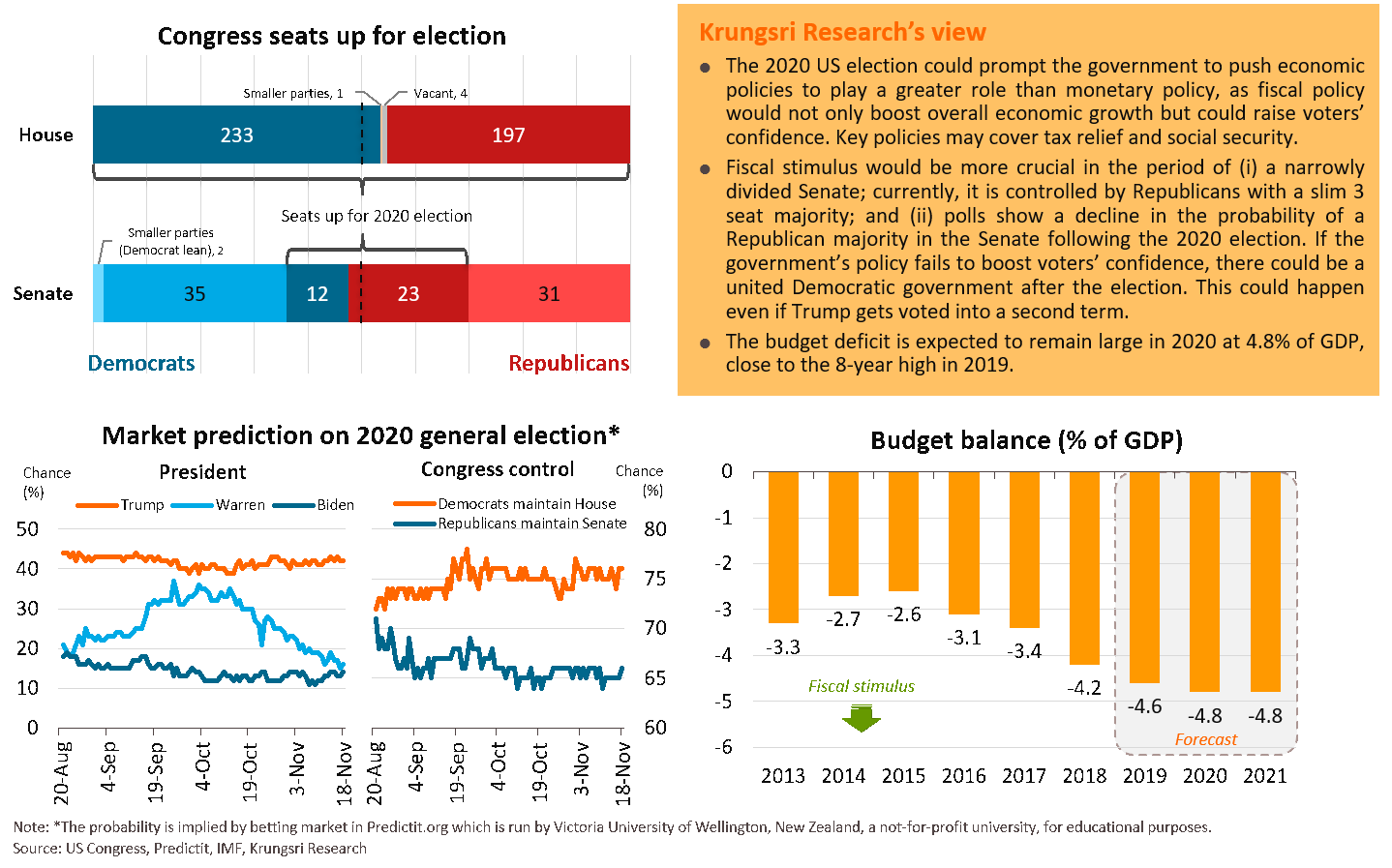

Fiscal policy will continue to boost growth and voters’ confidence ahead of 2020 US election

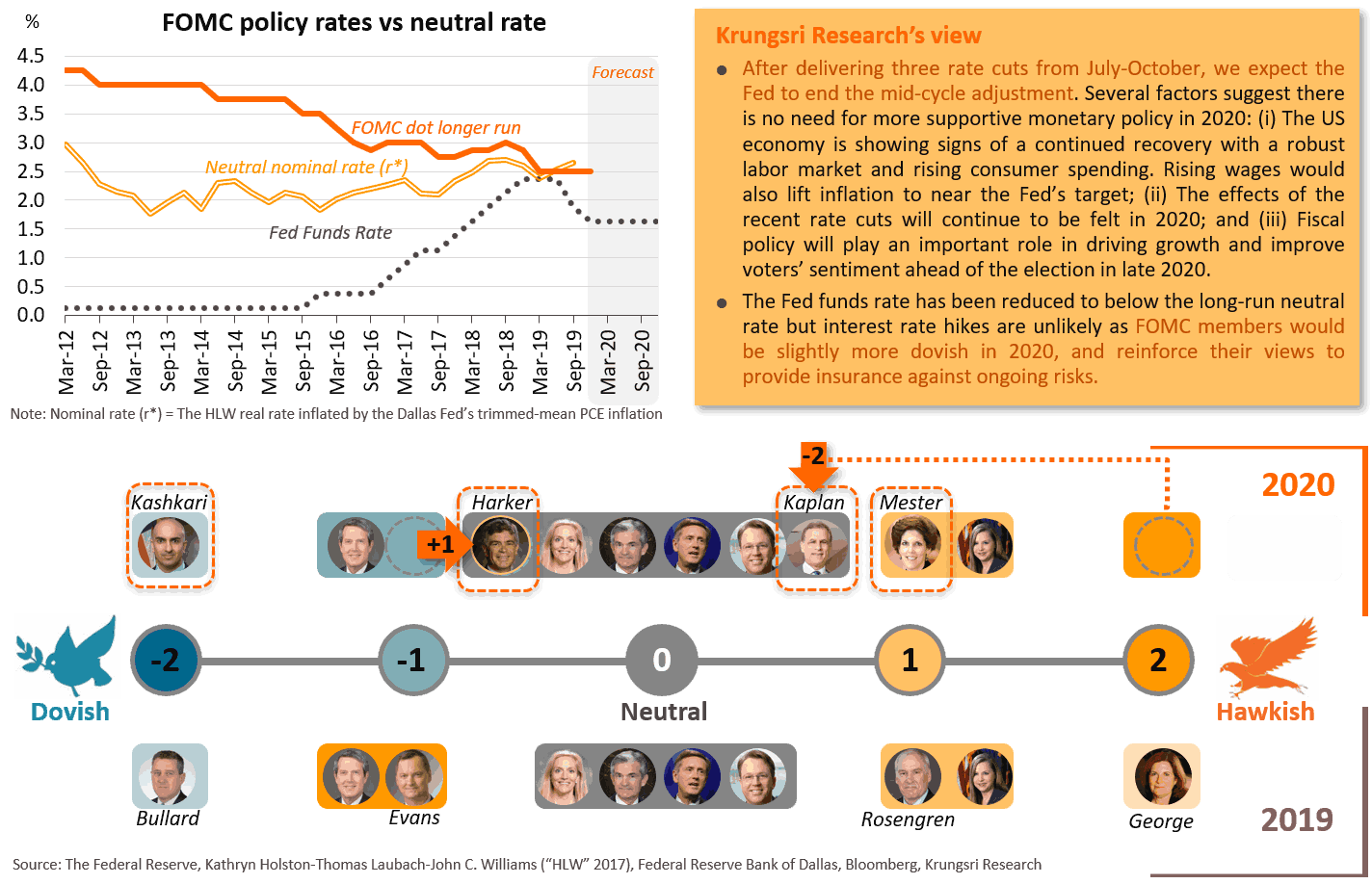

Fed policy: End of mid-cycle adjustment

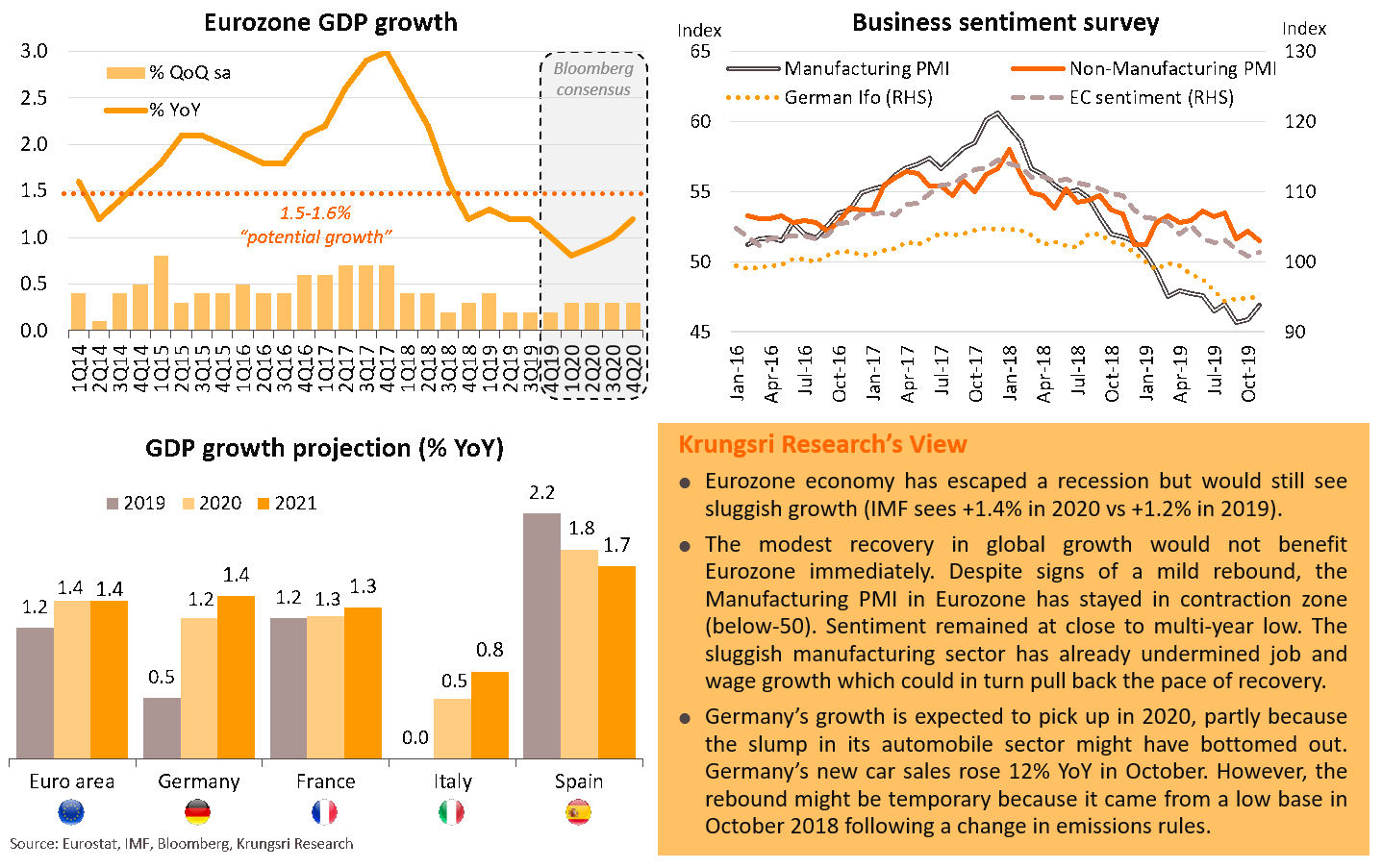

Europe: Past the trough; manufacturing sector has bottomed out but remains weak

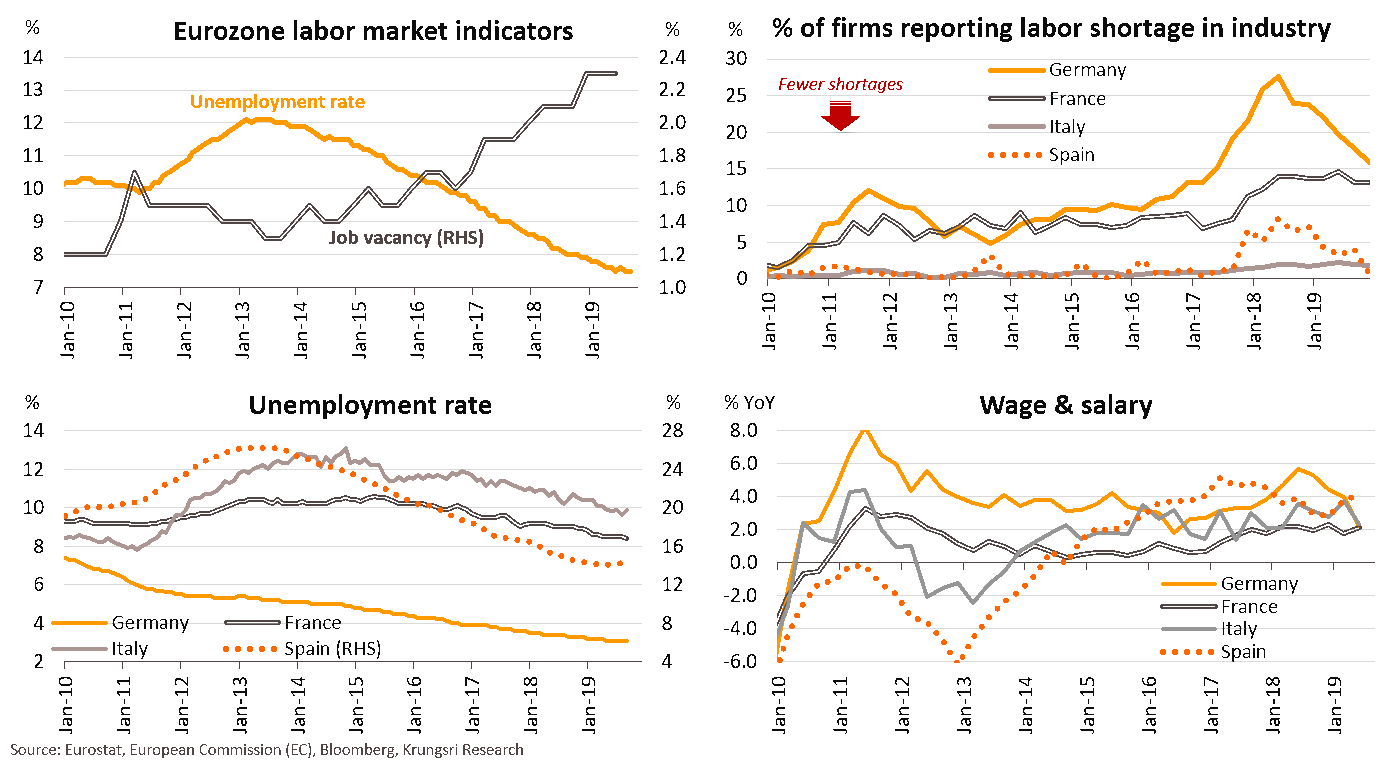

Slow job growth and stalling wage growth are eroding resilient domestic consumption

Although Eurozone’s employment rate is at its highest since the survey began in 2004, the unemployment rate has hovered at 7.5-7.6% for more than six months (after falling for several years). This has raised doubts unemployment would continue to drop. In addition, surveys of firms’ hiring intentions point to employment growth losing momentum in the periods ahead. The share of firms reporting labor shortage continued to fall in all core countries, most sharply in Germany. Given this, wage growth is likely to have peaked and could start to erode resilient domestic consumption.

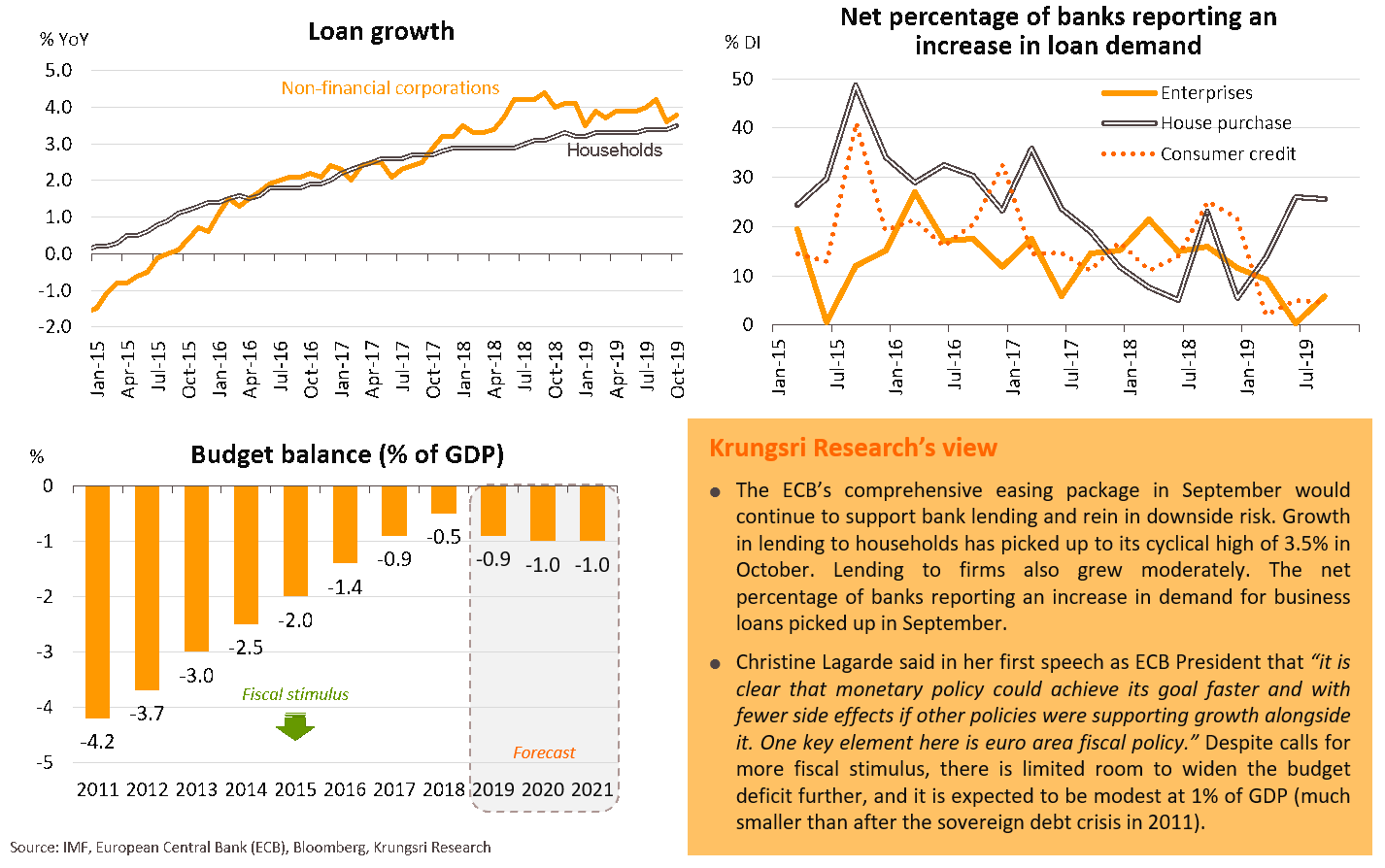

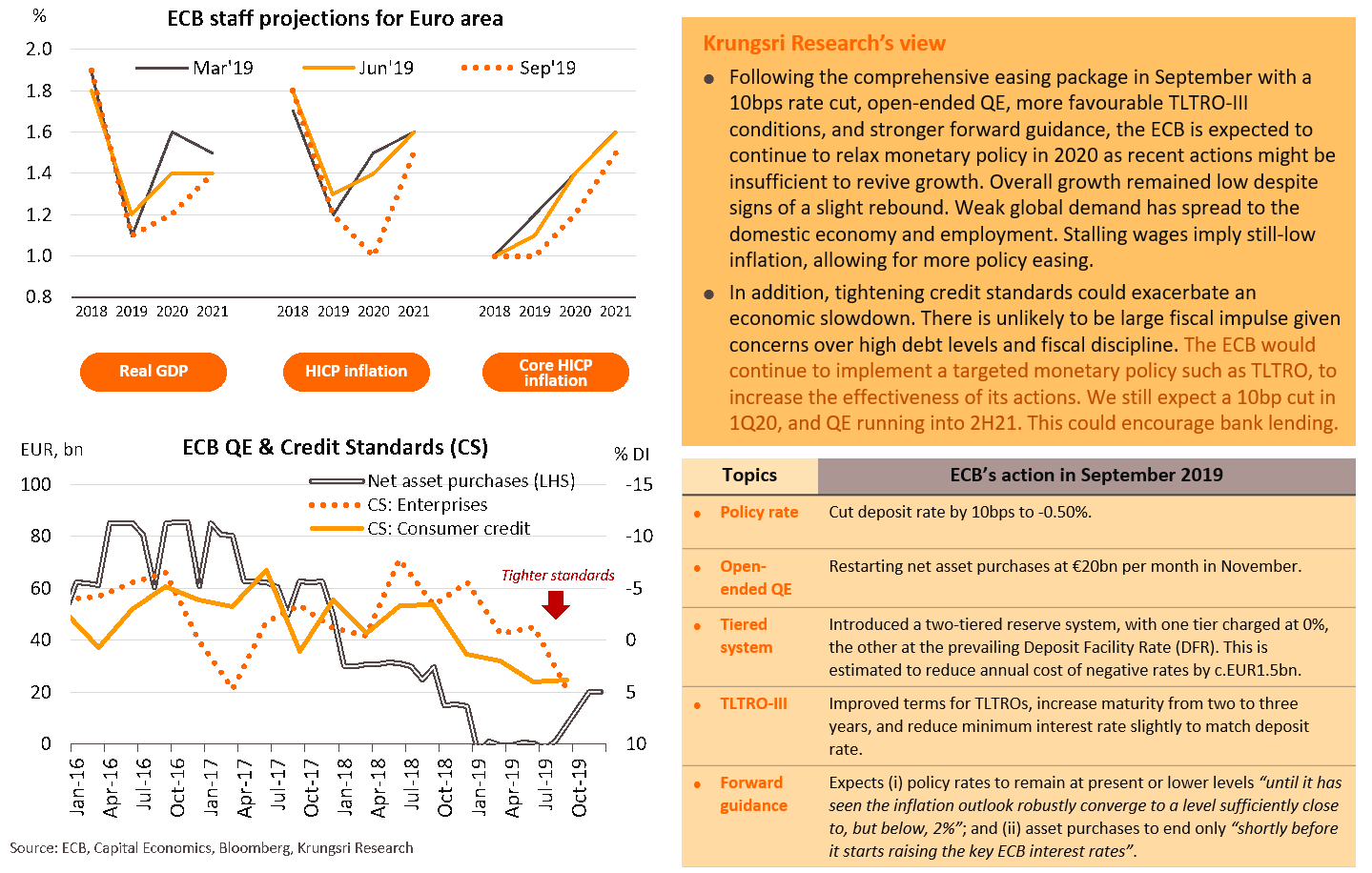

Easier credit conditions offer reassurance for the economy; calls for looser fiscal policy may not be achieved

ECB may deliver additional easing; effectiveness of targeted monetary policy will continue to improve

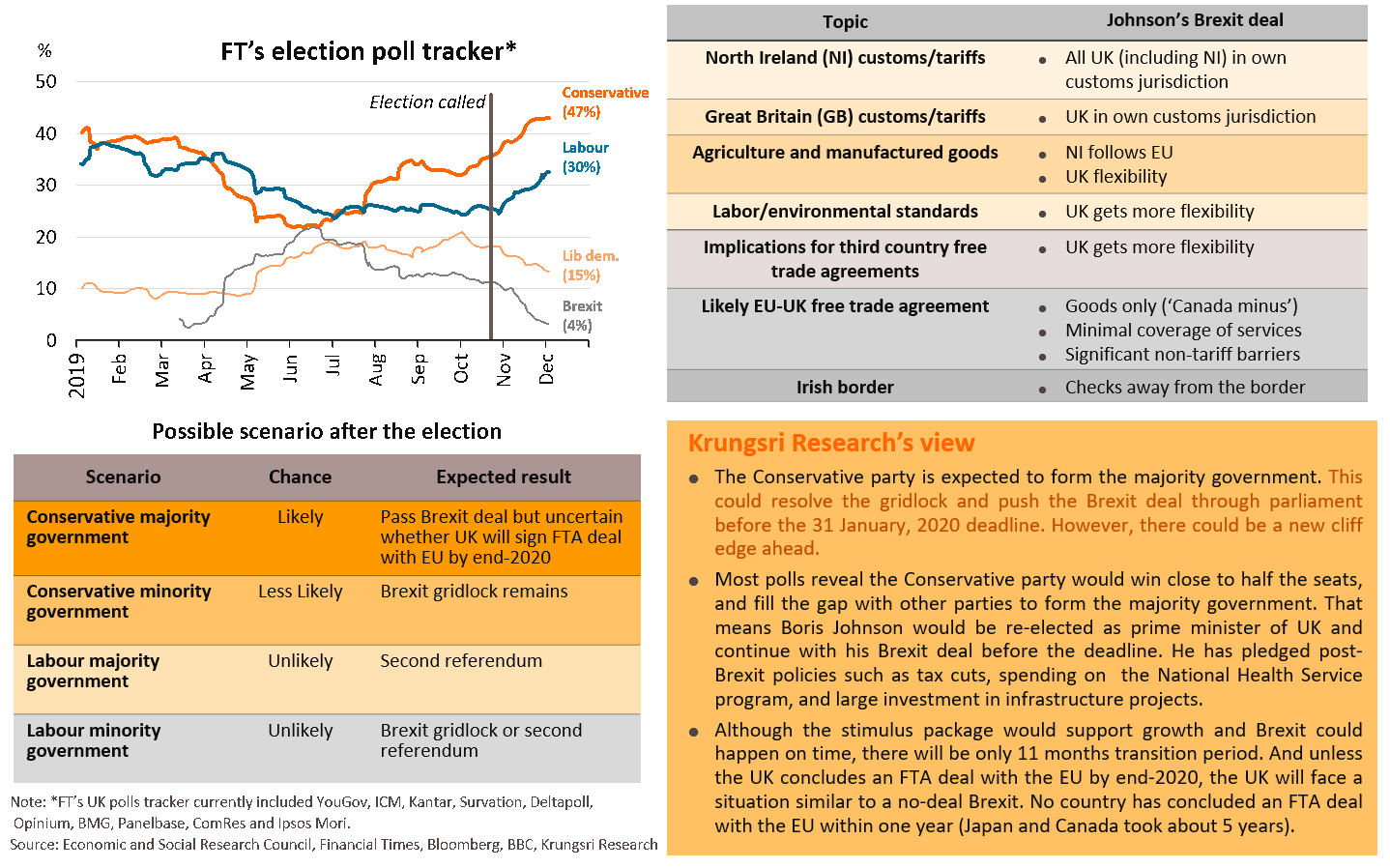

Might push though Brexit deal before deadline, but there is also post-Brexit uncertainty

China: Slow economy is manageable; trade surplus will narrow but domestic demand will improve slightly

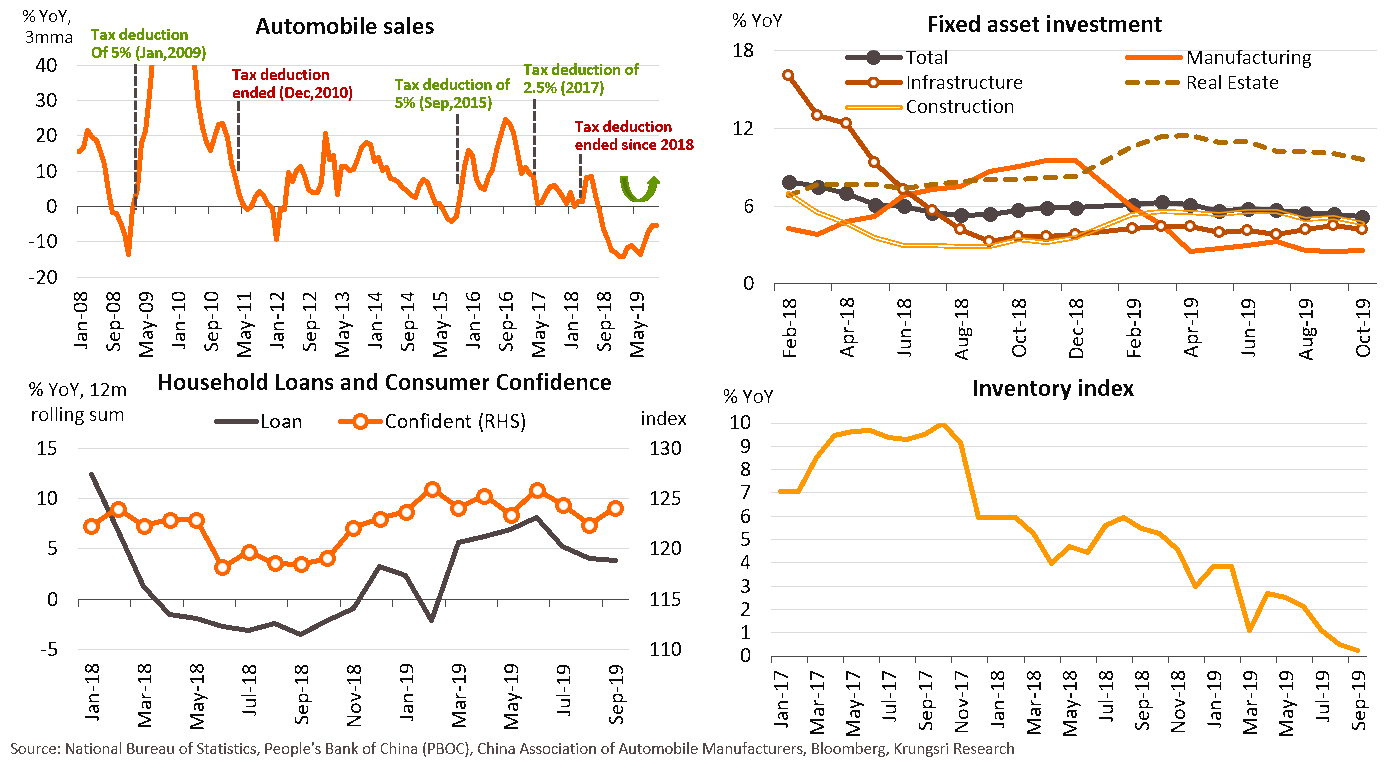

China’s economic growth is expected to slow down to 5.8% in 2020 from 6.1% in 2019. Exports should improve with a gradual recovery in global growth, but higher imports following recovering domestic demand could narrow net export surplus. Consumption could pick up as headwinds are fading. Automobile sales have bottomed out, suggesting a waning of payback effect from the earlier tax cut. Consumer confidence improved because of looser monetary and fiscal policies as well as progress in China-US trade talks. Household loan growth has started to stabilize, an early sign of higher durable goods spending. Meanwhile, fixed asset investment would be led by improving manufacturing investment, infrastructure projects and possibly restocking of inventory (after destocking for years), but growth would be curbed by a slowdown in the real estate sector.

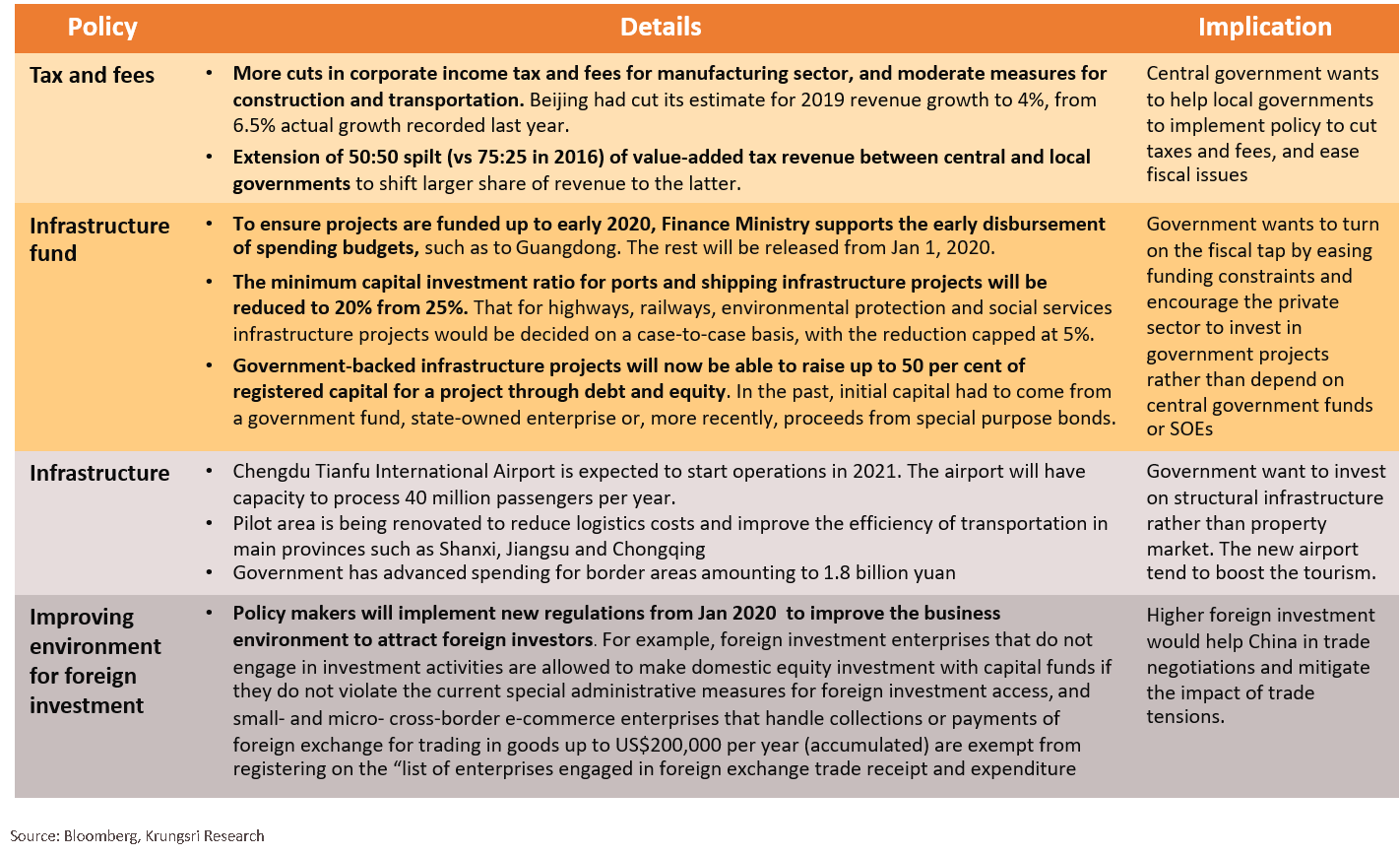

Fiscal stimulus continues to shore up economy, but lower government revenue could limit its effectiveness

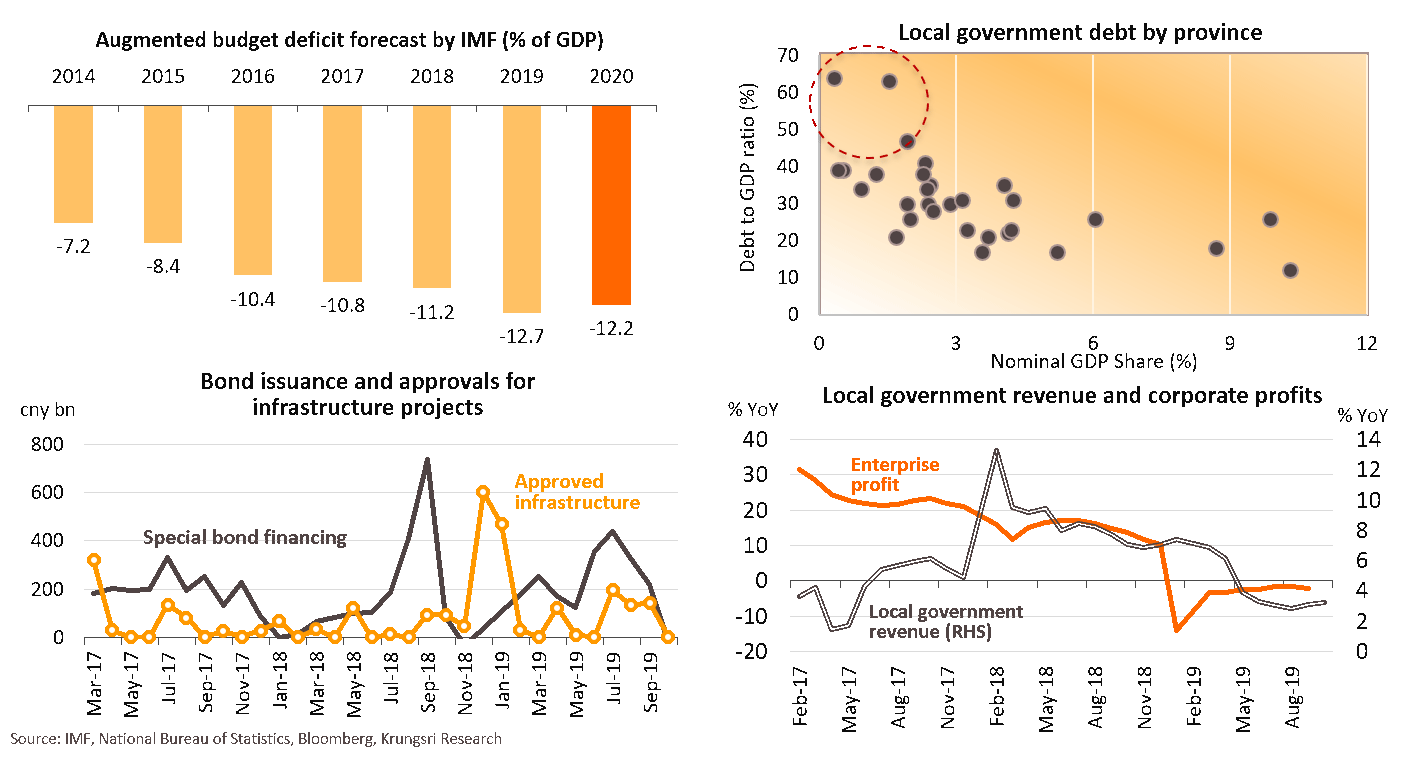

According to IMF forecasts, augmented deficit (including off-budget investment spending) would stabilize at 12% of GDP due to the government’s plan to continue with tax cuts and infrastructure spending. We believe the government will continue to ease fiscal policy to stimulate domestic demand amid lingering trade uncertainties. By area, local governments in most provinces registered low debt-to-GDP ratios, while provinces that registered high ratios are a small slice of the economy (less than 3% of GDP). However, effectiveness of policies would be moderate. Like 2019, despite a large issuance of special bonds and number of approved infrastructure projects, infrastructure investment growth only inched up to 4.2% in 2019 from 3.7% in 4Q18. This could be due to lower revenue of local governments following tax cuts and fee reductions, which could limit investment growth. Meanwhile, weak corporate profits could continue to depress the outlook for investment under public-private partnership (PPP) projects.

Fiscal stimulus shift towards private sector participation and structural infrastructure

PBOC will maintain prudent stance and targeted policy approach, implying limited support for overall growth

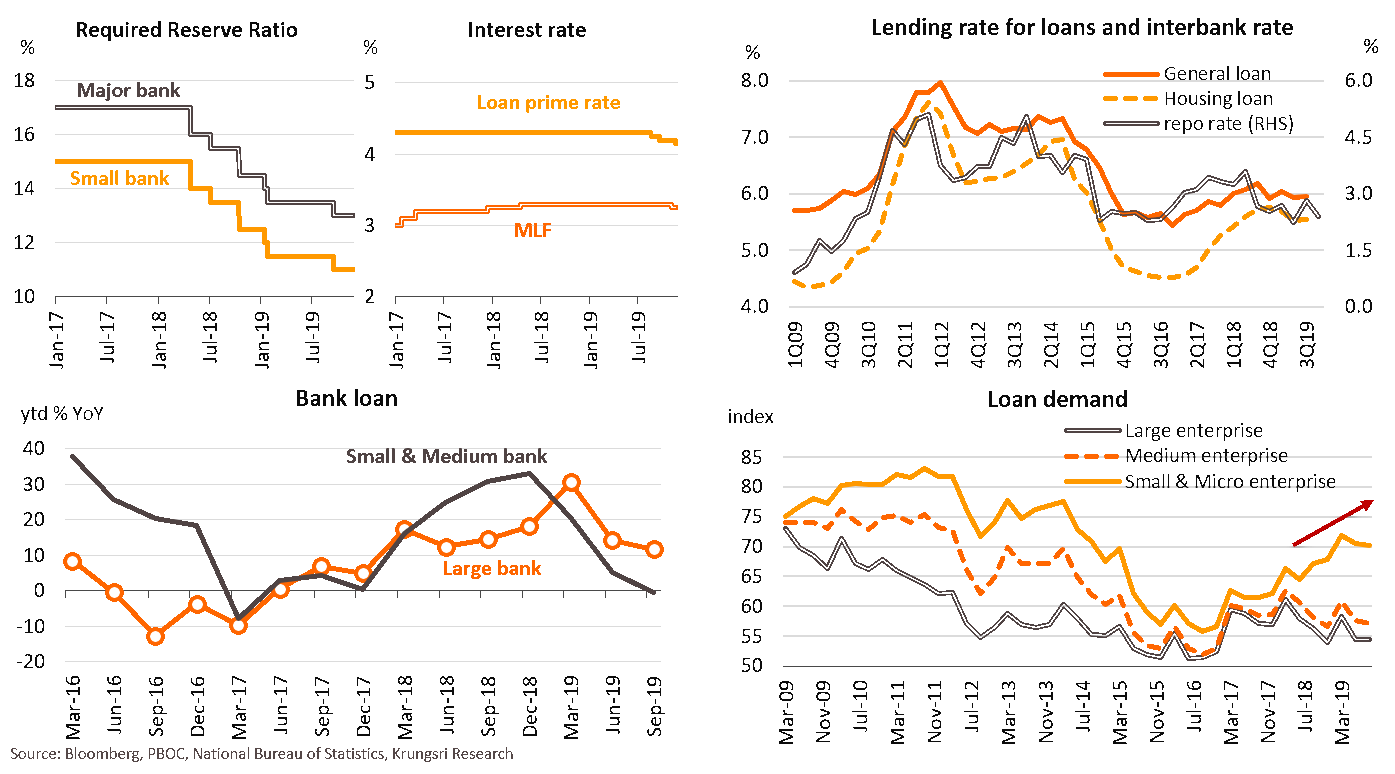

China’s central bank (PBOC) is expected to ease monetary policy by cutting RRR and loan prime rate to inject liquidity into targeted groups, especially small banks and enterprises. Although the targeted policy has reduced interbank rate (from 3.4% in 2Q18 to 2.4% in 4Q19), transmission to households and enterprises seem to be moderate, with lending rates falling by less than 0.20% from 2018. Moreover, loan growth has decelerated especially for small banks (-0.4% in 3Q19 vs +33% in 4Q18). Looking at borrowers, small enterprises usually face greater financial constraints than large and medium enterprises. Loan demand from small & micro enterprises has accelerated, compared to steady demand from other groups. This suggests a need for targeted monetary easing to help selected sectors/groups and to increase policy effectiveness.

Remains cautious despite lower risk to financial stability; preventing PBOC from employing large stimulus

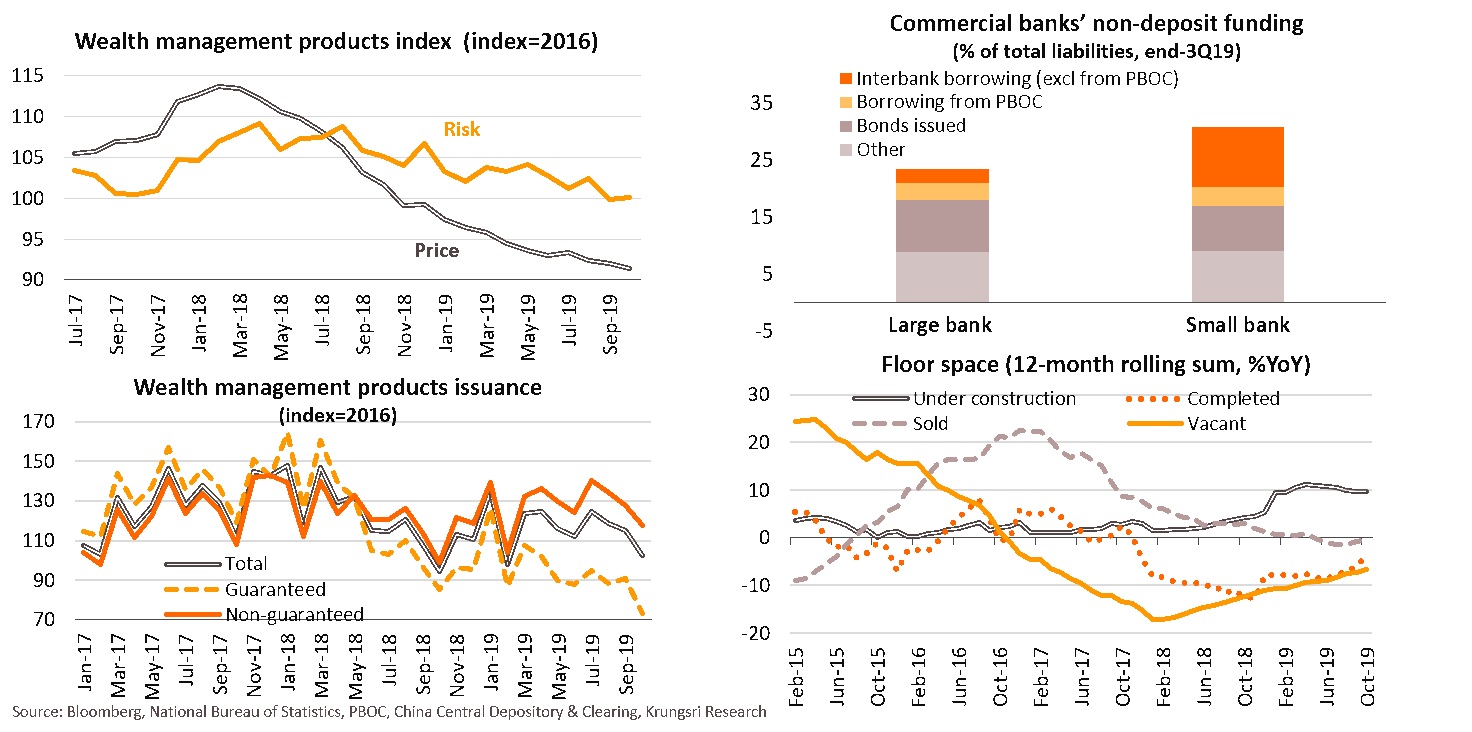

Rising risks to the financial sector have been contained in some sectors. Shadow financing has slowed to -7.4% in October 2019 from -0.7% in 2018. For wealth management products (WMPs), prices and risks have also decelerated with a decline in the number of WMP issuances (led by fewer guaranteed products). This suggests the PBOC’s aim to standardize WMPs (by letting prices reflect returns and risks) is on track in its reform plan. However, there is a need to monitor vulnerabilities in small banks. Amid the slower economy and high uncertainties, some small banks -- which rely on non-deposit funding, especially short-term borrowings from the interbank market -- could struggle with tight financial conditions. Meanwhile, although the property market is expected to cool down with fewer transactions, the increase in vacant space and space under-construction could be headwinds for the sector. The PBOC is likely to (ii) stick to a prudent stimulus approach to prevent risks to the property sector, and (ii) implement targeted monetary policy via small financial institutions to ensure the effectiveness of monetary policy.

Japan: Economy will lose momentum; higher tax threatens consumption but Olympic Games will help

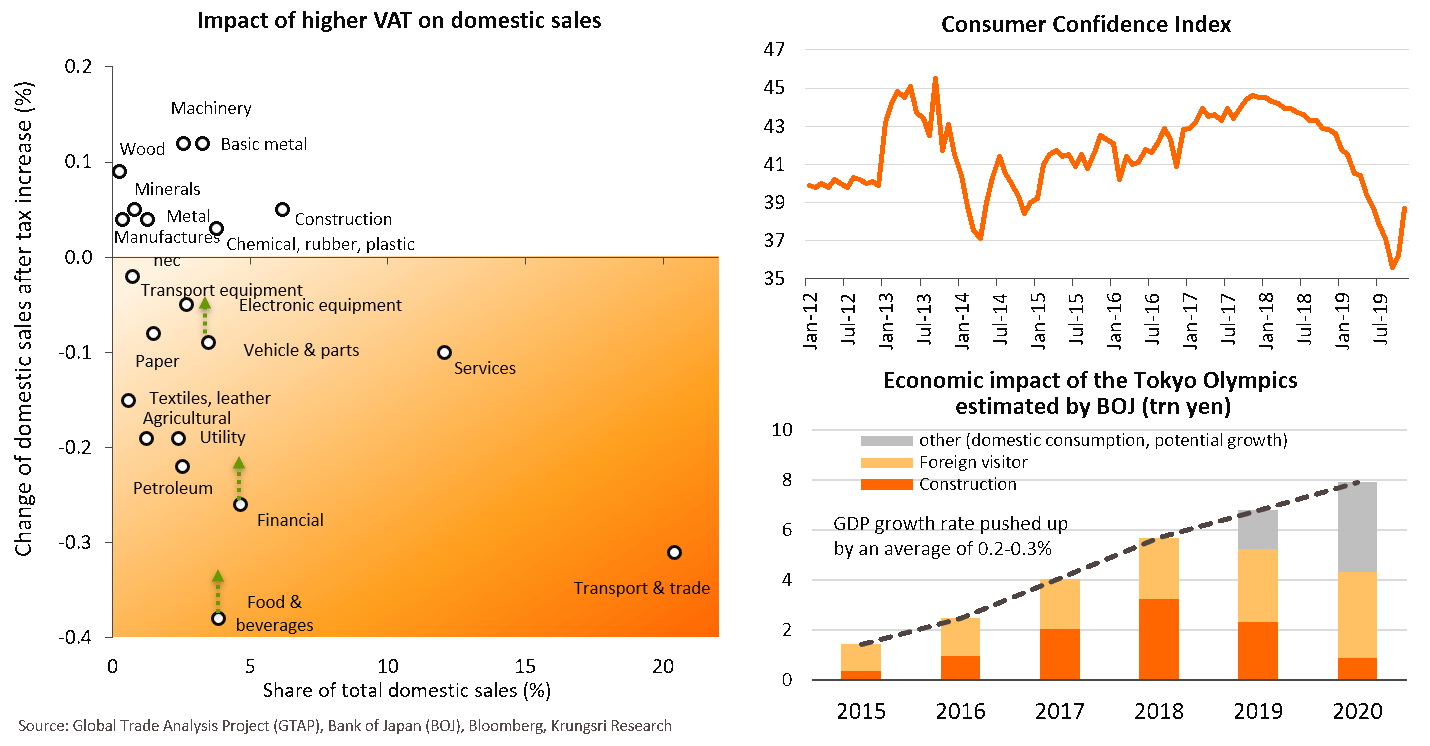

Japan’s economic growth is expected to slow to +0.5% in 2020 from +0.9% in 2019, dragged by slow private consumption and residential investment. The slowdown in consumption reflects the impact of the consumption tax hike in October 2019 which had increased overall prices and dampened consumer purchasing power. Our study shows this tax hike could reduce total domestic sales by 0.04% from base line (5-year average of consumption is 0.6%). The weak consumer confidence could hurt consumption but the impact could be smaller in some sectors such as food, vehicle and insurance, thanks to government aid measures. In addition, the 2020 Olympic Games in Tokyo would increase inbound tourism spending and income from foreign visitors, although, gains from residential construction have waned.

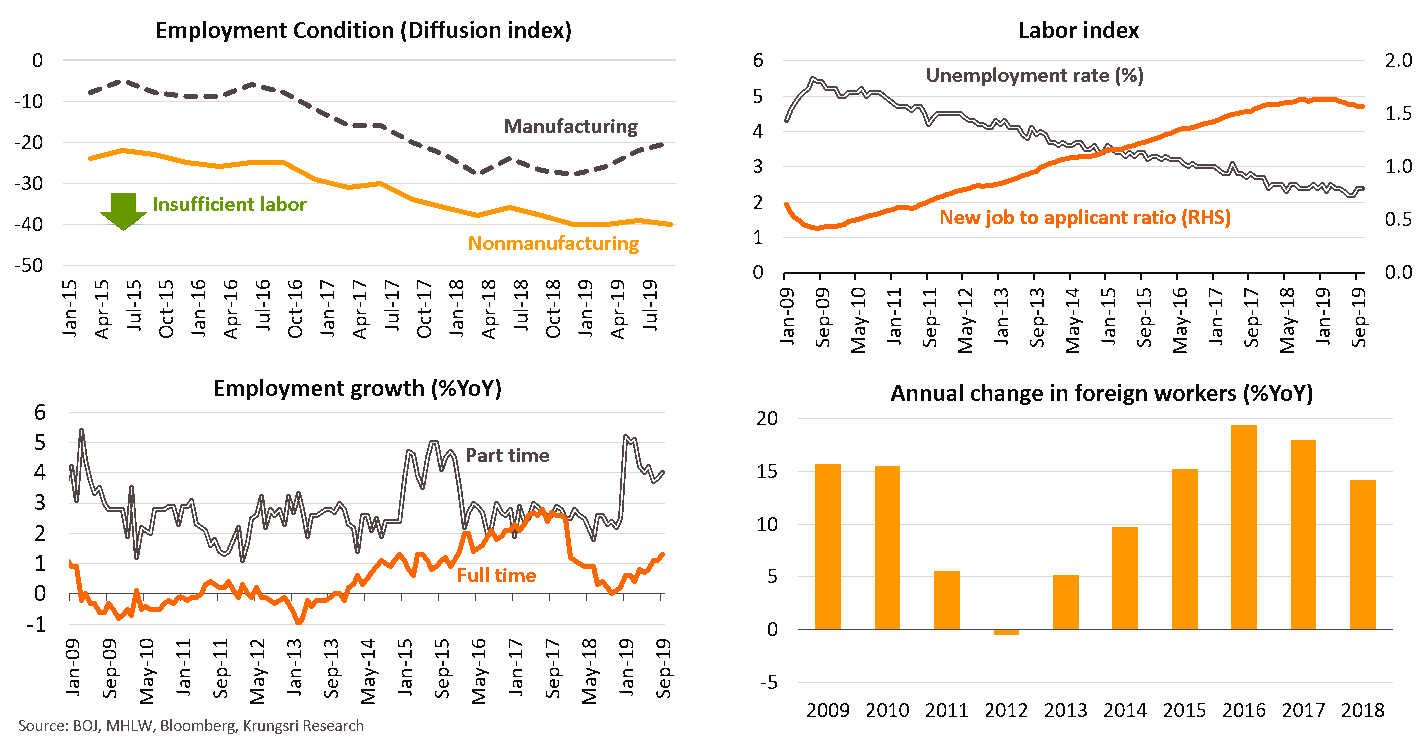

Robust labor market is propping up consumption and reduce risks of an economic recession

Despite slowing wage growth, the labor market remains robust across sectors. Demand for labors in the manufacturing sector remains strong, albeit slower, and remains high in the non-manufacturing sector. Full-time employment has also picked-up from lows at the start of 2019, and there is favorable growth in temporary employment. The record-low unemployment rate and high jobs-to-applicant ratio suggest a robust labor market. This should prop up consumption and reduce risks of an economic recession. For sectors that face severe labor shortage, manufacturers’ costs could rise and hurt corporate profits. Although the government introduced a new immigration law on April 1 to attract foreign labor, the effectiveness of this policy is limited by strict qualification requirements. The immigration agency had expected to attract 40,000 foreign workers by March 2020, but as of November only 895 new work permits had been issued. This suggests those sectors will continue to invest in labor-saving facilities.

Business investment remains cautious despite improving exports and still-firm labor-saving Capex

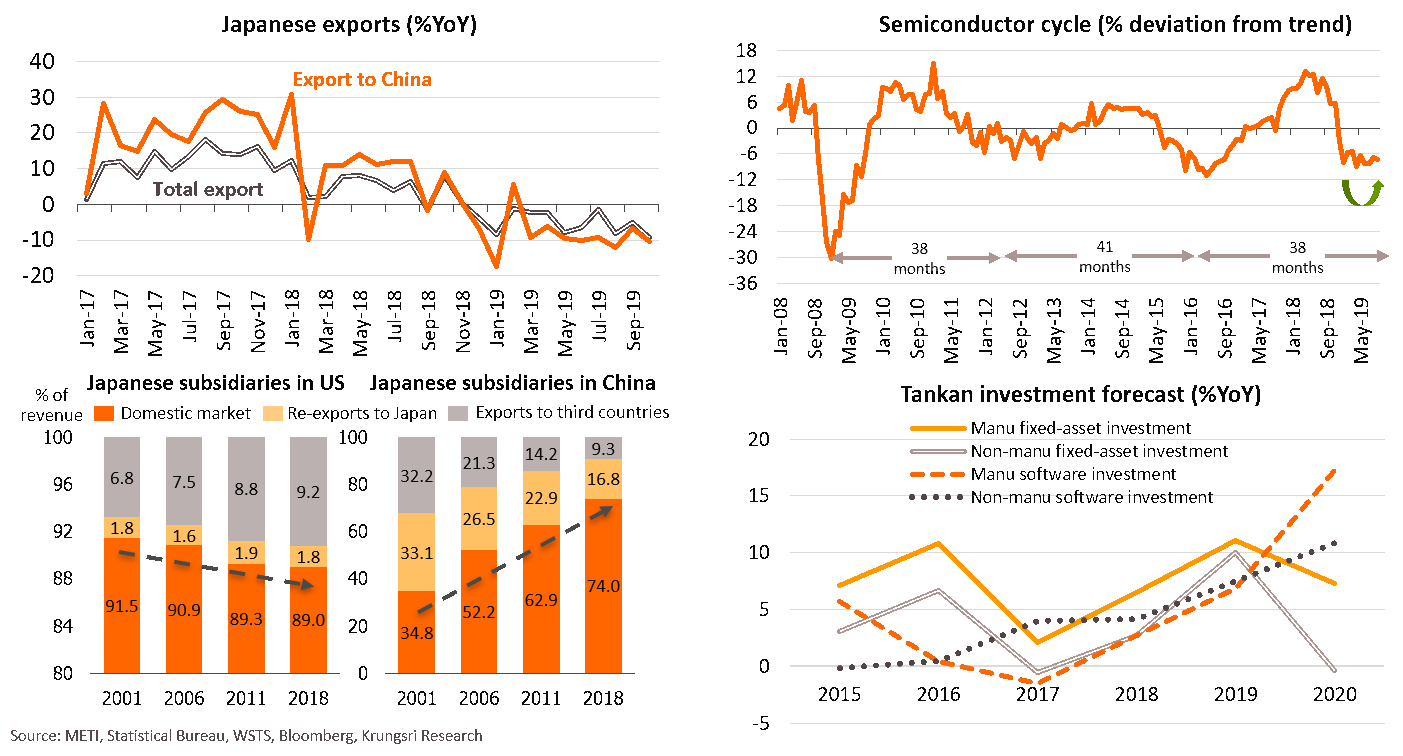

We see exports improving only slightly along with global demand. Japanese exports could be aided by tailwinds from relatively strong growth in domestic demand in China. For Japanese manufacturers, China has increasingly become an export destination rather than simply for offshore subsidiaries, reflected by a surge in the share of revenue from Japanese subsidiaries. Furthermore, the current cycle for IT-related exports has lasted 38 months, close to the recent completed cycles (38-41 months). Japanese electronics may gain from a possible upturn in the current cycle in 2020. This could increase capital-expenditure on labor-saving technologies (e.g. software). However, we expect overall investment growth to remain weak due to still-high uncertainty over global trade, a decline in construction activity for the Olympic Games, and softer domestic demand following the sales tax hike.

Japan-South Korea dispute hits tourism and automobile exports, but impact is limited

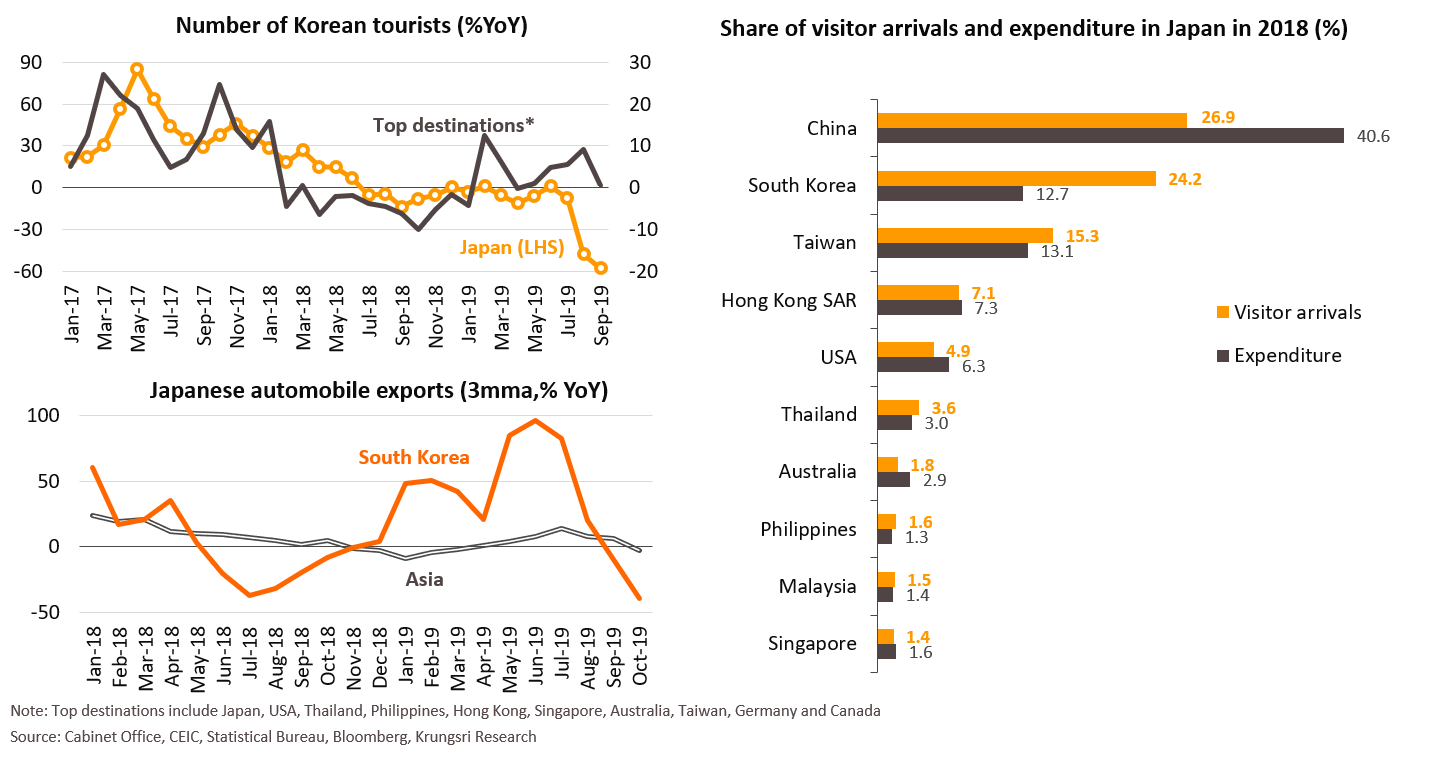

The spat could be headwinds in Japan’s tourism industry. South Korean visitors to Japan had dropped by 58% YoY in September but the effects could be limited. Although Korean tourists are the second-largest share of arrivals at 24.2%, their spending is only 12.7% of total foreign tourist spending in Japan. This is much less than spending by Chinese tourists at 40.6%. Apart from the Services sector, Japanese automobile exports to South Korea continued to decline after Korean consumers started to boycott Japanese goods since July amid the escalating conflict, but the impact is moderate because automobile exports to Korea account for only 0.9% of Japan’s total automobile exports. Nevertheless, because South Korea is the third largest export market for Japan at 7% of total Japanese exports, it cold get worse if the boycott spreads to other export items.

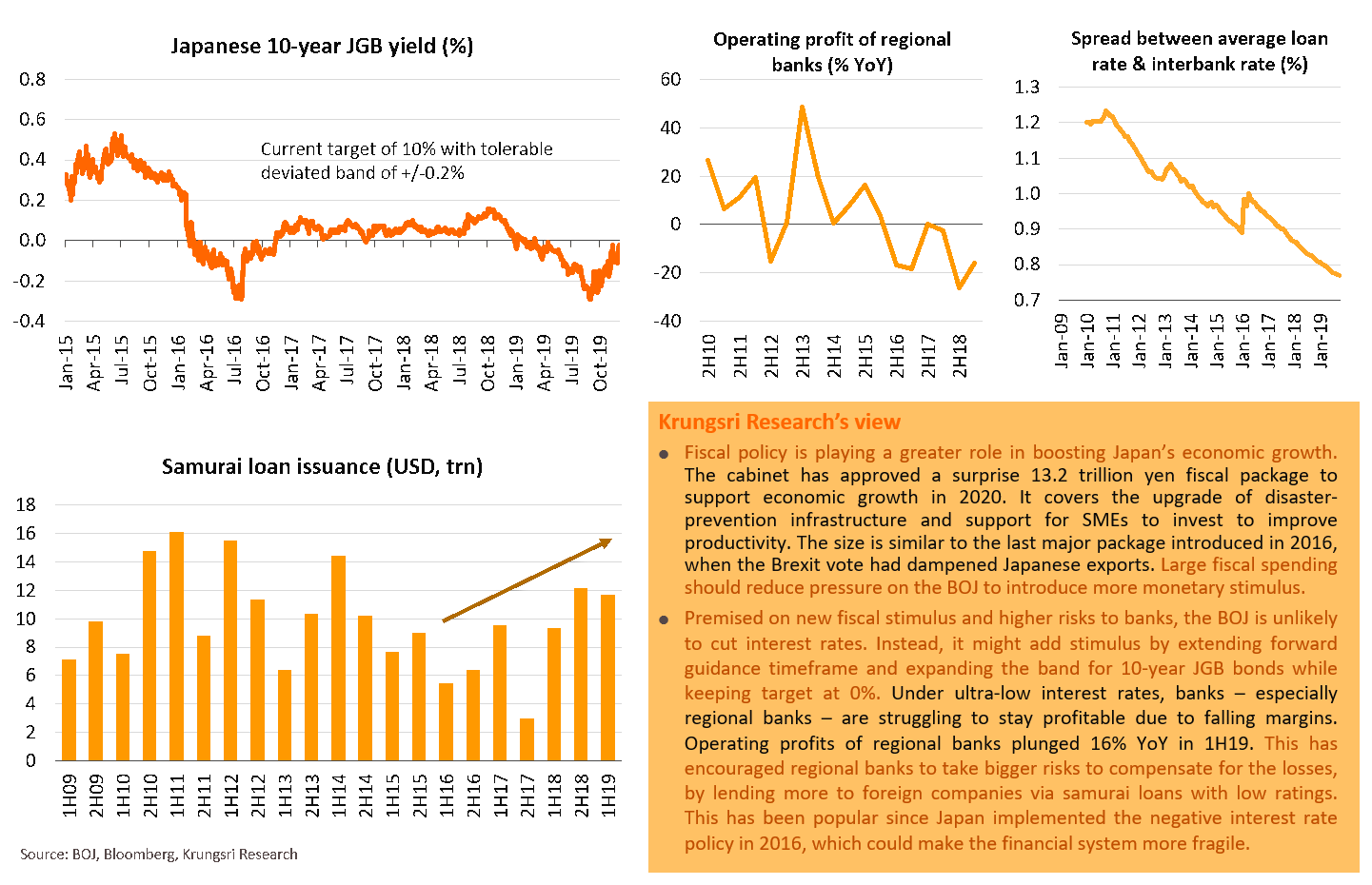

Greater role of fiscal policy reduces pressure on BOJ to introduce more monetary stimulus

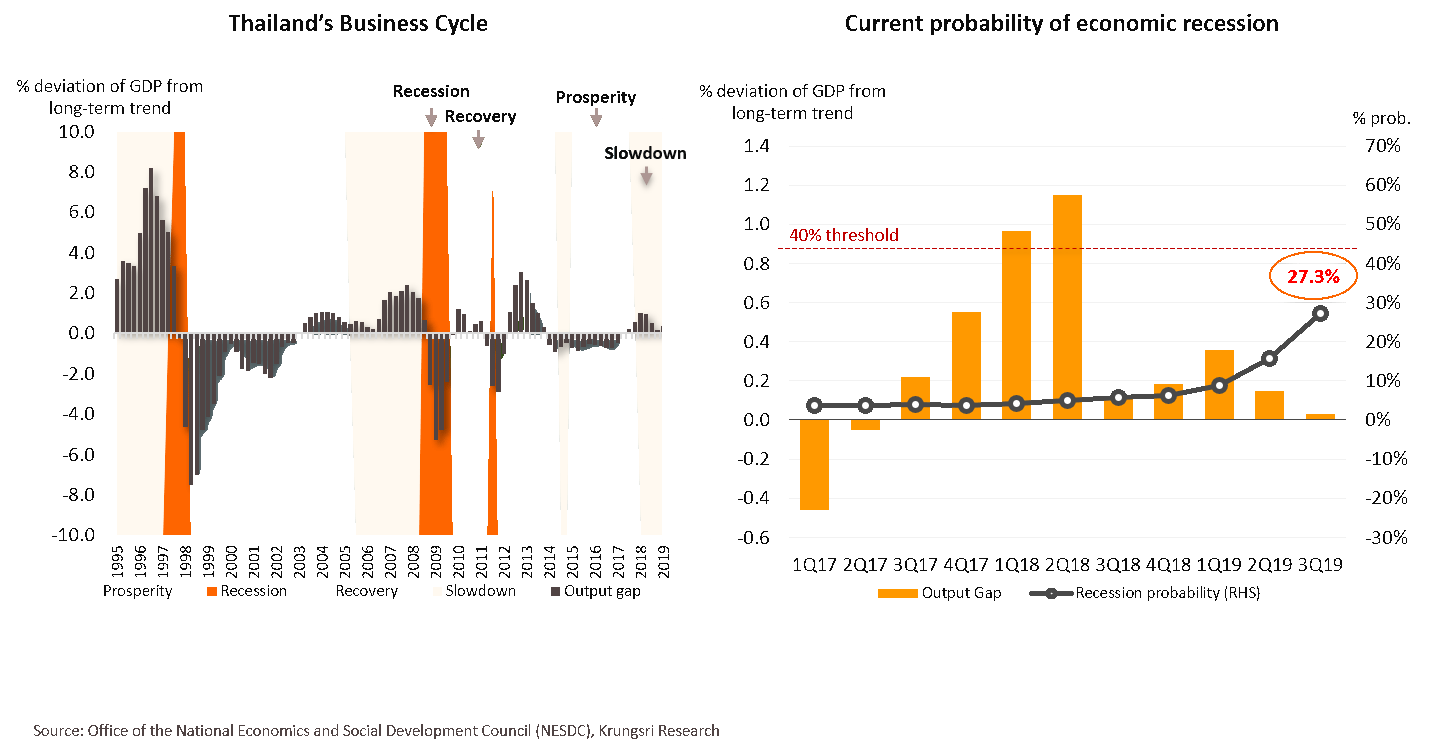

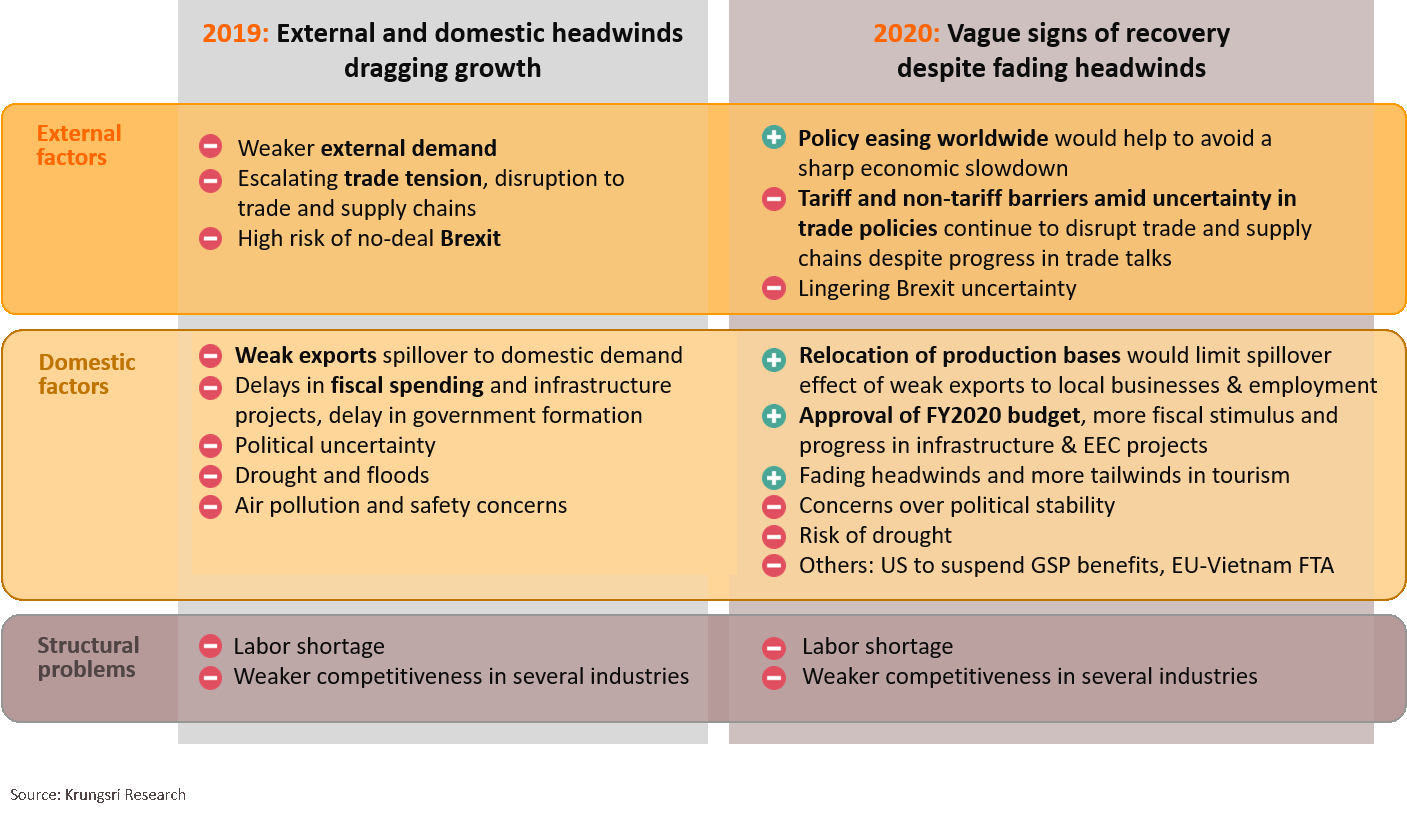

Thai economy: Slowing down amid rising recession risks

Krungsri Research developed the Markov Regime-Switching Model to estimate risks of an economic downturn. The model captures Thailand’s economic recessions in 1997, 2008 and 2014. The model suggests the Thai economy is in a period of slowing growth. A probability above-40% indicates very high risk of a recession. The probability of an economic recession in Thailand has risen to 27.3% in 3Q19 from 4.1% in 1Q18, still below 40%.

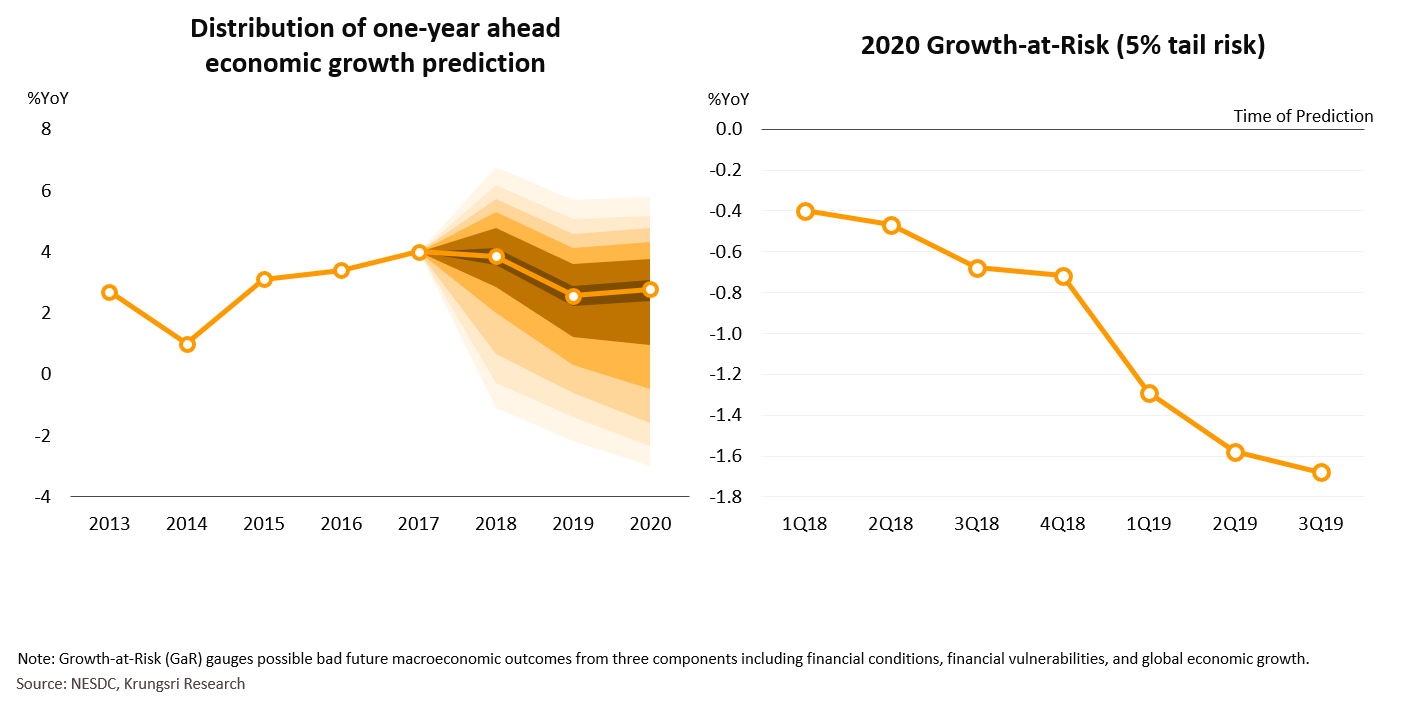

Greater uncertainty: Expect 2020 median growth forecast to inch up but risks are biased towards downside

Thailand’s economic growth (median forecast) is expected to improve slightly in 2020. However, there will be rising uncertainties, reflected by the wider forecast band in the fan chart. The Growth-at-Risk (GaR) concept also suggests the macroeconomic scene would be worse than the previous year. There is 80% probability the range of one-year ahead growth forecasts would widen from 0.3% to 4.1% predicted in 2018 to -0.5% to 4.3% predicted in 2019. Also, the low-end of the forecast band has been dropping since early 2018, from -0.4% in 1Q18 to -1.7% in 3Q19. These reflect increasing uncertainty and risks to the Thai economy.

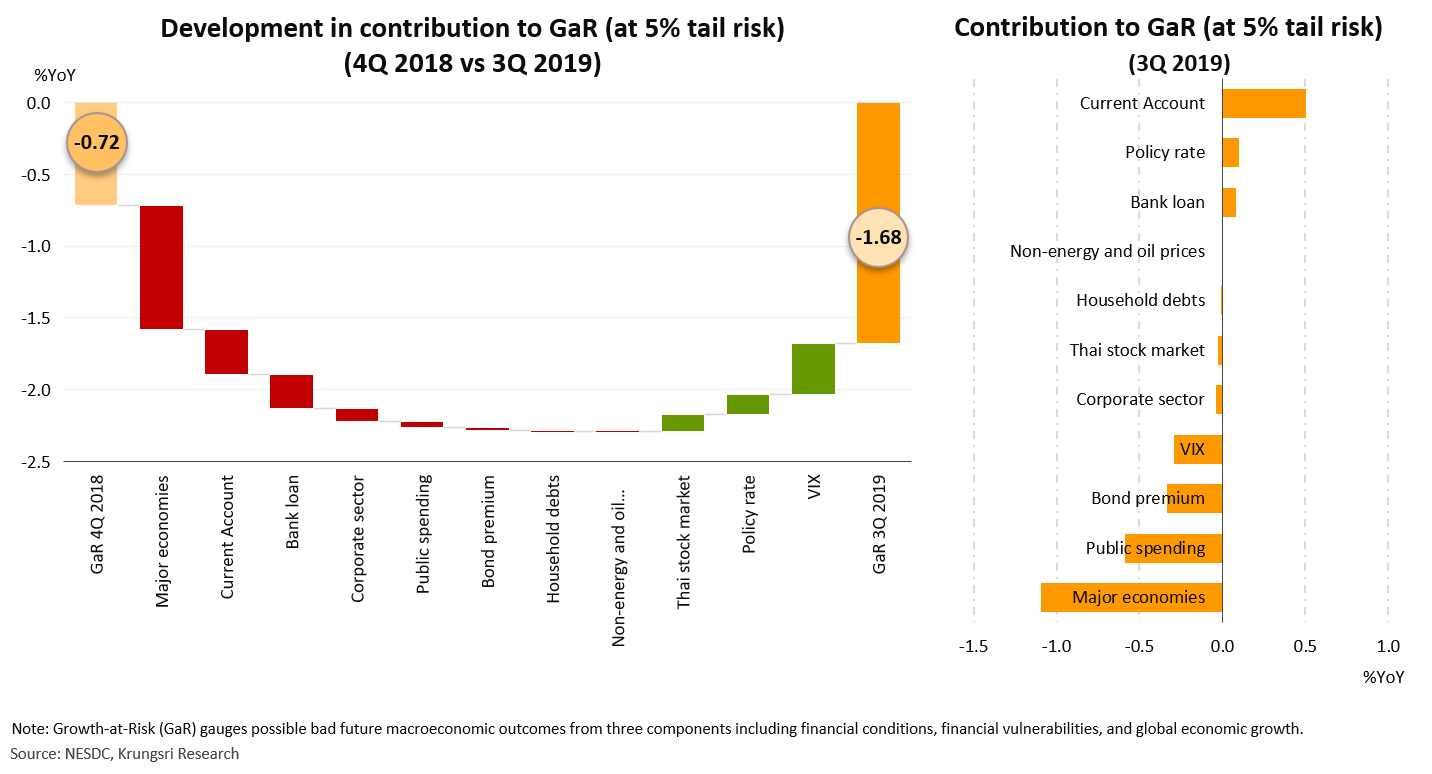

Economy will be more fragile as downside risks mount

Over the past year, the Thai economy has become more fragile due to slowing economic growth in major economies. Also, rising uncertainties in the bond market and lower-than-expected public spending continued to drag the economies. Meanwhile, the banking sector is also less supportive of growth in the Thai economy, with low policy rates having a small impact.

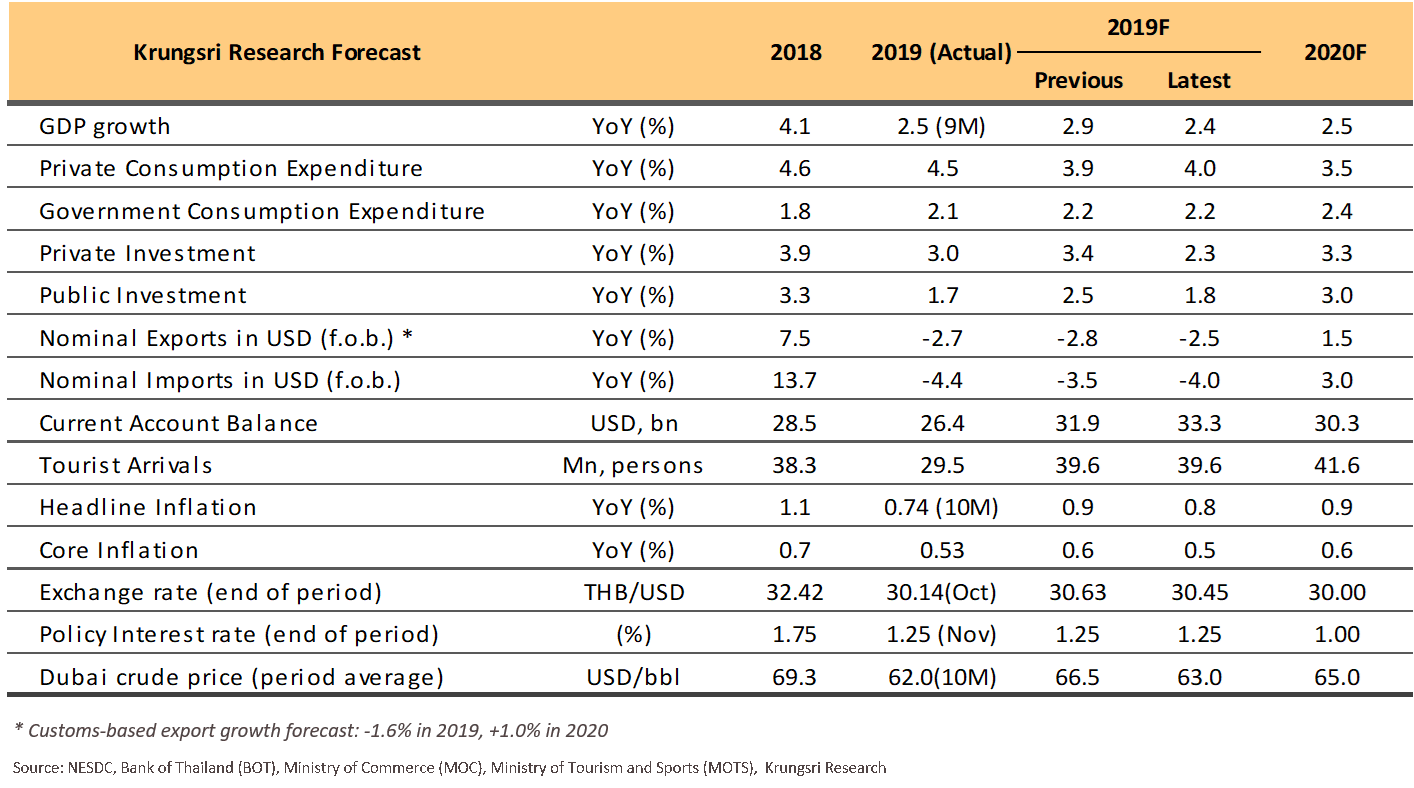

Thailand Economic Outlook 2020

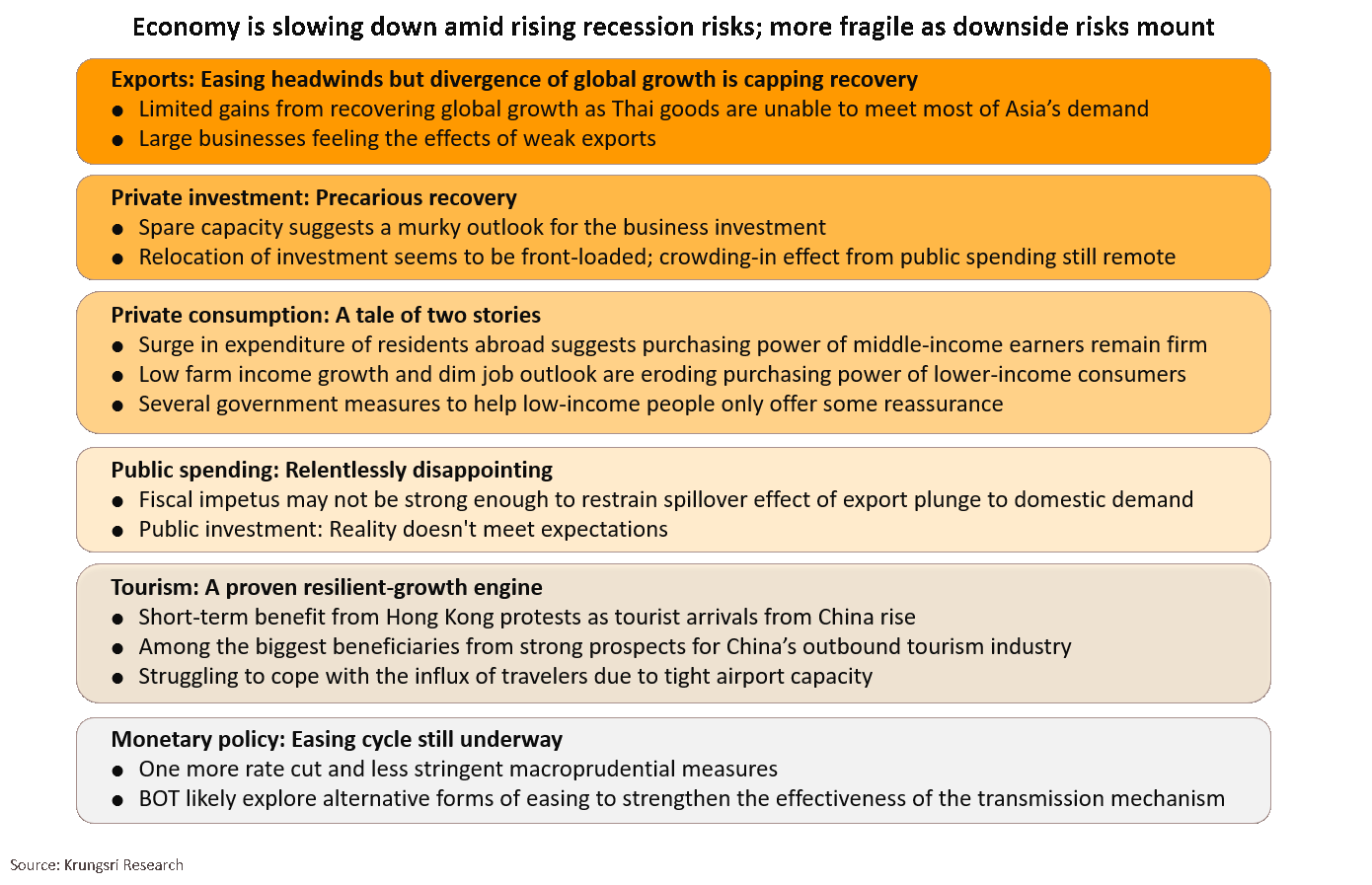

Thai economy in 2020: Some headwinds are easing but growth drivers remain fragile

Highlights for 2020: Another year of sluggish, below-potential growth

Exports: Limited gains from improving global growth as Thai goods contribute little to Asia’s domestic demand

Looking ahead, global GDP growth is expected to improve to +3.4% in 2020, compared to the post-financial crisis low of +3.0% in 2019. This would be driven by improving economic growth in developing countries rather than major countries. However, Thai exports would see limited gains from a more optimistic outlook for developing countries in Asia because these countries (including ASEAN countries), have relatively low dependence on Thai products to meet their domestic demand, unlike Europe and the US. Therefore, the weak growth outlook for major countries could mean downside risk for Thai exports.

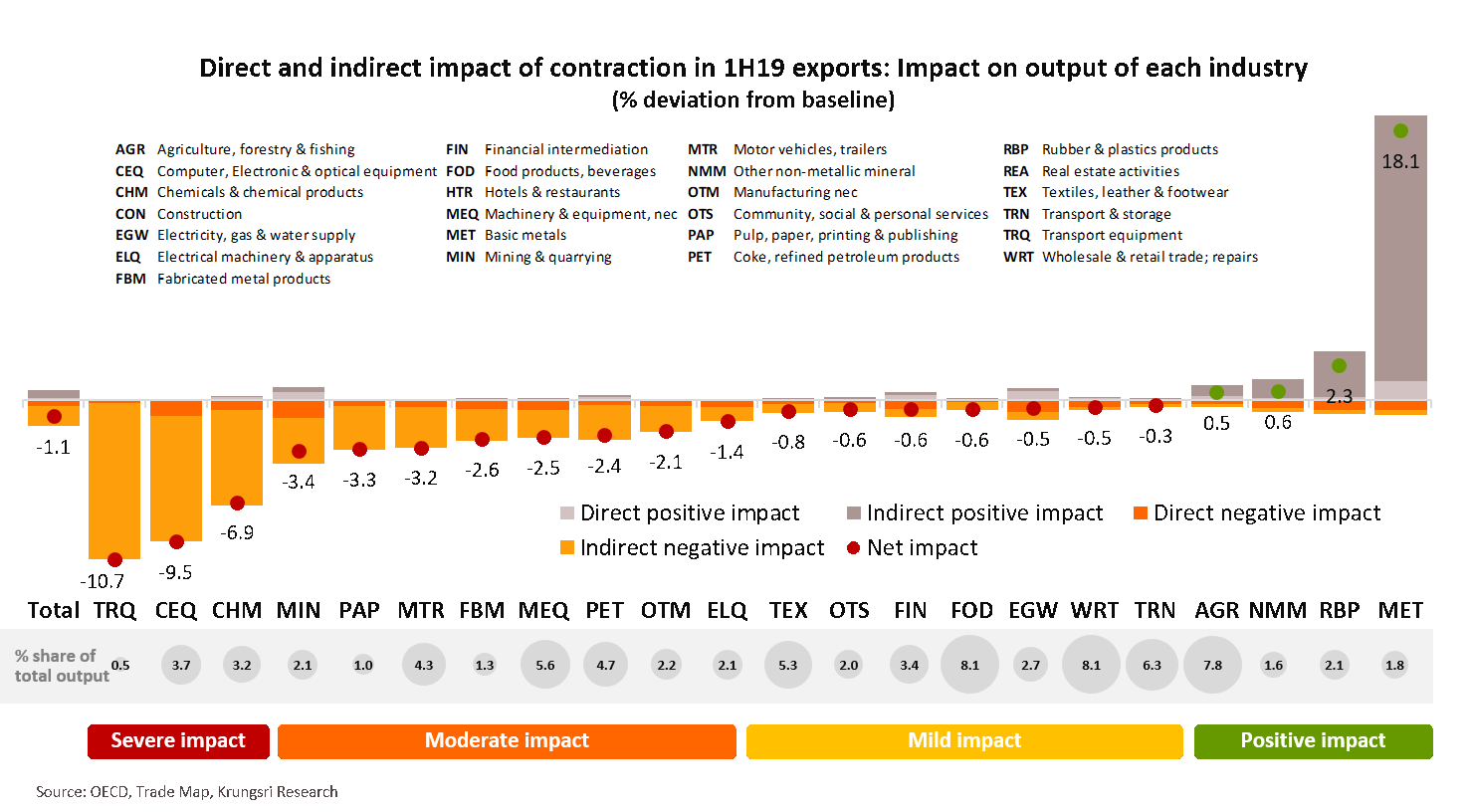

Indirect impact of weak exports is much larger than direct impact, due to ripple effect on the supply chain

The weaker exports have hurt most Thai industries, led by indirect negative impact on transportation equipment, computer & electronics, chemicals & chemical products, mining, pulp & paper products, and motor vehicles. The weak exports also had knock-on (but mild) impact on non-exports and service sectors such as financial intermediaries, wholesale & retail trade, and transportation.

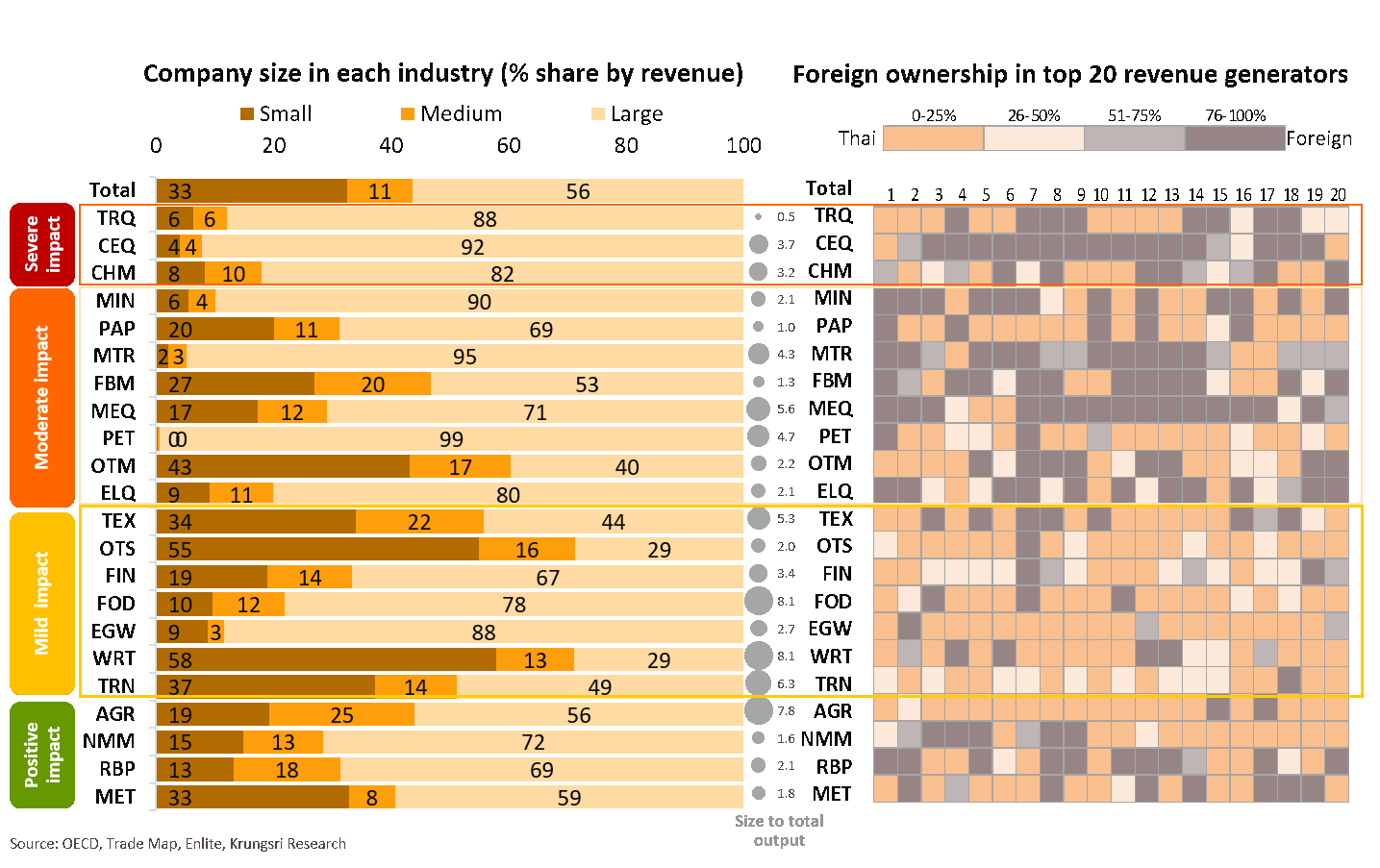

Moderate-to-severe impact on large foreign firms

Large-size firms account for 80-90% and 40-99% of firms in severely- and moderately-affected sectors, respectively, and 29-88% in mildly-affected sectors. Nationalities of firms in the first sectors are mixed but those in mildly-affected sectors were mostly owned by Thai and Thai majority shareholders.

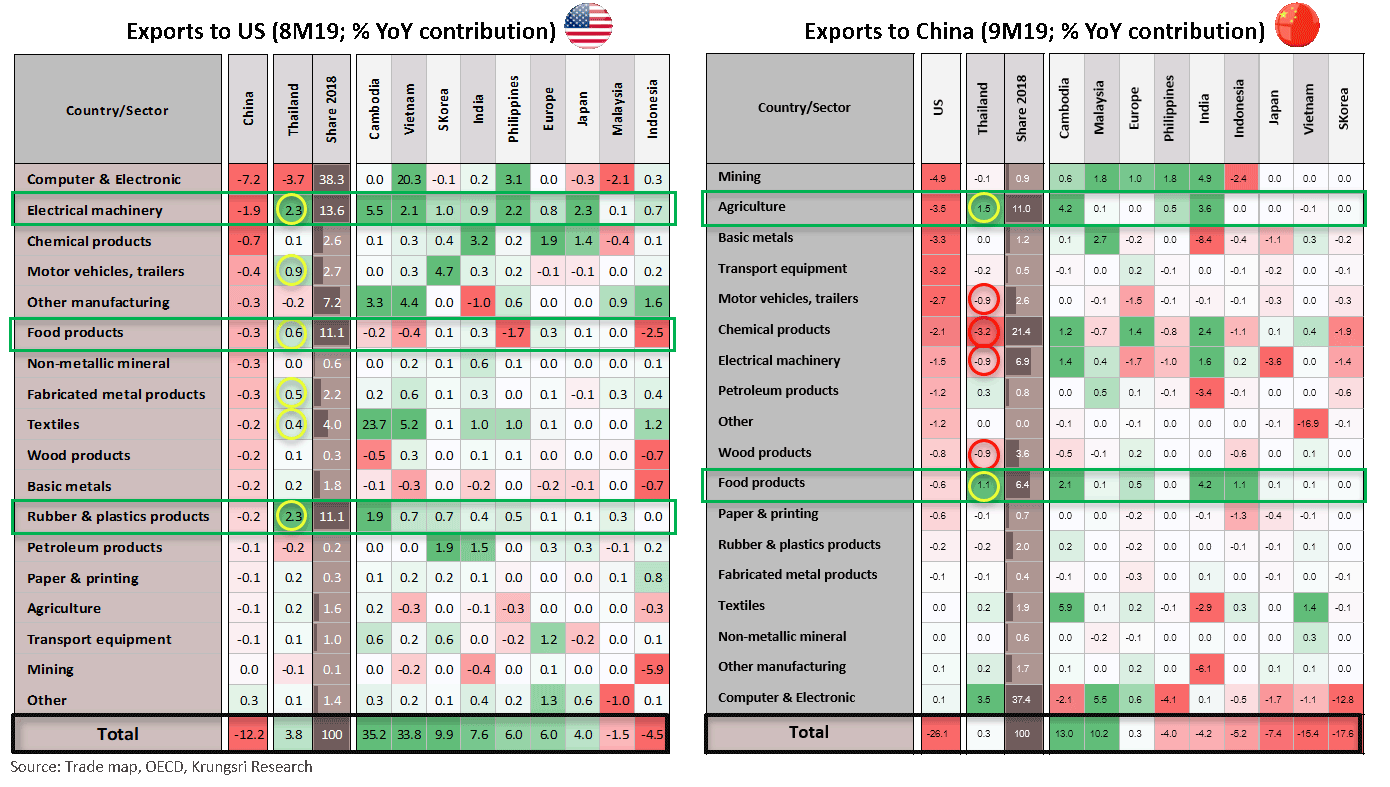

Mild positive effects from trade diversion after US-China tariffs; some gains in Thai exports to the US

The spate of tariffs have hurt US-China trade, but Thai exports -- particularly to the US -- could benefit from trade diversion, led by electrical machinery, rubber and plastic products, and food products. In the China market, Thailand could gain from substitution effect but the magnitude would be mild and possibly only in a few sectors. Hence, Thailand could register smaller gains from trade diversion than some other countries. At the same time, many sectors in China that import Thai materials had shrunk after the supply chain was disrupted, especially chemical products and electrical machinery.

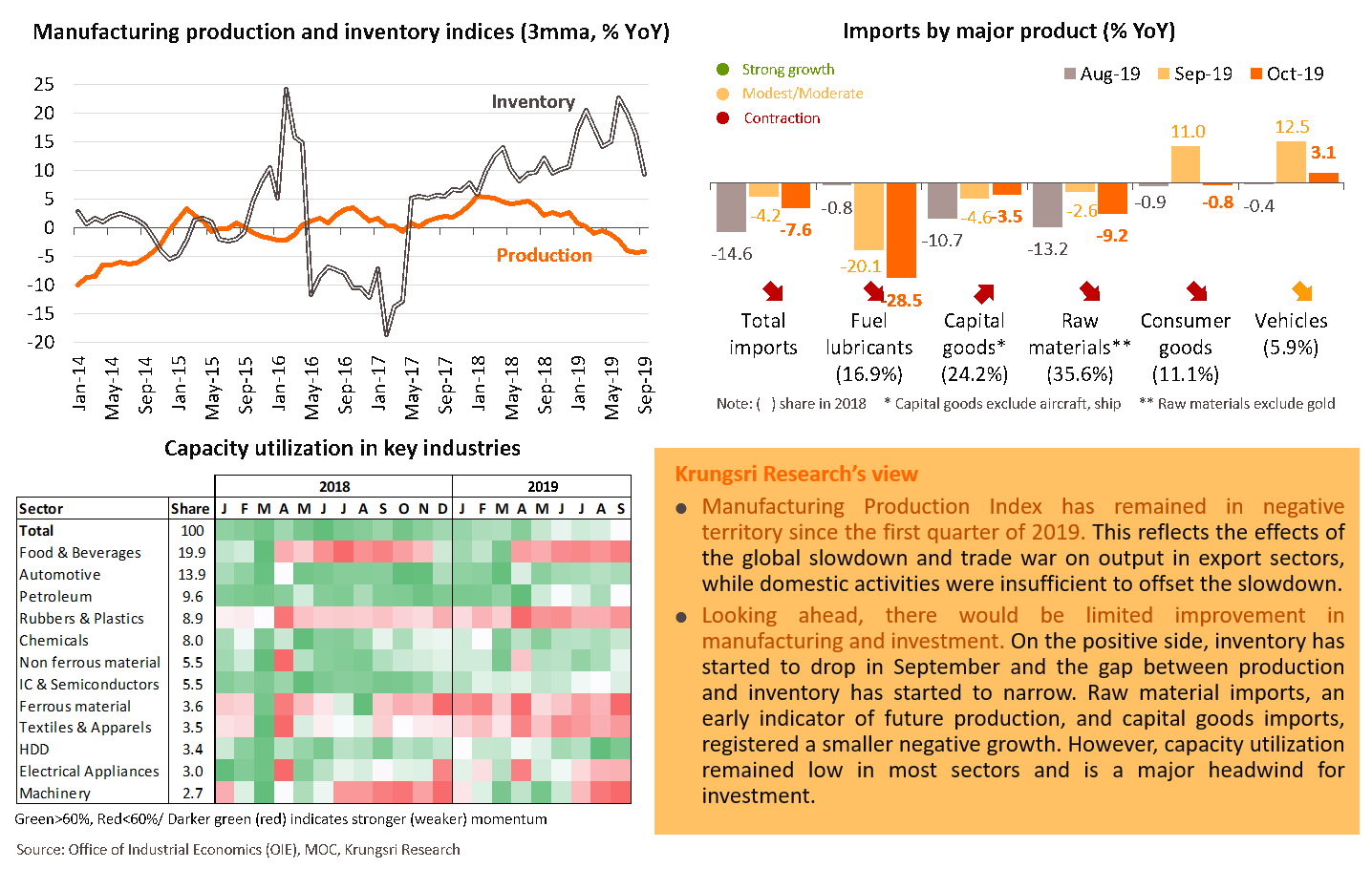

Private investment: Spare capacity suggests murky outlook for business investment

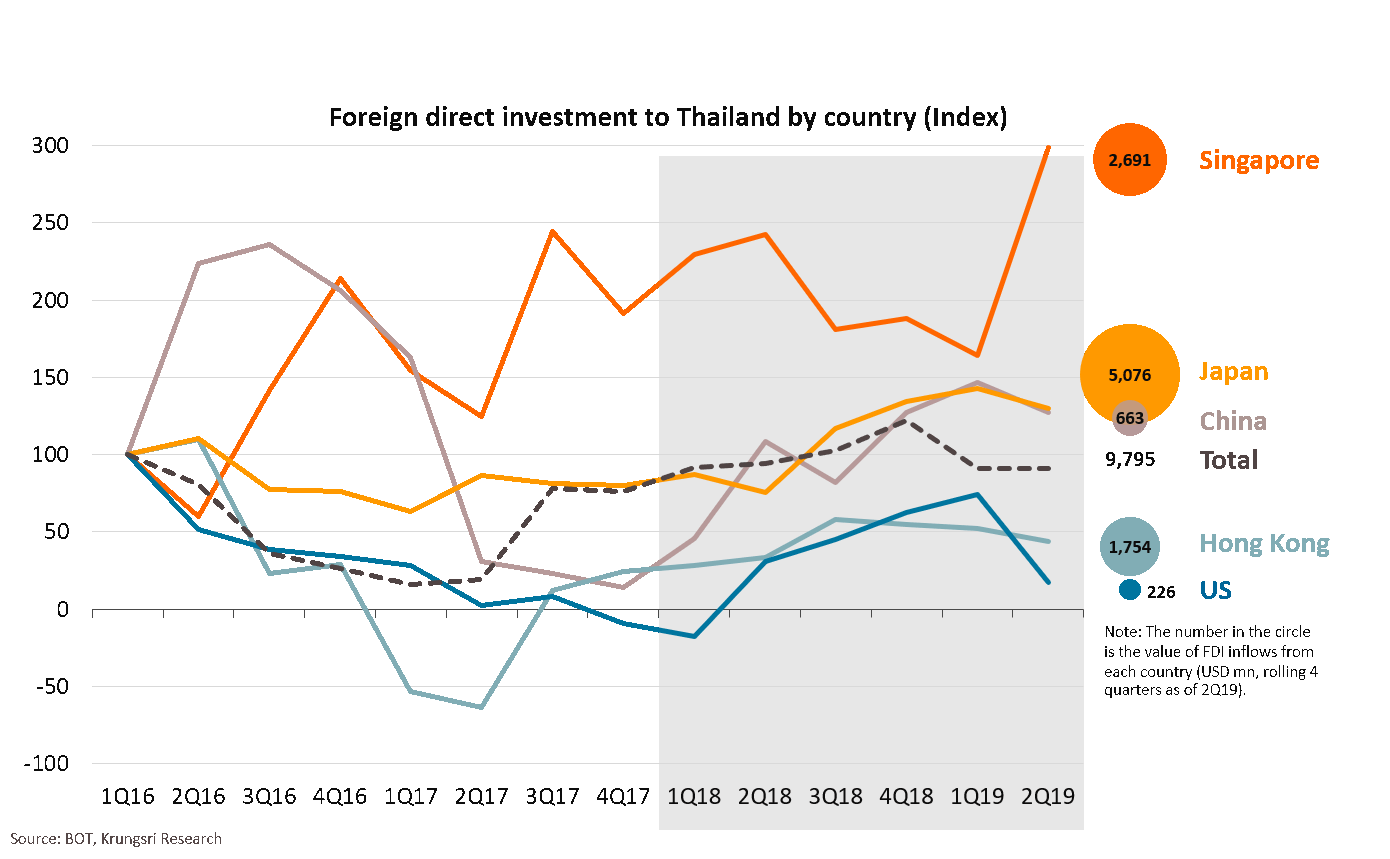

Foreign direction investment: moderate signs of relocation of production bases to Thailand

Since the US-China trade war escalated in 2018, there have been signs of relocation of production bases to Thailand. This is reflected in the rebound in foreign direction investment (FDI) inflows from several countries, including the US and China. In 2019, those signs seem to be moderate with mixed data. Total FDI inflows to Thailand fell 3.6% YoY in 2Q19 (vs +60.5% in 4Q18) partly due to the slower global and Thai economies, as well as weaker sentiment of producers around the world amid uncertainties. However, recent FDI inflows from China and Japan remain well above the levels in early 2018, and inflows from Singapore, the major financial intermediary hub in this region, have surged.

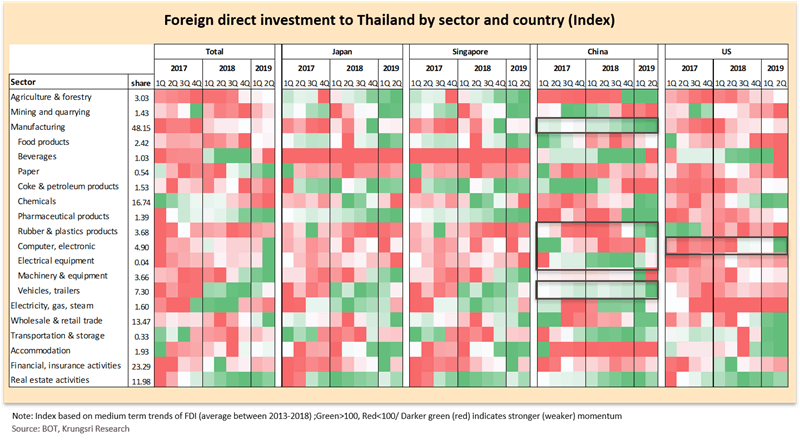

Total FDI inflows rose in some sectors; China inflows are more broad-based than US inflows

Overall FDI inflows to some sectors have risen, led by computer, electronic & electrical machinery, and vehicles. Following rising trade tensions, there have been more FDI inflows from China especially in the manufacturing sector, such as rubber & plastics, motor vehicles, and electrical equipment. This suggests some Thai products could benefit from replacing Chinese exports to the US. Meanwhile, inflows from the US have been limited in sectors such as computer & electronics which saw relocation of production bases to Thailand.

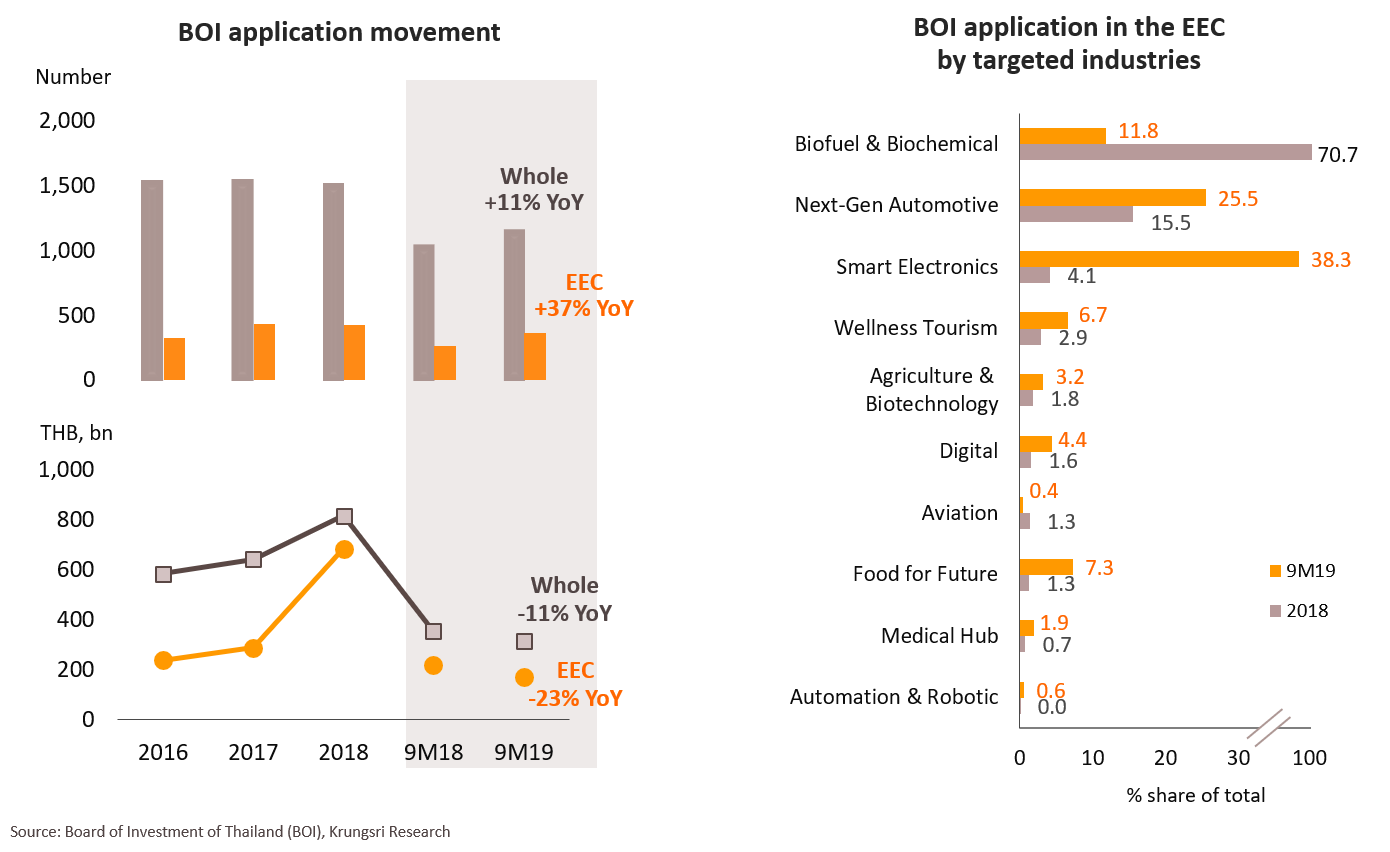

Investment in EEC: Applications rose but investment value dropped, implying limited growth ahead

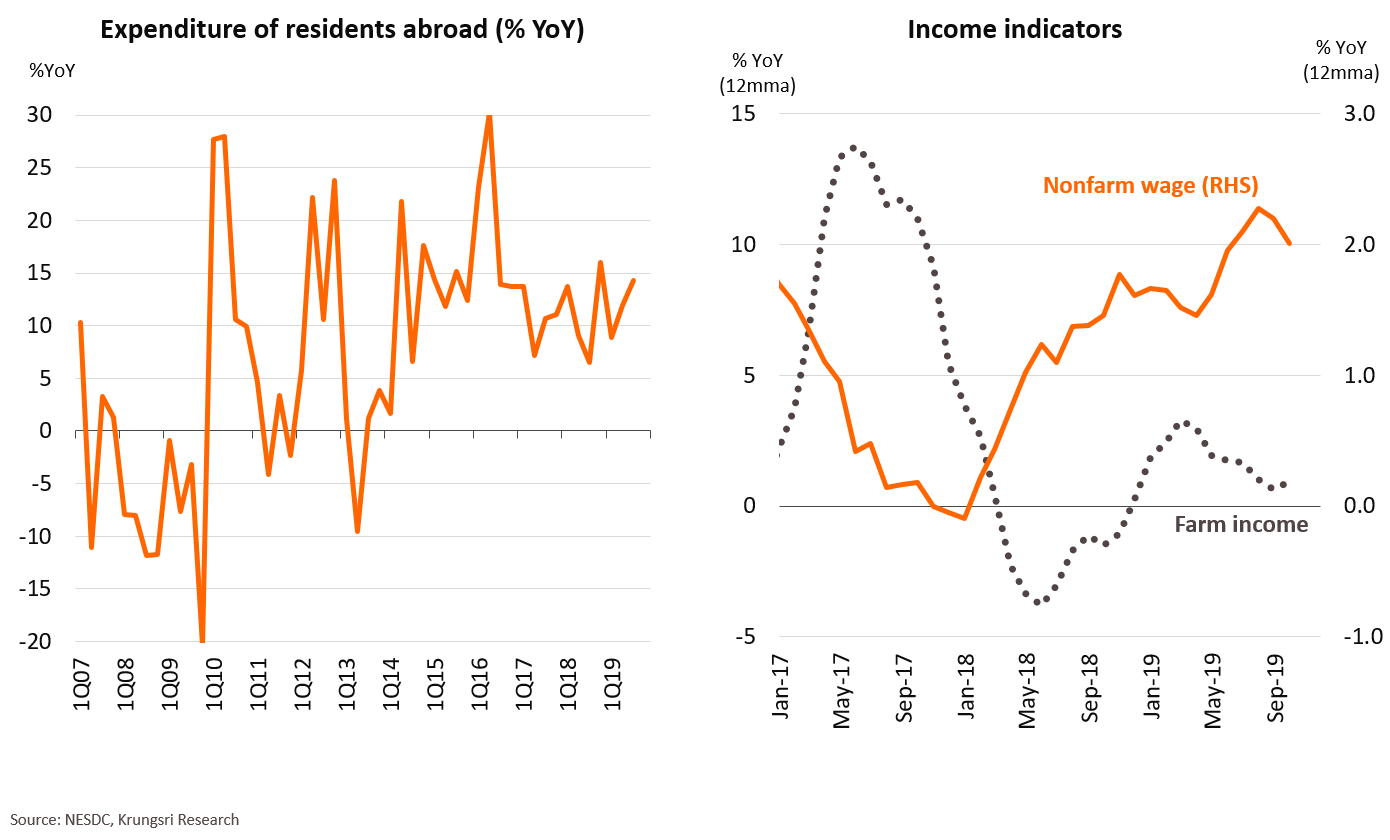

Consumption: Surge in overseas expenditure suggests firm purchasing power of middle-income earners

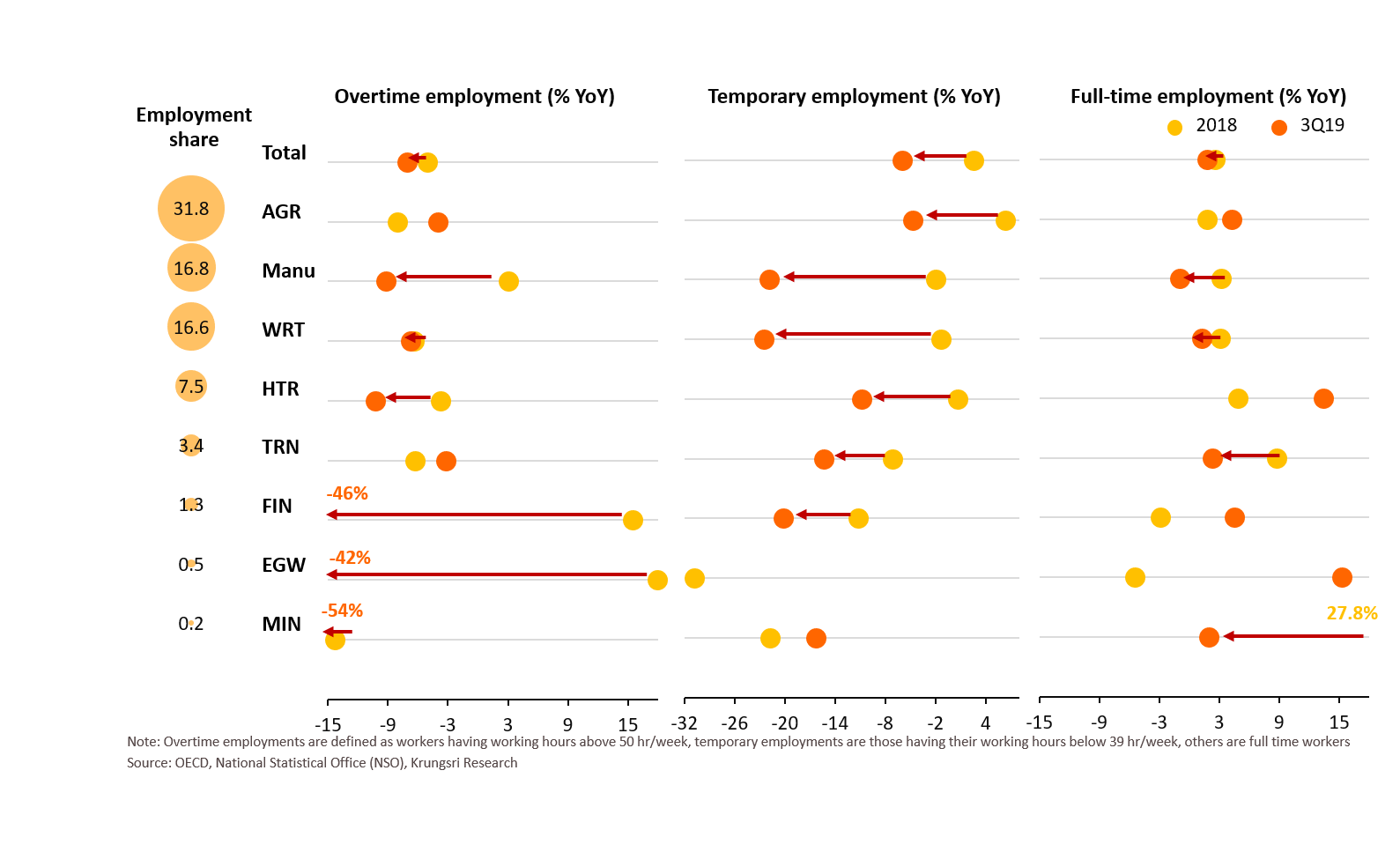

But weak exports will continue to hurt employment, as overtime & temporary jobs decline

The weaker exports will spread to domestic activities. There are more pronounced drops in overtime and temporary employment across industries. In manufacturing, overtime employment growth turned to -9.2% YoY in 3Q19 from +3% in 2018, while temporary employment fell deeper, by 21.9% in 3Q19 vs -1.9% YoY in 2018. For full-time employment, few industries have trimmed headcount; in manufacturing it fell to only -0.9% from 3.2%.

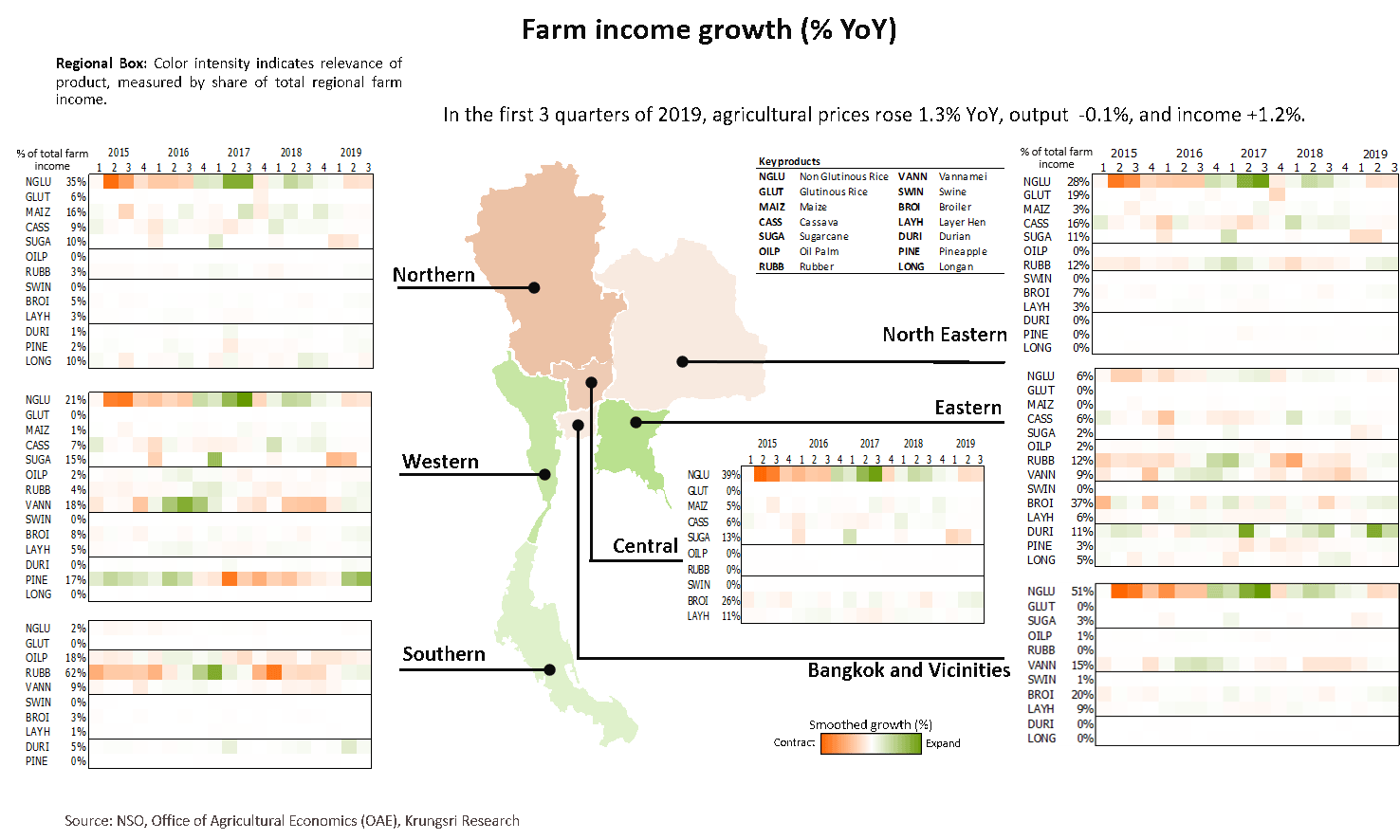

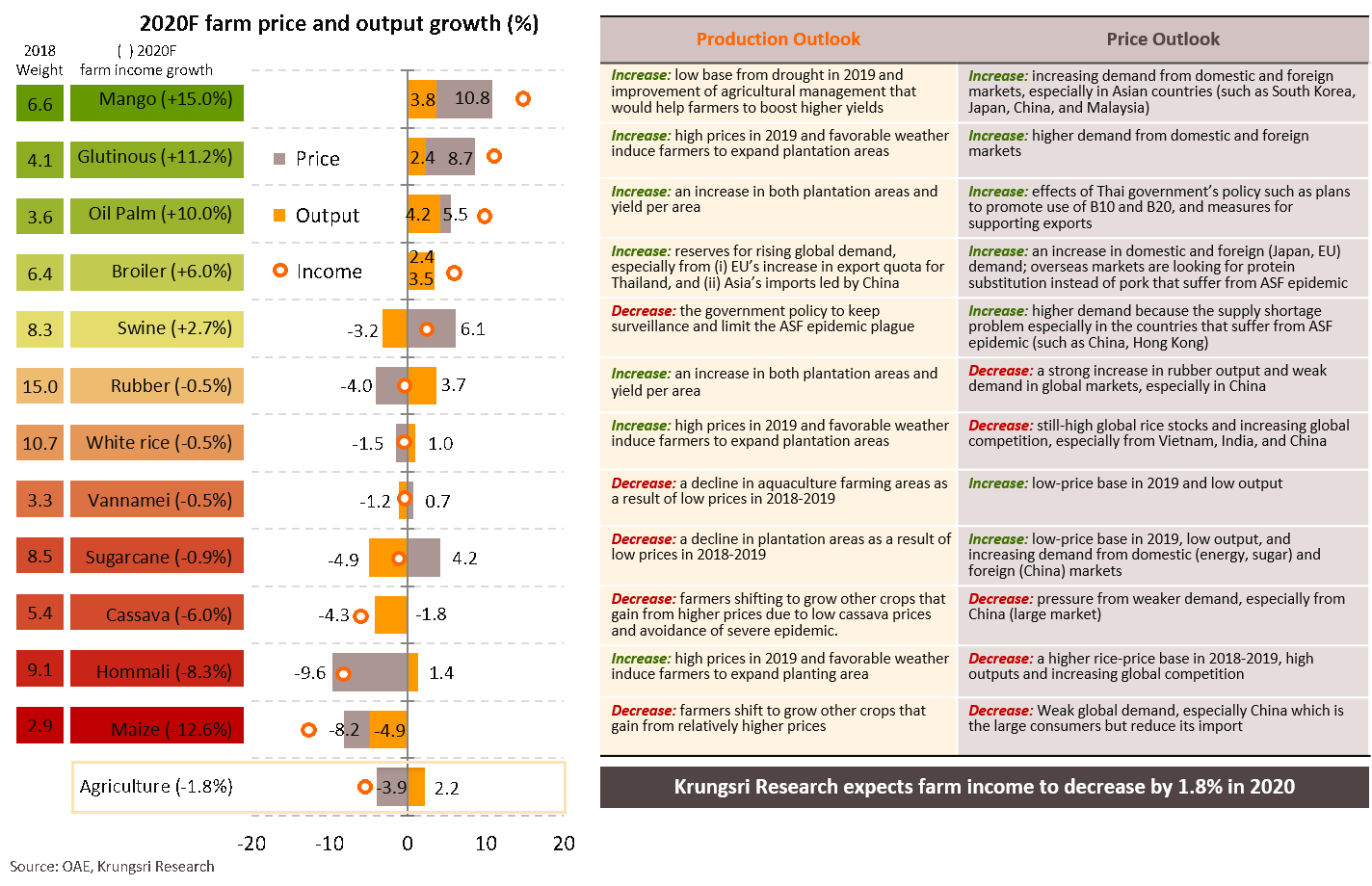

Farm income inched up but output is flat; improvement in southern region due to low-base effect

Outlook for farm income remains bleak as several major crops face unfavorable factors

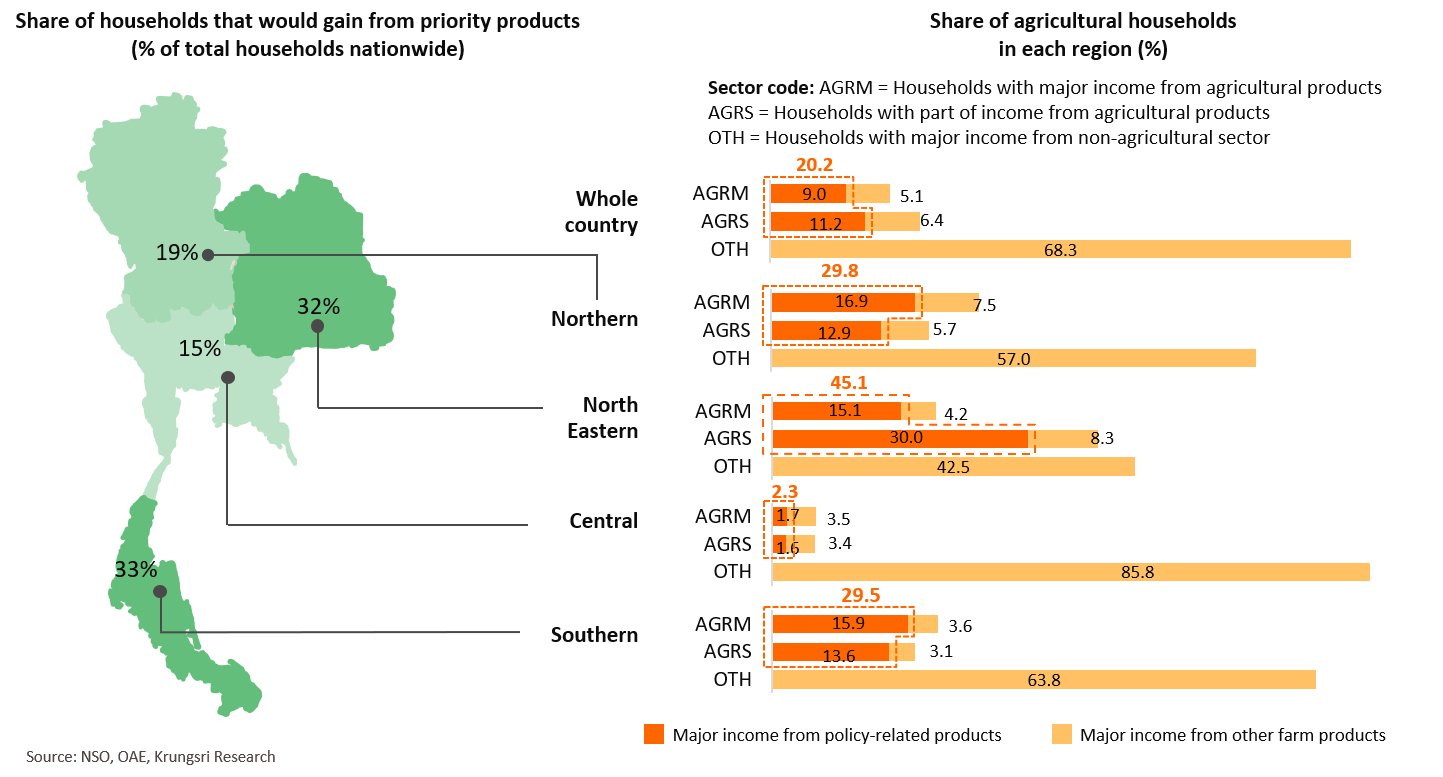

20% of Thai households would benefit from income guarantee scheme for crop farmers

The Commerce Ministry’s plan to guarantee income for crop farmers, including those cultivating rice, rubber, cassava, oil palm and corn, would benefit 20% of total households in Thailand (4.28m out of 21.4 m households). About 9% of households would be the biggest beneficiaries as most of their income are derived from the priority products. Northeastern and Southern regions will benefit the most, at 32% and 33% of total government spending under this scheme.

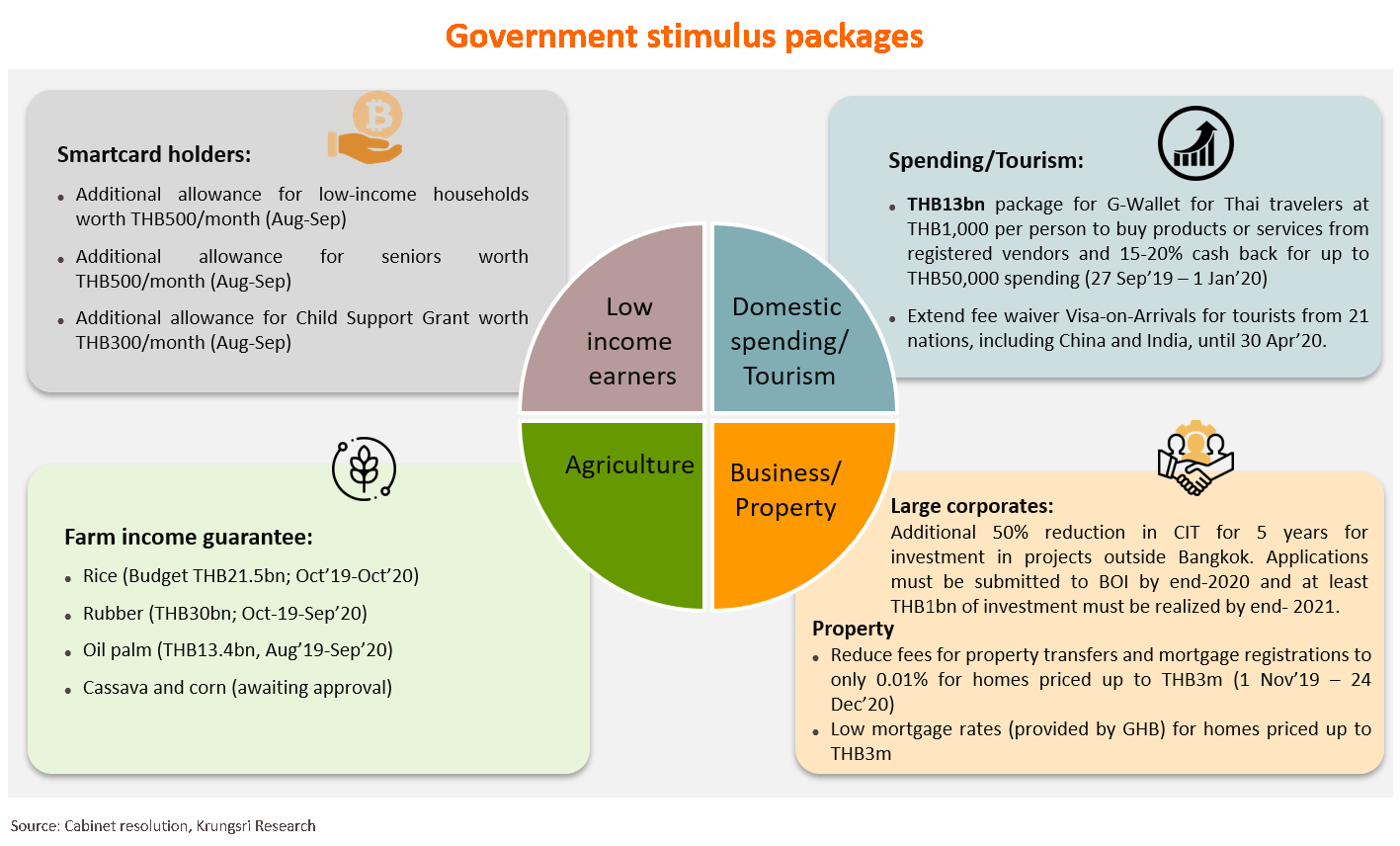

Recent stimulus measures may not be enough to stop export weakness from spilling over to domestic demand

Public spending: Potential of fiscal policy could help nurture growth during an economic slowdown

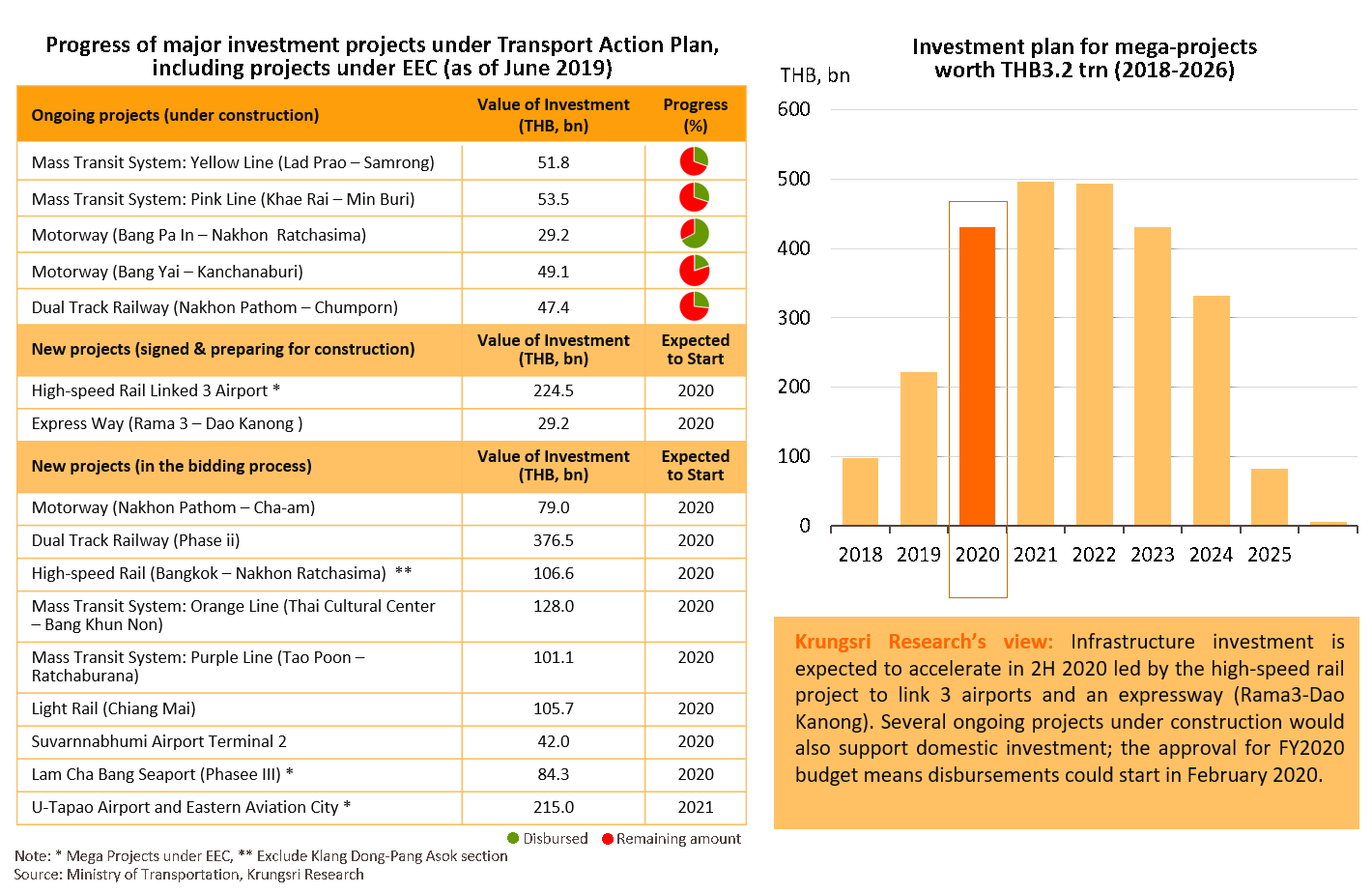

Public investment: Further progress in mega projects in 2H20, more projects to start in 2021-2022

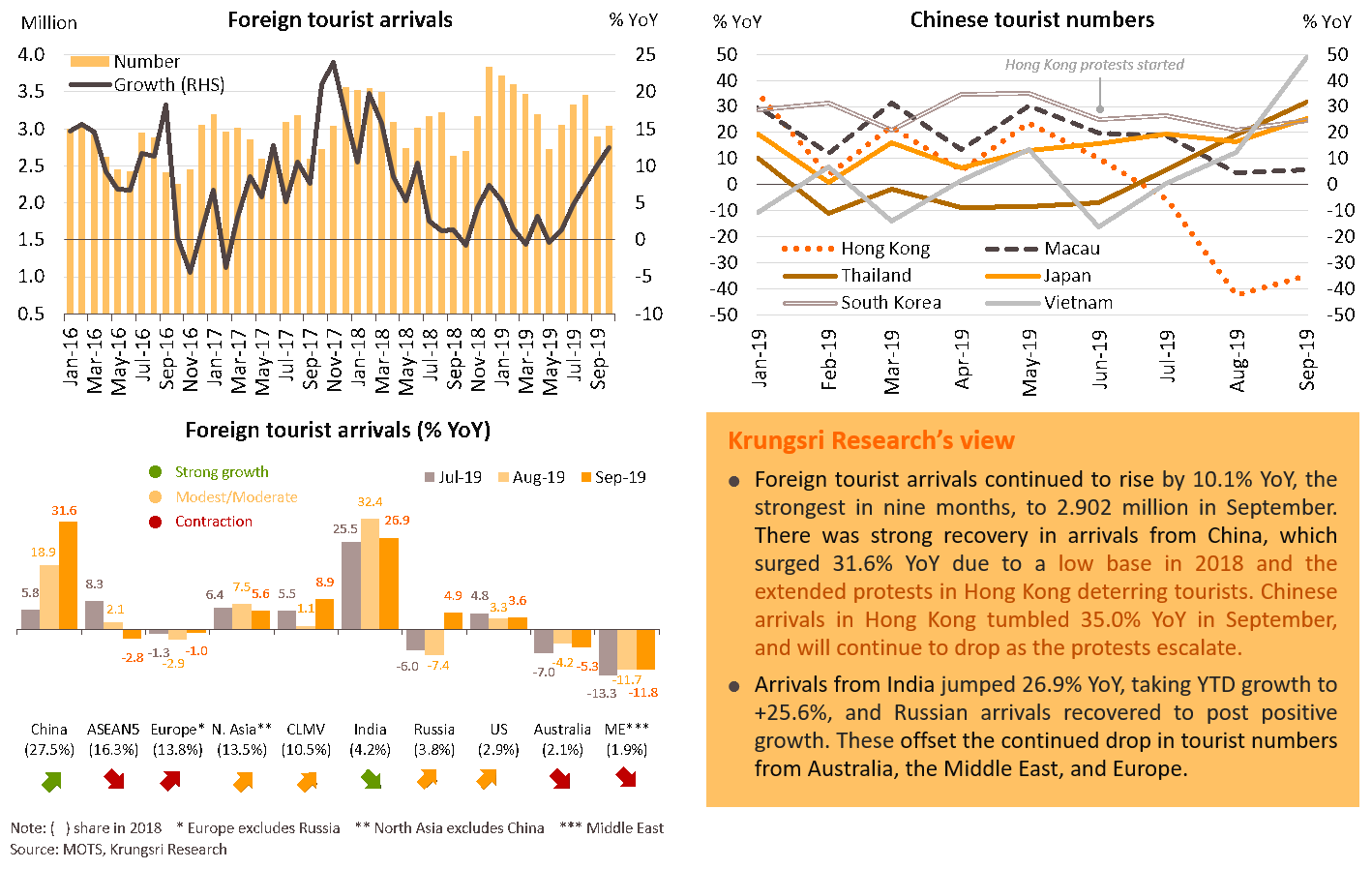

Tourism is recovering, led by Chinese tourists and windfall from Hong Kong protests

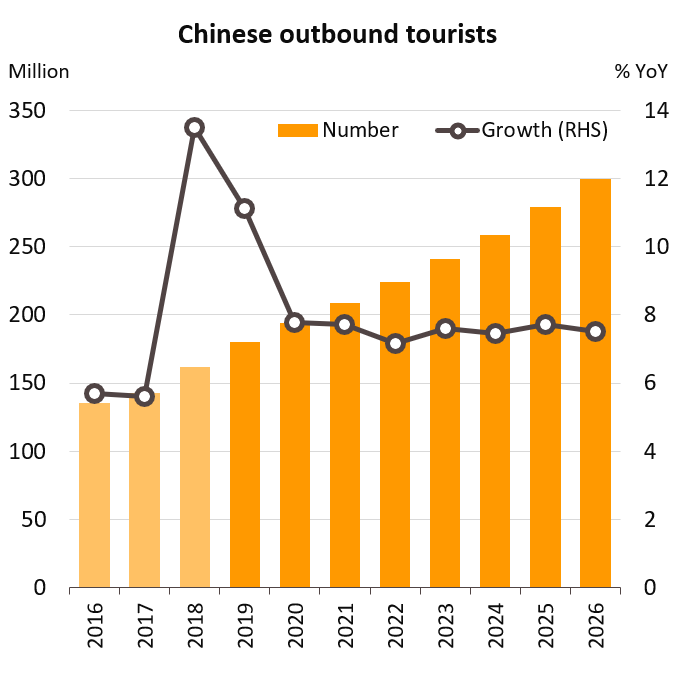

Strong prospects for China’s outbound tourism industry; Thailand can benefit from offering easier visa policy

|

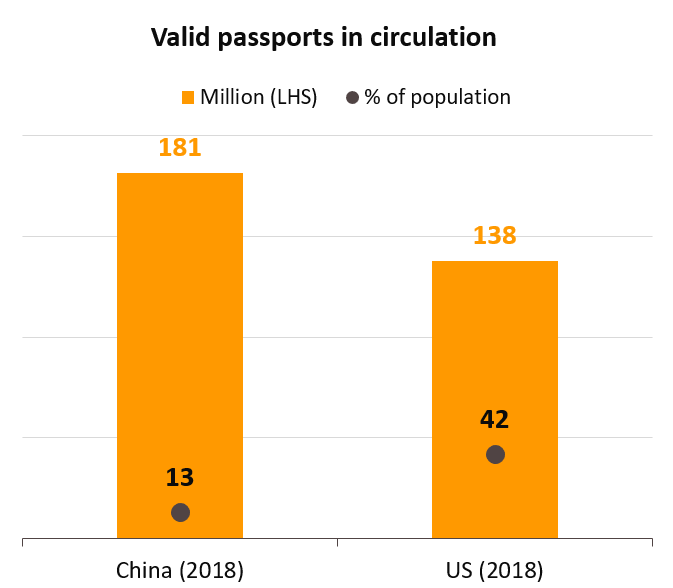

Only 13% of China’s population currently hold a passport compared to 42% of the US population. By 2027, the number of passport holders in China is expected to reach 300 million or 20% of the population, according to the World Tourism Organization (UNWTO). In addition, the combined share of middle-income population in second- and third-tier cities will jump to 76% in 2022 from 58% in 2002, according to McKinsey. This segment will generate first-time travelers, and Thailand is a relatively cheap tourist destination.

|

|

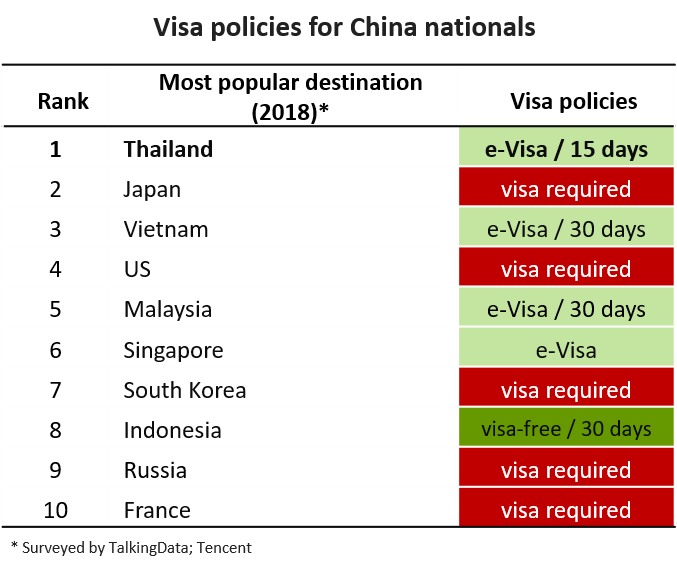

Even though Chinese tourists tend to explore more luxurious destinations such as Europe and Americas, they are still subject to strict visa restrictions in many countries. But among the most popular tourist destinations for Chinese travellers, Thailand has the advantage of easier access. Specifically, South Korea and France offer visa-free access to nationals of more countries than Thailand, but Chinese tourists still require visas to travel there.

|

|

|

|

Strong prospects for China’s outbound tourism industry; Thailand among the biggest beneficiaries

|

The China Outbound Tourism Research Institute (COTRI) forecasts the number of Chinese outbound tourists would reach 180 million in 2019 and 300 million by 2026.

|

|

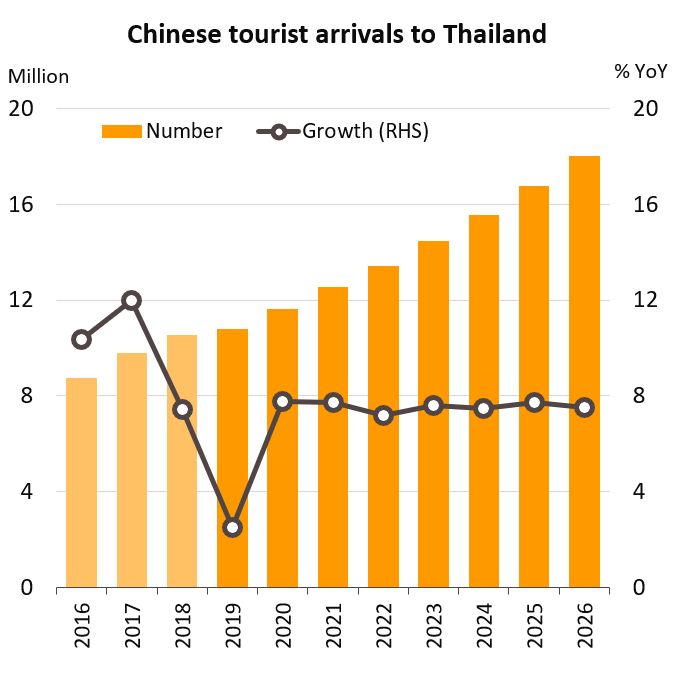

Assuming Thailand continues to attract 6% of the total number of Chinese outbound tourists, the number of Chinese arrivals in Thailand could reach 18 million by 2026. The assumption is conservative compared to 6.6% p.a. average growth in 2016-2018.

|

|

|

|

Source: China Outbound Tourism Research Institute (COTRI), UNWTO, MOTS, Krungsri Research

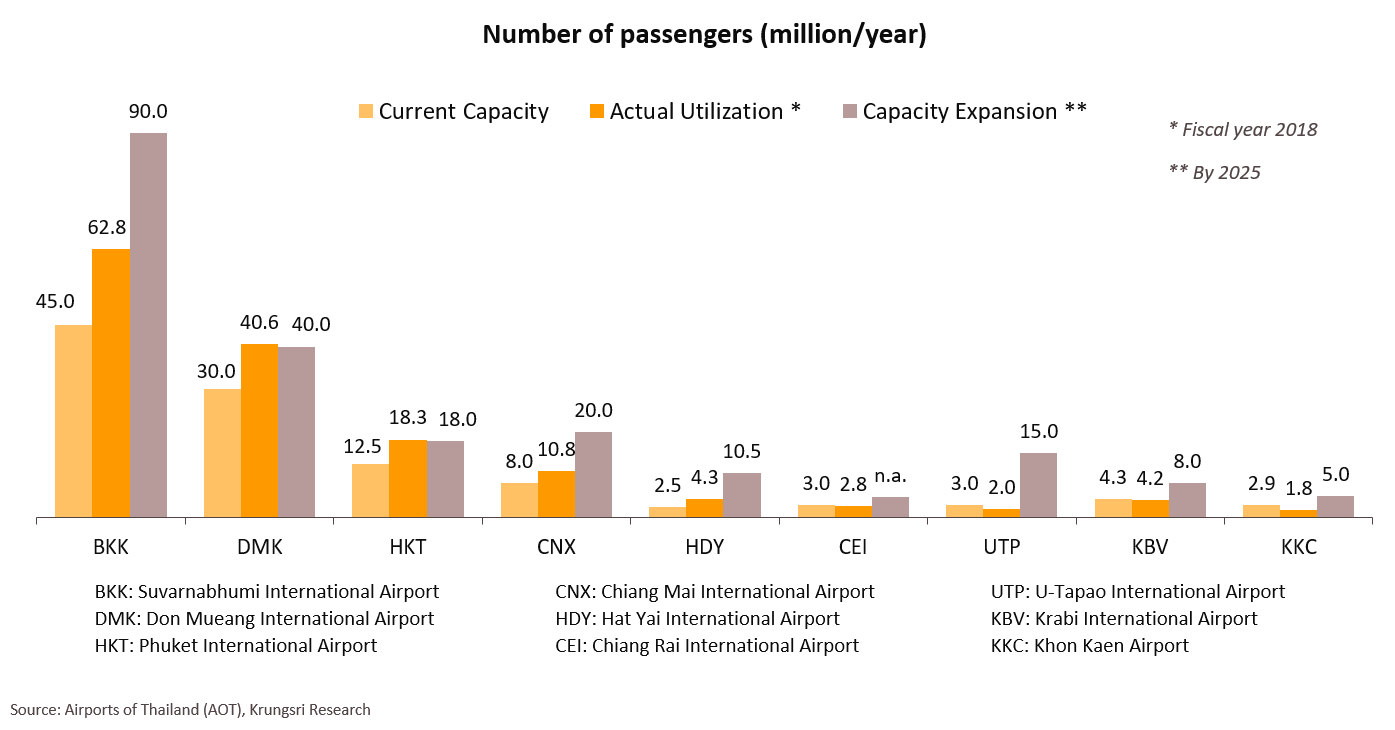

Thailand is struggling to cope with the influx of travellers due to tight airport capacity

The nation’s airports are processing more passengers than they are designed to handle. To address this, the government plans to upgrade infrastructure, including adding new terminals at the two international airports in Bangkok, as well as expand U-Tapao airport near Pattaya. That would increase combined capacity to about 145 million passengers per year by 2025, from 75 million currently.

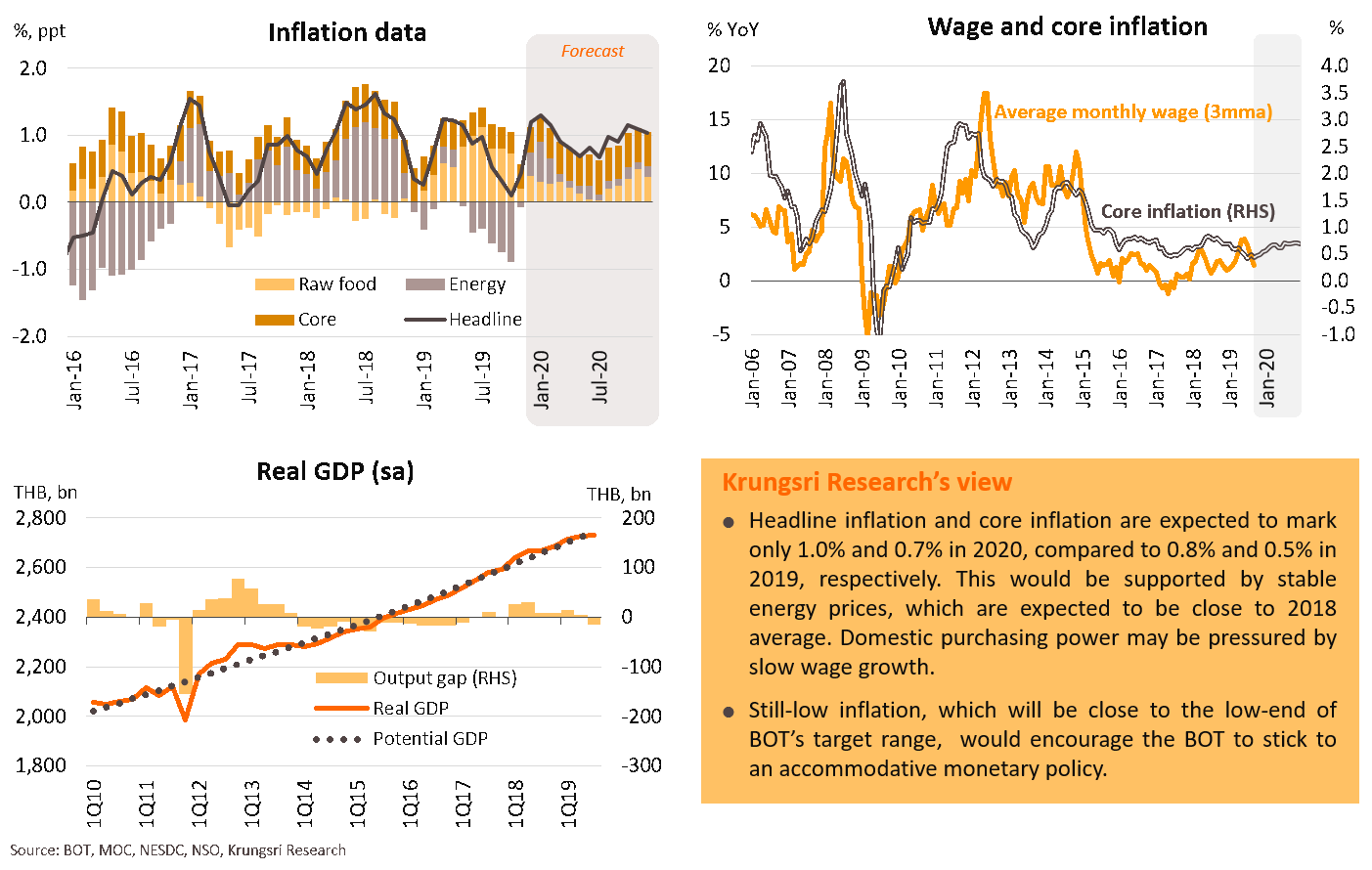

Inflation to remain at low end of BOT target given slow recovery in domestic demand and low energy prices

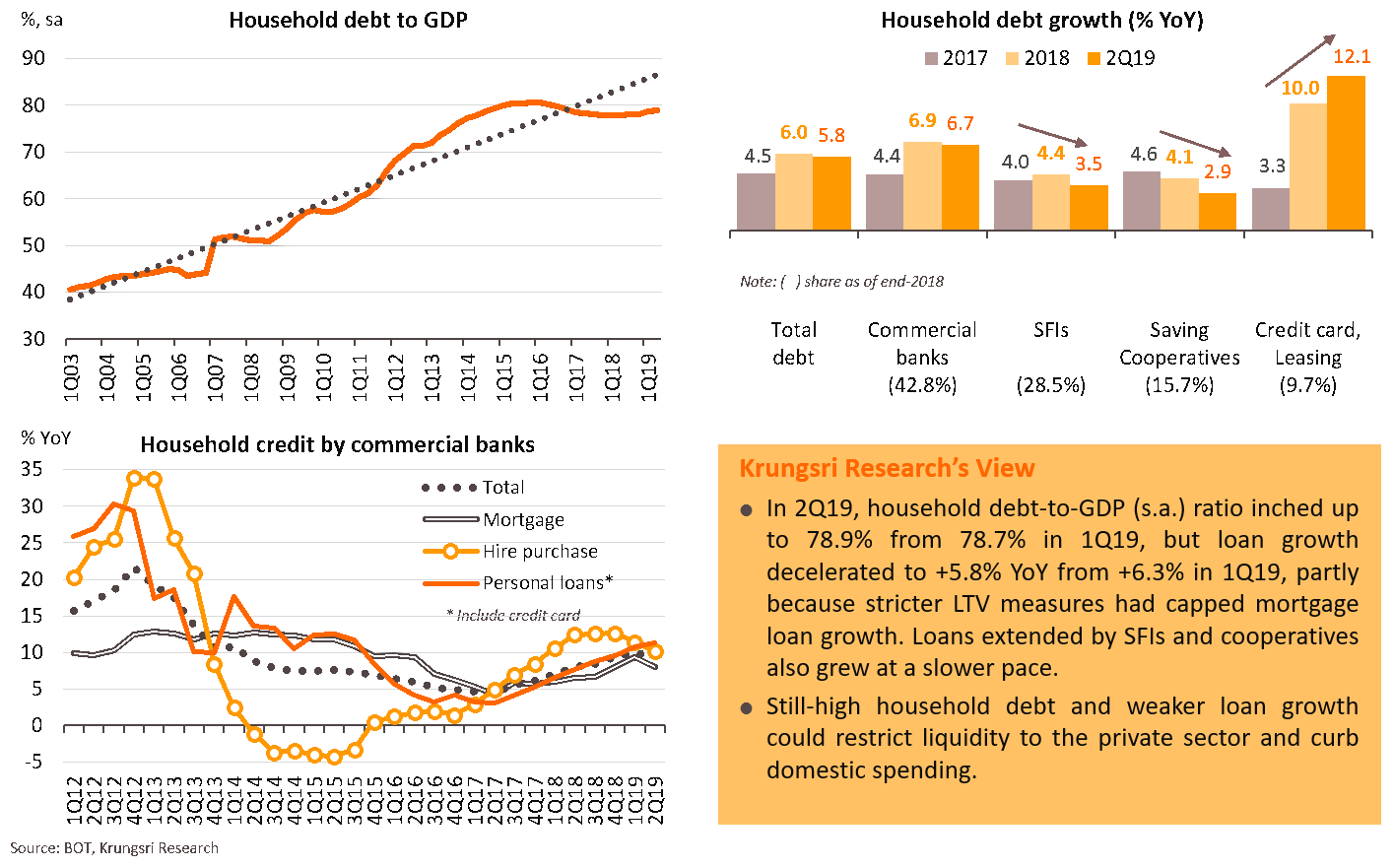

Still-high household debt and slower loan growth could curb liquidity to private sector

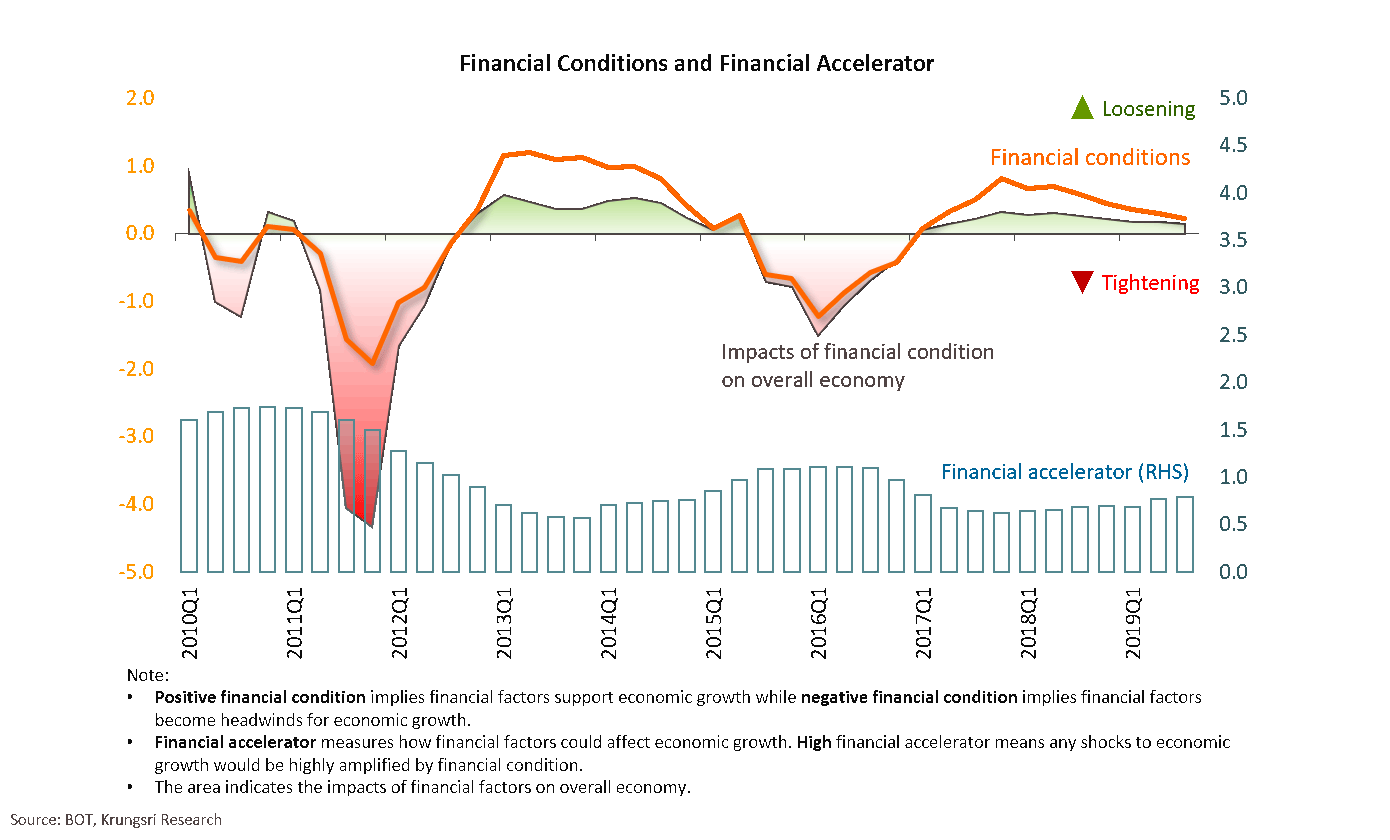

Financial conditions are much less supportive of economic growth

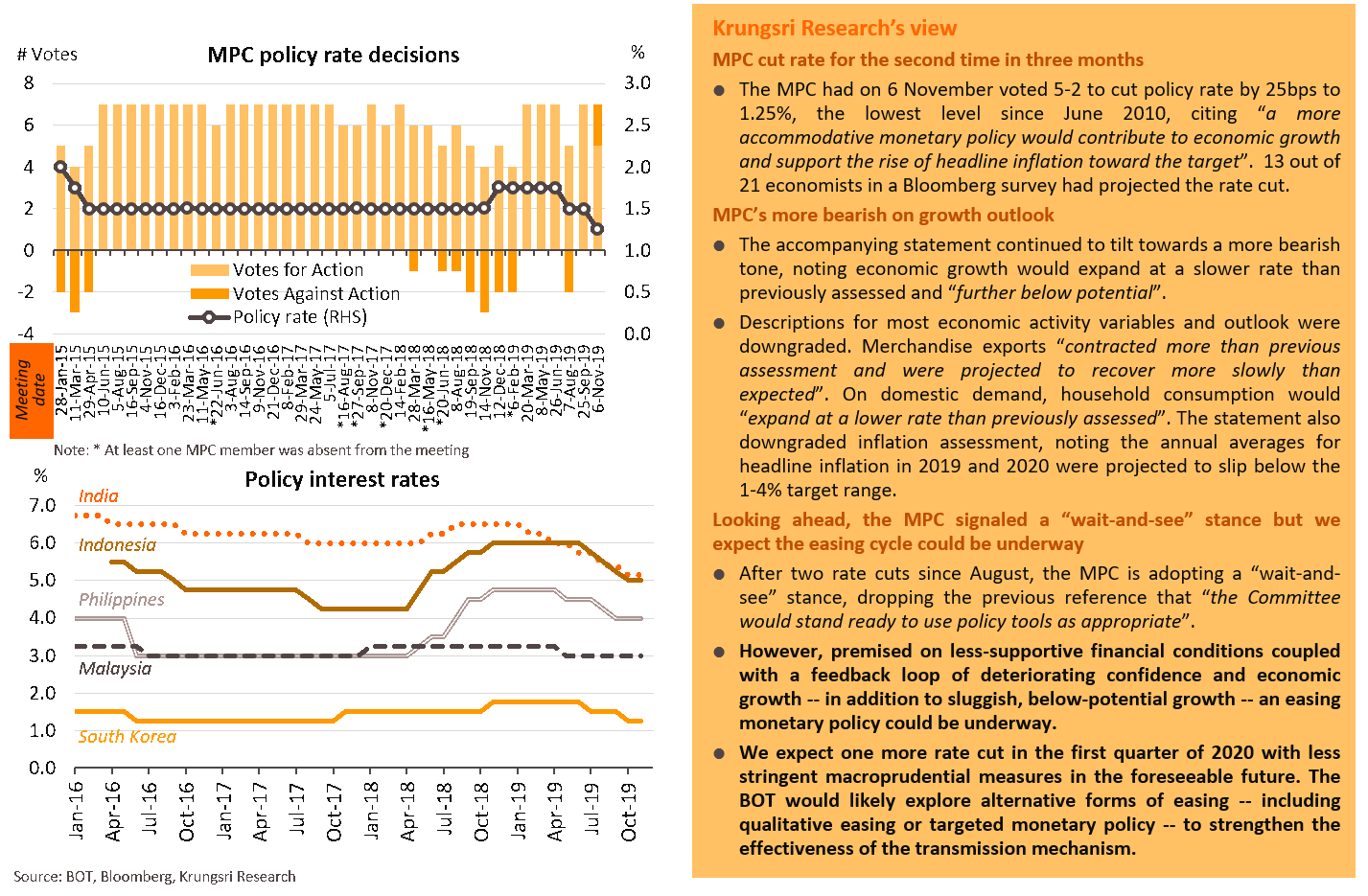

Monetary policy: Easing cycle still underway with one more rate cut and targeted policy

Key risk factors

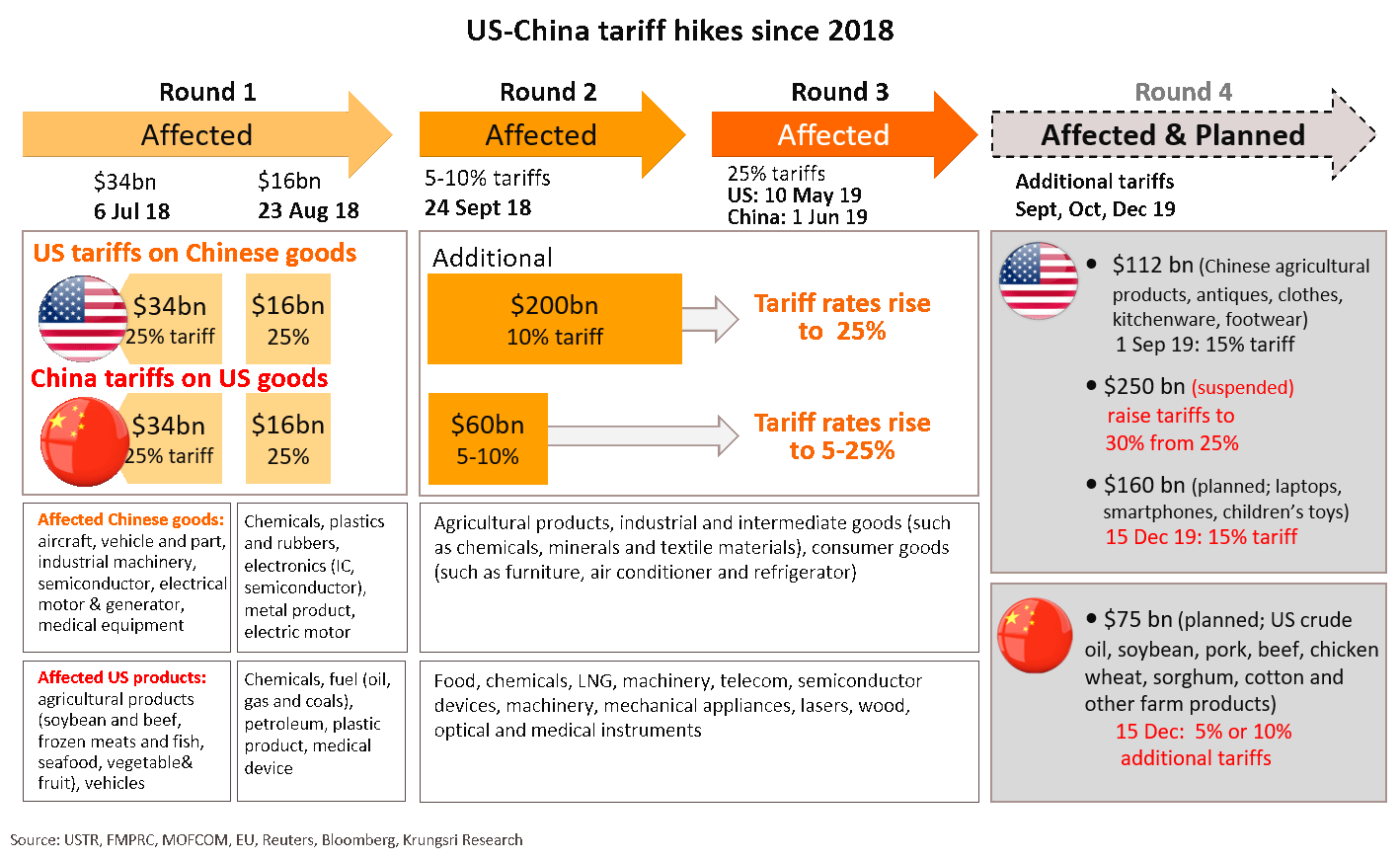

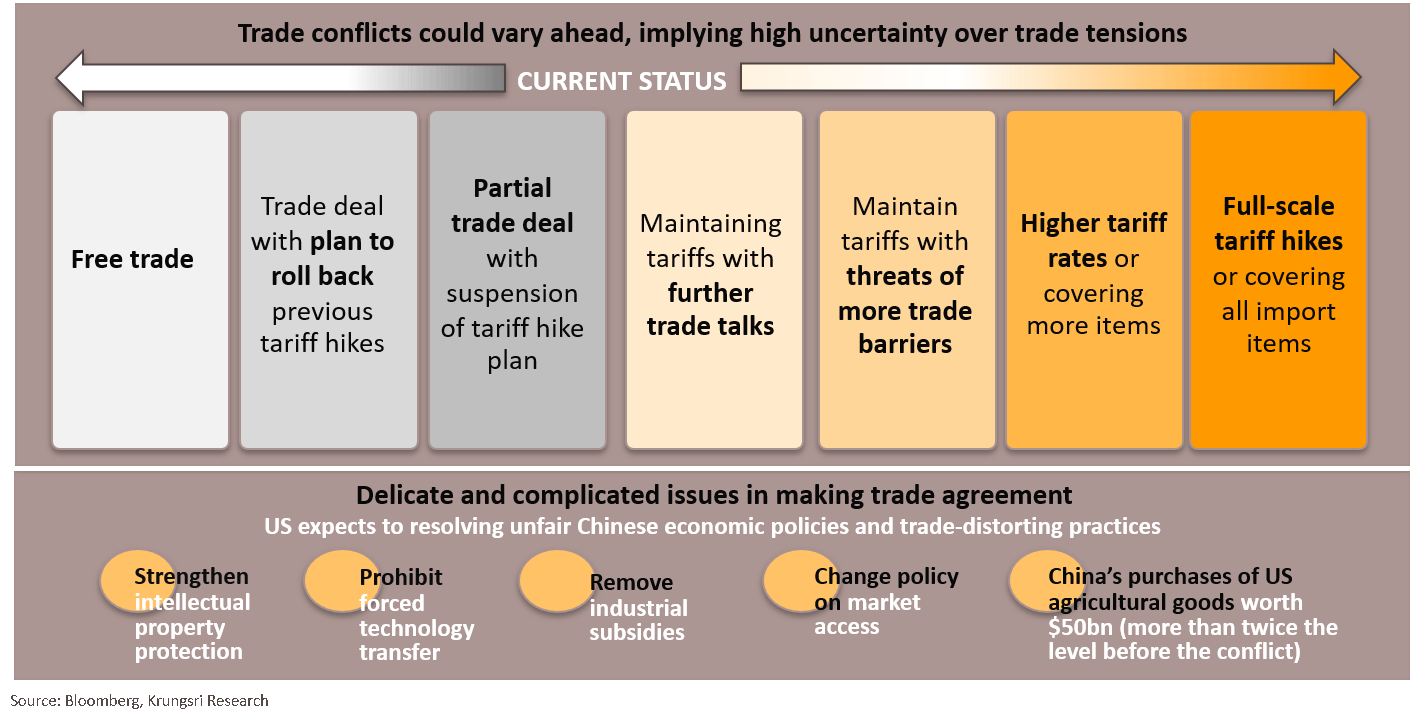

Risks to trade: Despite trade talks, US and China tariff hikes since 2018 are hurting global trade

Uncertainty in trade tension could increase risks to business expansion, relocation plans, and overall growth

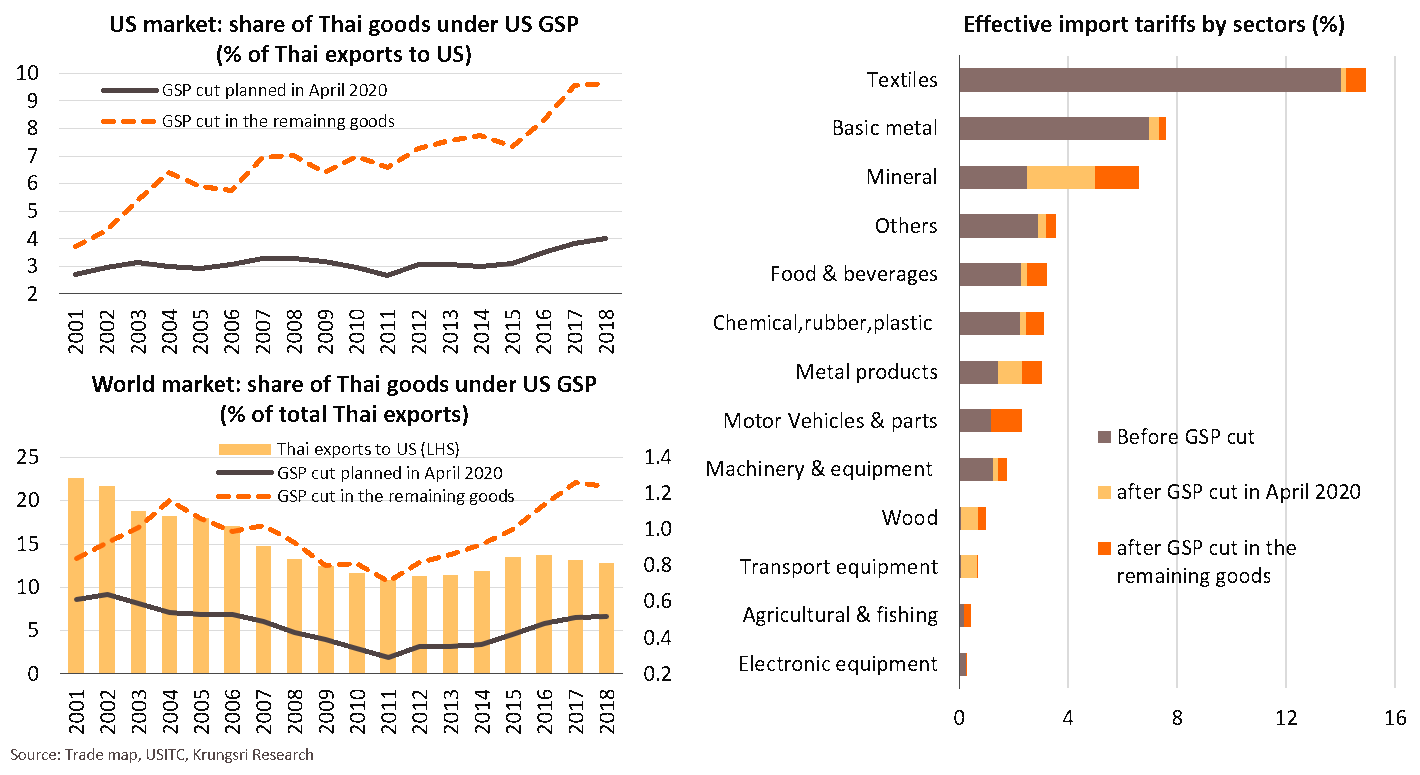

US plan to end GSP benefits for Thai goods in 2020 will hit 4% of Thai exports to the US, 13.6% in the worst case

The plan is set take effect on 25 April, 2020. It would cover 573 items (40% of 1,485 items eligible for GSP in 2018). Thailand exported 355 of the 573 products on the lists which accounted for 4.0% of Thai exports to the US in 2018, up from 2.7% in 2011. In the worst case, if the US cuts GSP benefits for all Thai goods, the incremental share of affected products would be 9.6%. Exports of these goods to the US and world markets have surged in the past few years, implying risks to Thai exports. If the US ends GSP benefits for all Thai goods, sectors that would see the biggest increase in tariffs would be mineral, motor vehicles & parts, metals, and textiles.

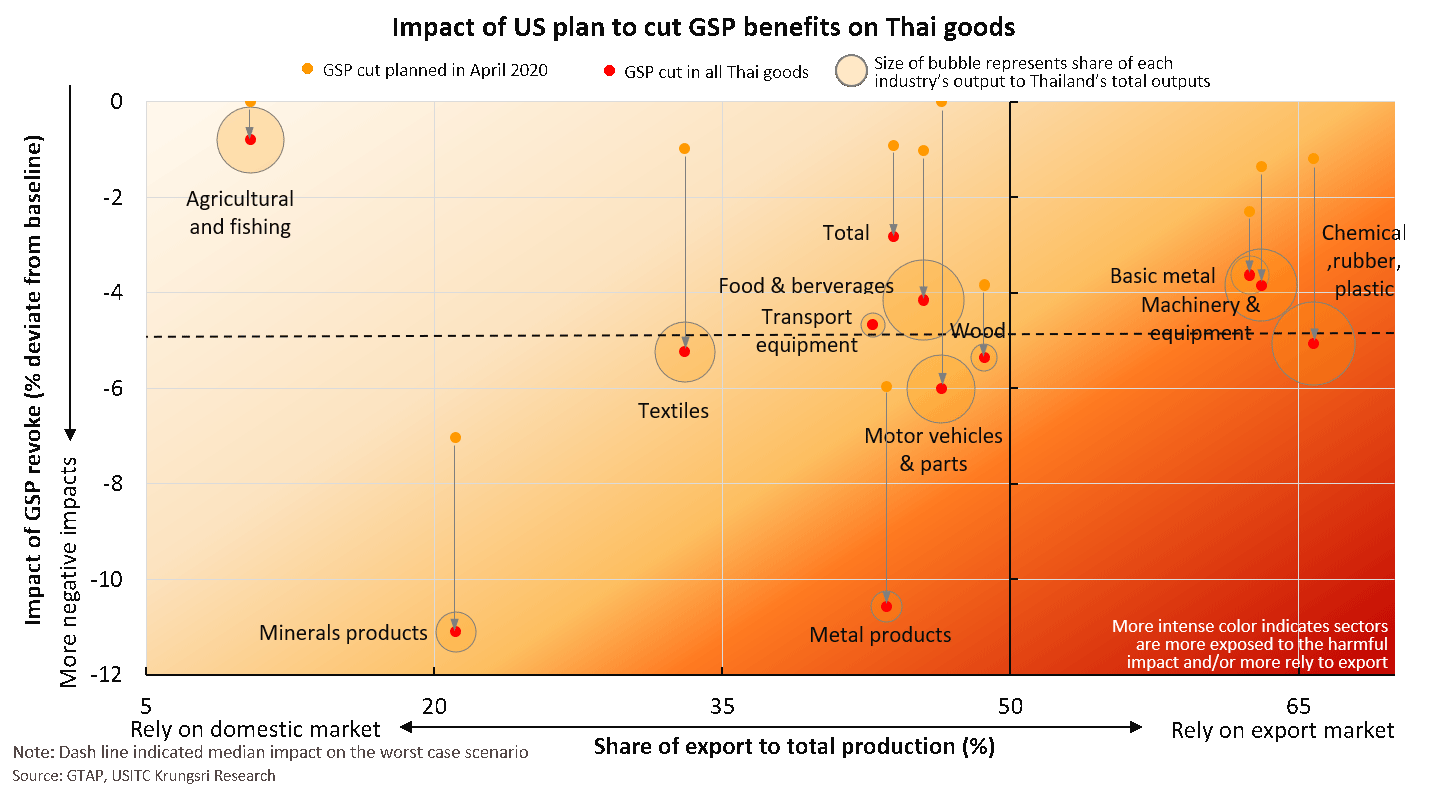

Limited impact on overall Thai exports, but high risk to exports to the US in the worst case scenario

The plan to suspend GSP on Thai goods would have minimal impact on overall Thai exports (less than 0.01%), but Thai exports to the US could shrink by 0.9% from the baseline. The largest impact (more than -5% from baseline) would be on mineral products (such as ceramic), metal products (such as iron and steel, screws and bolts), and transport equipment (such as motorcycles ). In the worst case (i.e. end GSP benefits for all Thai goods), Thai exports to the US could shrink by up to 1.9%, led by motor vehicles & parts, mineral products, metal products, textiles, and chemicals & plastics.

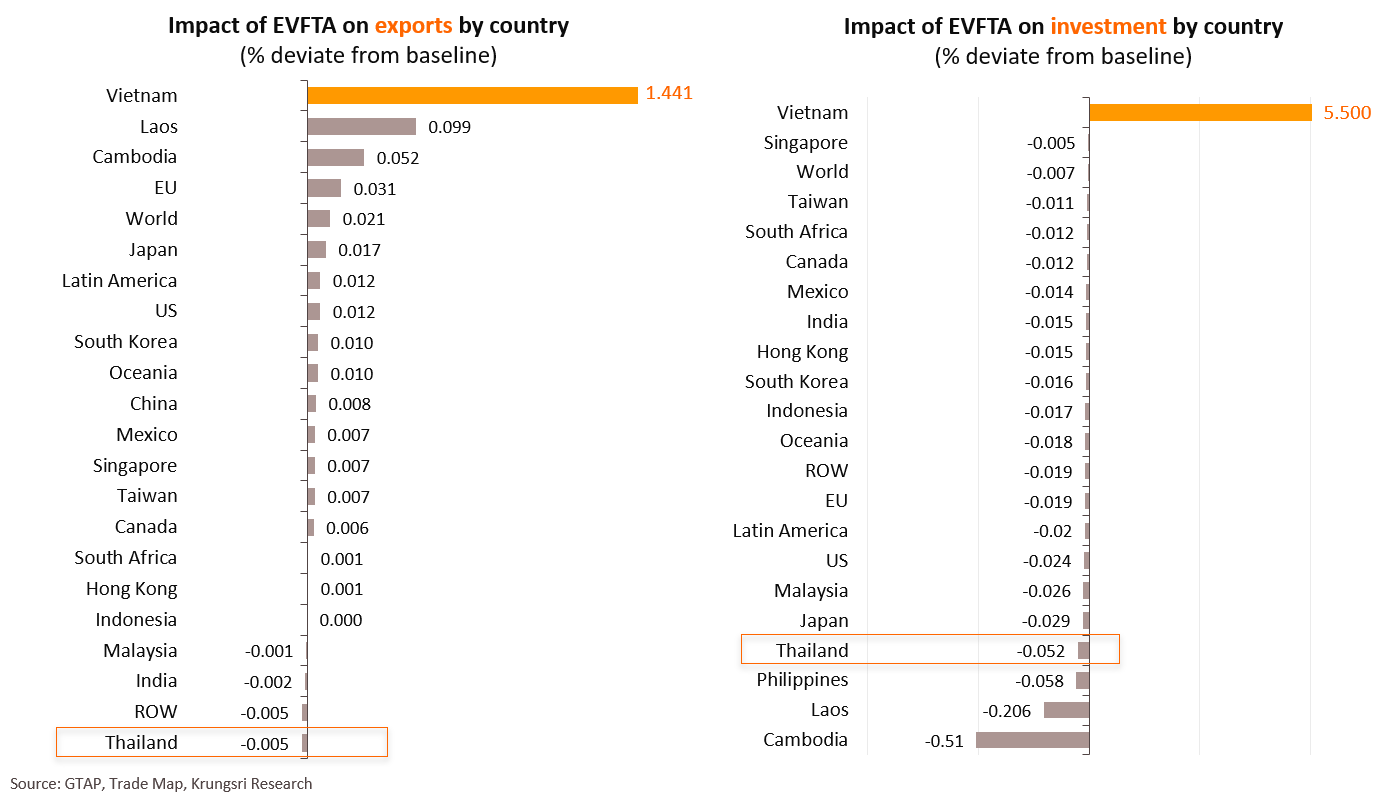

EU-Vietnam FTA: Thailand could be one of key countries to lose exports and investment

The Free Trade Agreement (FTA) between the European Union and Vietnam, set to take effect in 2020, includes near-complete removal of tariff barriers, reduction of non-tariff barriers, and improved access to Vietnam’s services market. Due to close-to-zero tariffs between Vietnam and the EU, there is larger risk to Thailand’s major export sectors to both countries and investment activity in the country. Our study suggests Thailand would be one of the biggest losers of this FTA. The risks could be even higher when Vietnam start to enhance its competitiveness.

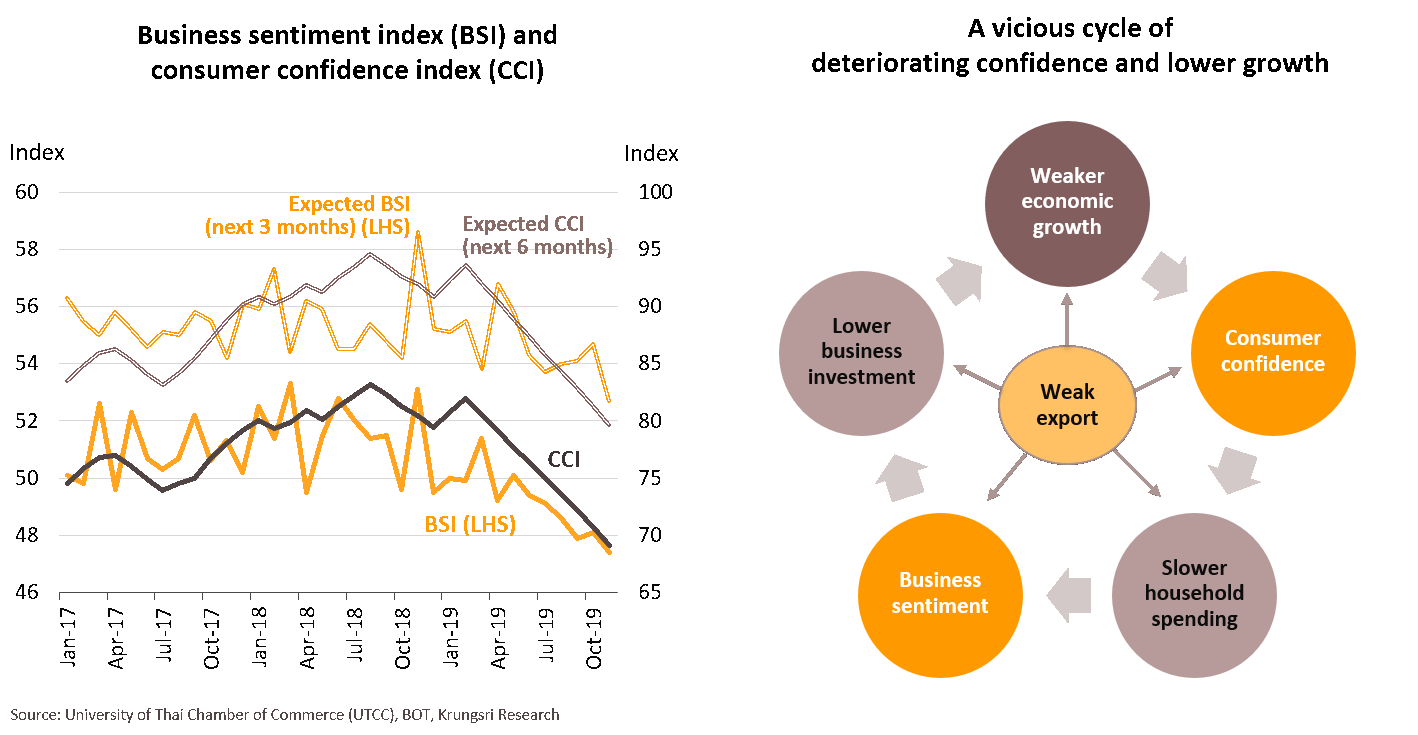

Weaker confidence could create a vicious cycle of slower spending, lower investment and weaker growth

The export weakness would not only adversely affect private investment and consumption but also hurt business sentiment and consumer confidence. If the recent spate of economic stimulus policies fail to revive confidence, Thailand could slip into a vicious cycle of slower consumer spending, lower business investment and weaker economic growth.

Policy risks: several measures might become counter-cyclical economic policy during the recovery period

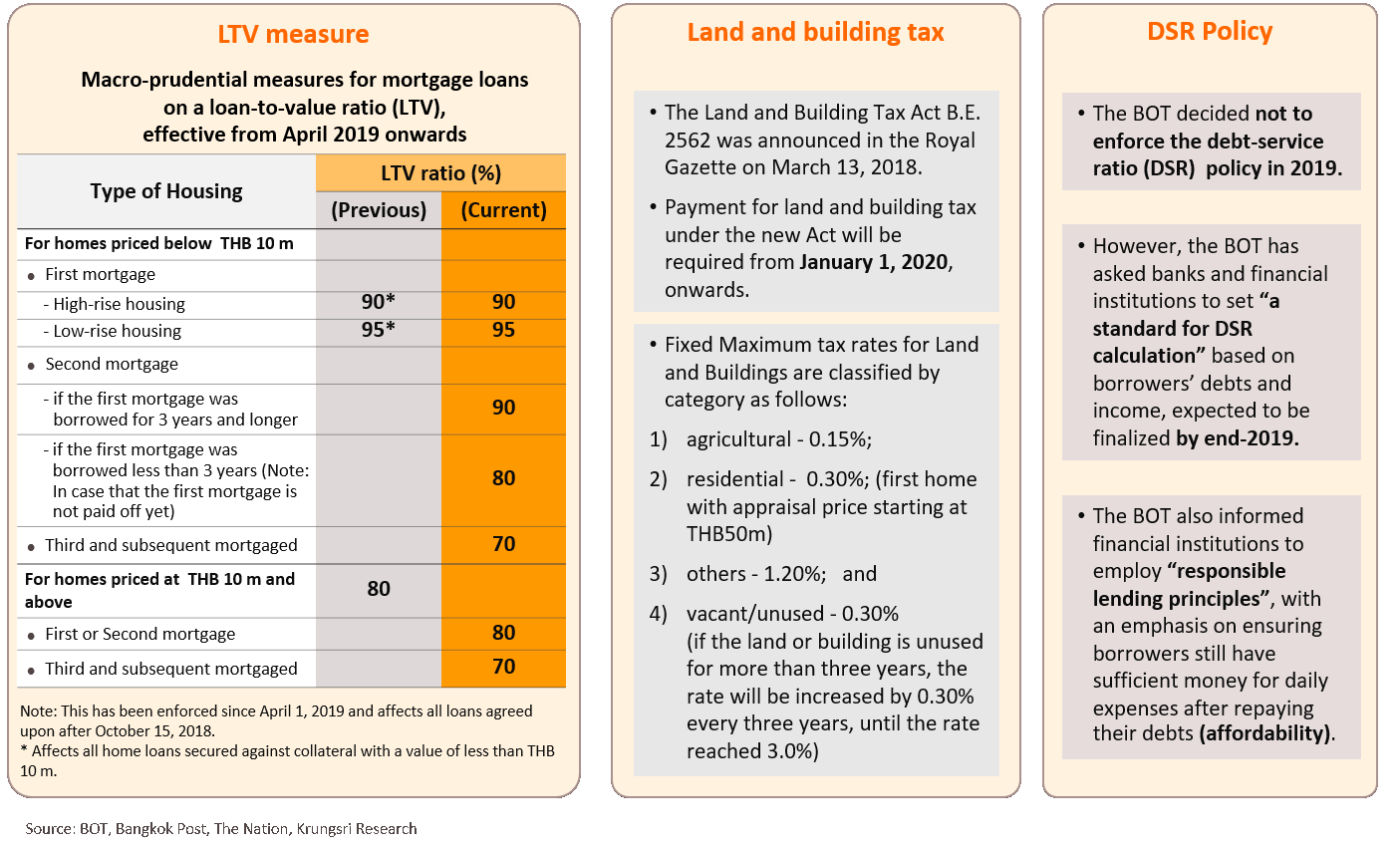

Excess housing supply remains a key concern

As private investment in dwellings account for up to 56% of private construction (as of 2018), it would have an impact on investment in machinery and equipment. Hence, the housing market has a large influence on the direction of domestic investment and resulting risks to the overall economy. However, total housing supply in BMR has continued to rise to a record high. Although demand reached a 5-year high in 2018, that was partly due to front-loaded effect of stricter LTV measures announced in October 2018. Future demand is likely to slow down and may not be able to absorb the cumulative supply. And given weak domestic purchasing power and uncertain foreign demand amid a slowing global economy, the excess supply -- especially in the condominium segment – would continue to be a major concern in the next few years.

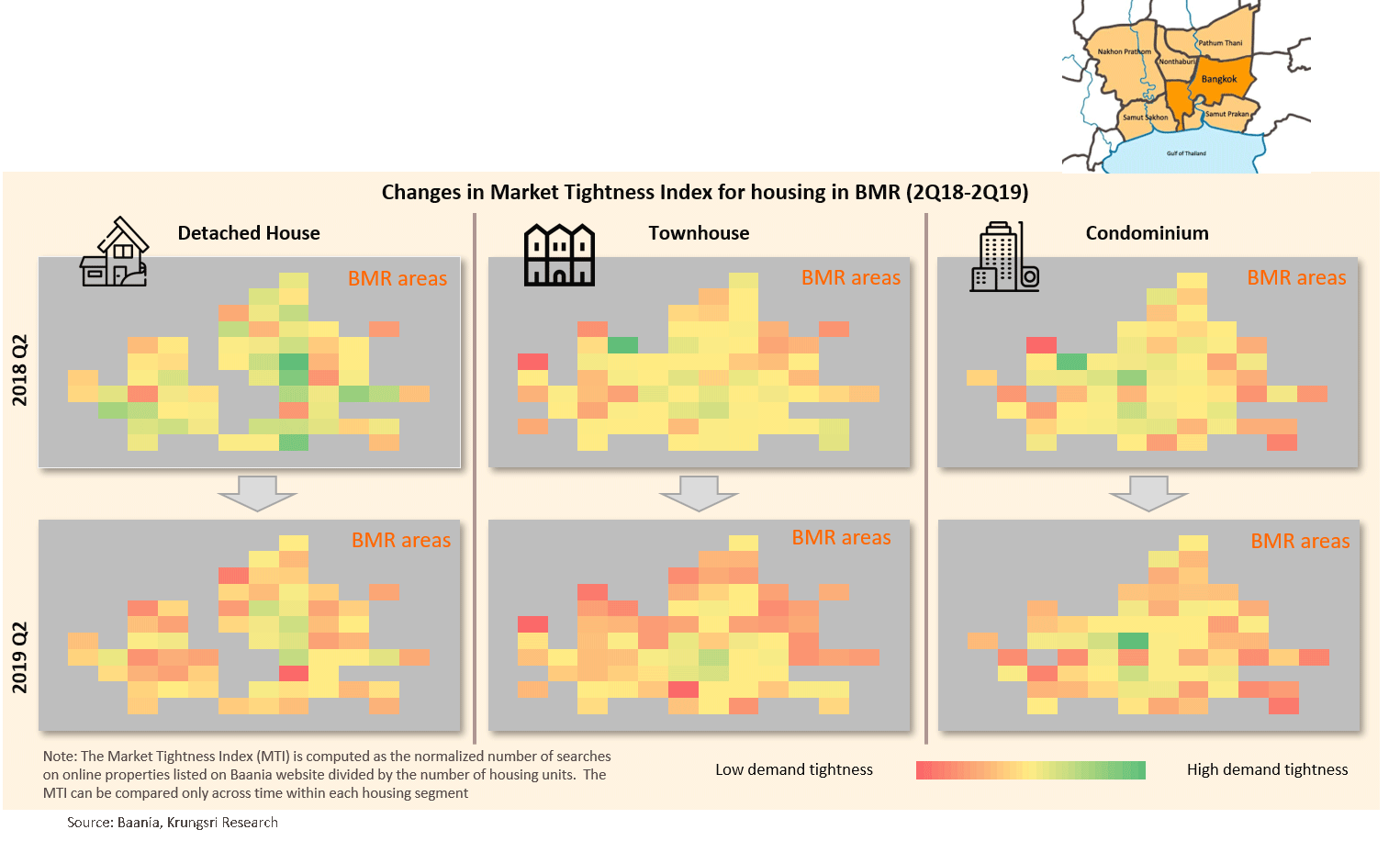

Market Tightness Index indicates slower demand in all housing segments in BMR

Krungsri Research’s Market Tightness Index, a proxy for potential housing demand, has declined since 2018. This has increased concerns over all residential segments in the BMR, that inventory could rise in the near future. The index has been declining for most of the 72 districts in the BMR. Red and orange colors indicate districts with low number of searches per housing units, implying lower potential demand in the future. Given the current weakness in economic activities, the housing market could see a larger oversupply.

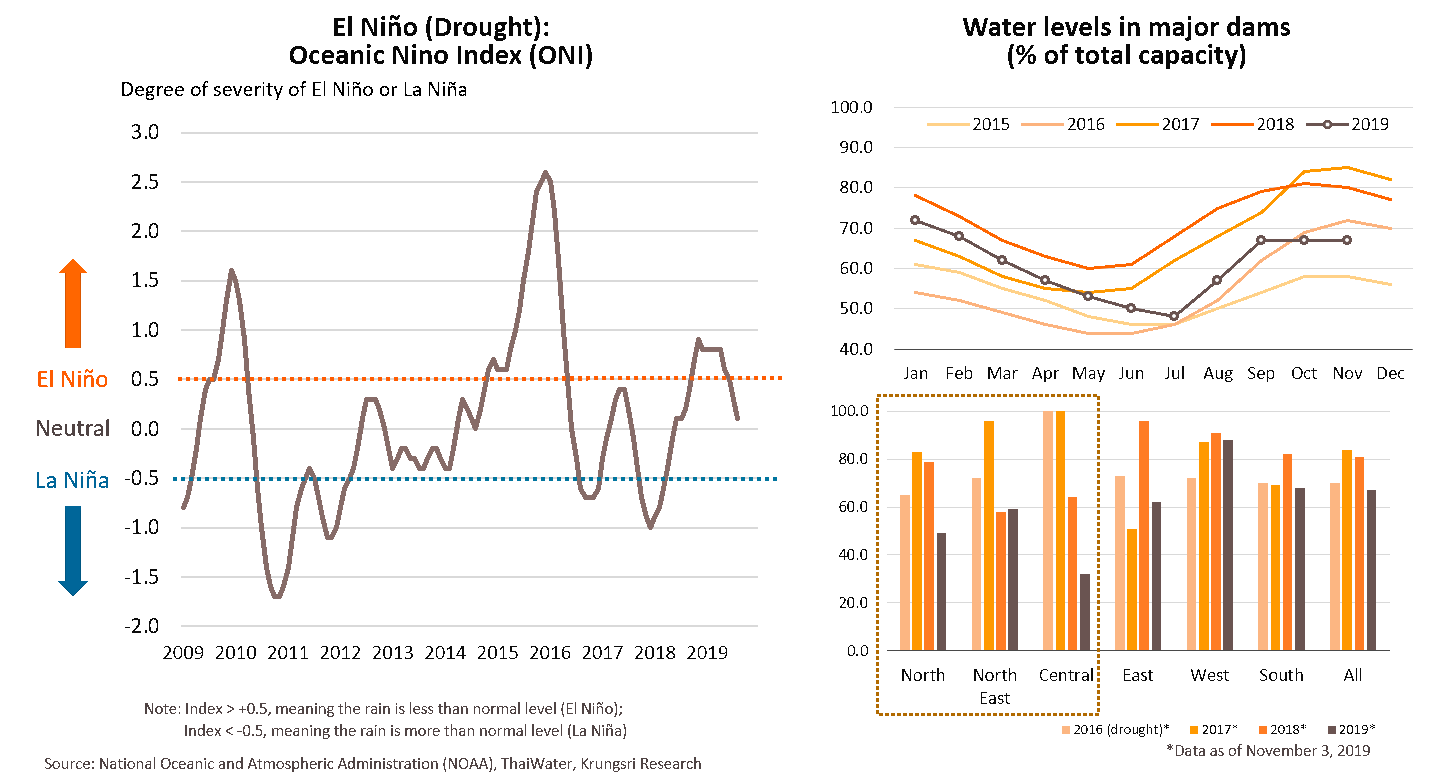

Drought risk as water levels in major dams drop to near 2016 crisis levels; might hurt purchasing power

Compared to the 2016 drought, the situation in 2020 might be a great concern. Even though the National Oceanic and Atmospheric Administration (NOAA) sees no signs of El Nino (vs strong El Nino in 2016), water levels in most major dams – especially in the North, Northeast, and Central regions -- are currently lower than in 2016. In the central region, levels in major dams are far below 2016 levels and the irrigation department could have limited room to release water from dams in the North (currently close to 2016 levels). Farm output could be damaged in the first half of 2020 (or before the regular rainy season in the third quarter of the year). This could dampen purchasing power and consumer confidence.