Executive Summary: Vietnam is likely to recover from the COVID-19 pandemic faster than regional peers and growth should rebound to its annual rate of 6.0-7.0% in the medium to longer term

Vietnam: An overview

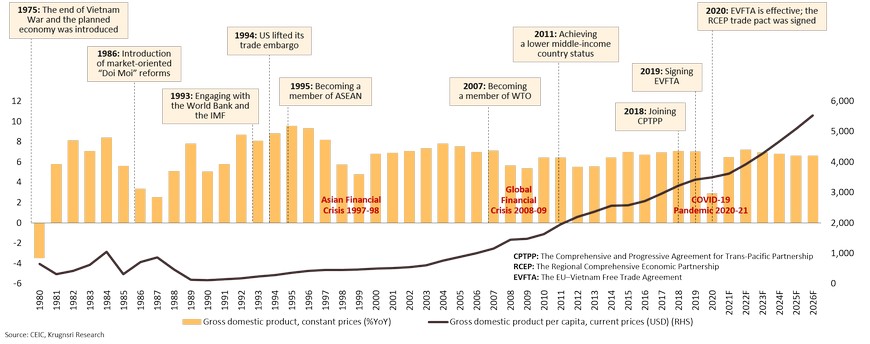

Vietnam has enjoyed prolonged periods of high economic growth and it aims to become a high-income developed country by 2045

Following its first grand market-orient reforms known as the Doi Moi in 1986, the agriculture-based and relatively closed economy has been transformed to become FDI-driven manufacturing and export-oriented. As a result, the country has enjoyed sustained periods of high economic growth and achieved the lower middle-income status in 2011. And, in 2019, the GNI per capita reached USD1,952.64 (2010 price), according to the World Bank. On the back of trade liberalization and economic modernization, this development has paved the way for Vietnam’s sizeable domestic market to flourish.

Medium-term macro forecasts: High growth will continue

Recent Economic Developments

Strong growth will be sustained in the long term supported by FDI-led manufacturing sector, exports, and favorable fundamentals

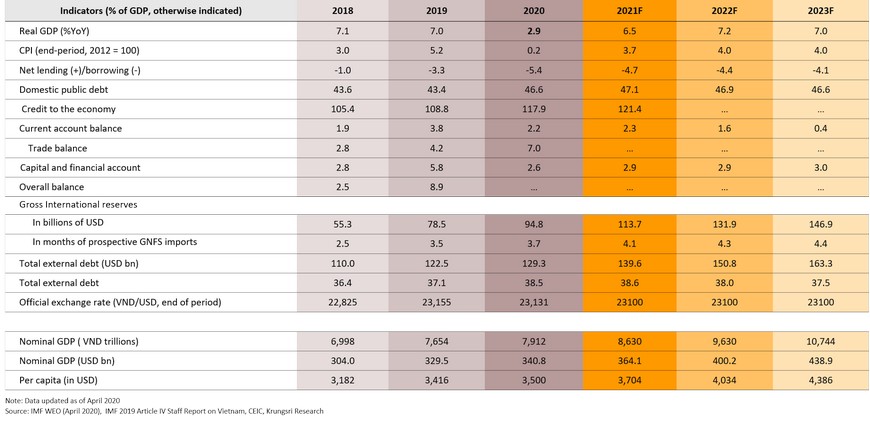

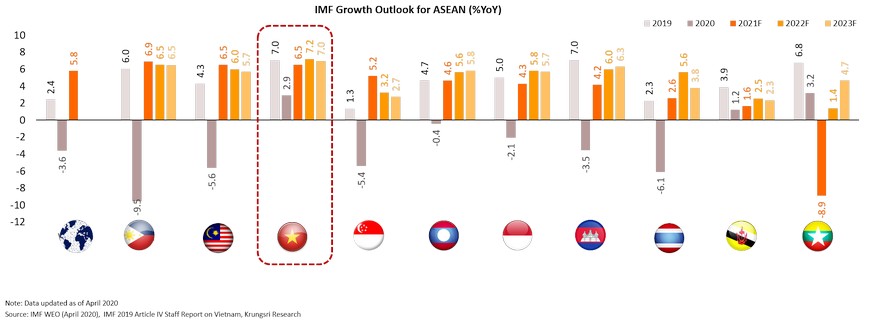

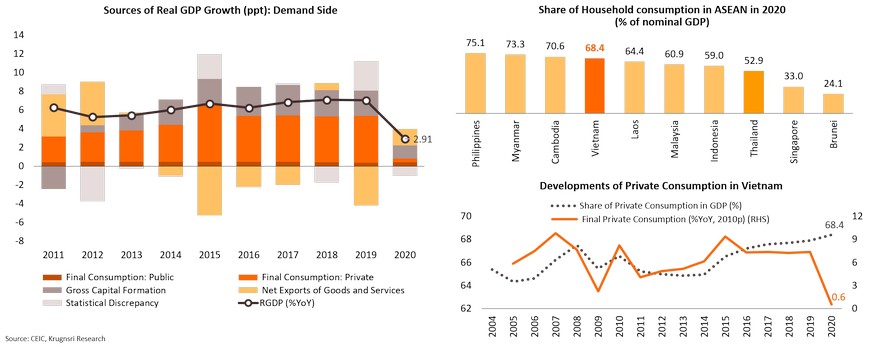

Vietnam managed to achieve positive growth rate of 2.9% in 2020, among 26 economies with economic expansion according to the IMF, despite the global adverse impact of the COVID-19 pandemic and the divergence of the global economy recovery. In 2021, the outlook is optimistic as the economy is expected to be back on its potential trajectory of 6.0% - 7.0% p.a. This will be supported by the strong performance of the manufacturing sector and exports as well as sizeable domestic demand. In the medium term, Vietnam’s high growth path will continue and the country will be the fastest growing economy in this region.

In 2021, economic activities will gradually normalize on the back of effective containment measures of the COVID-19 pandemic and the global economic recovery

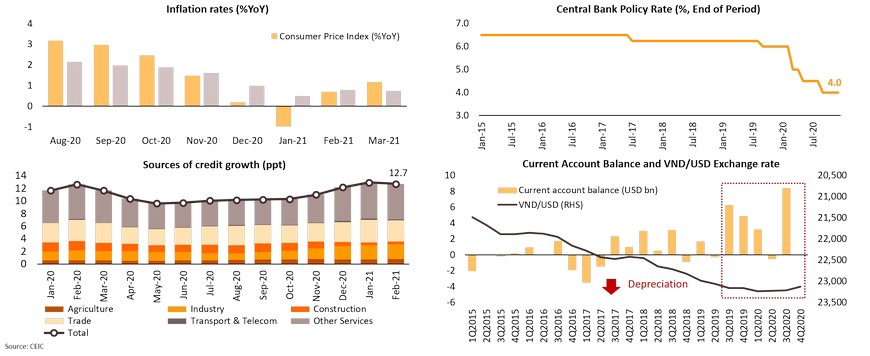

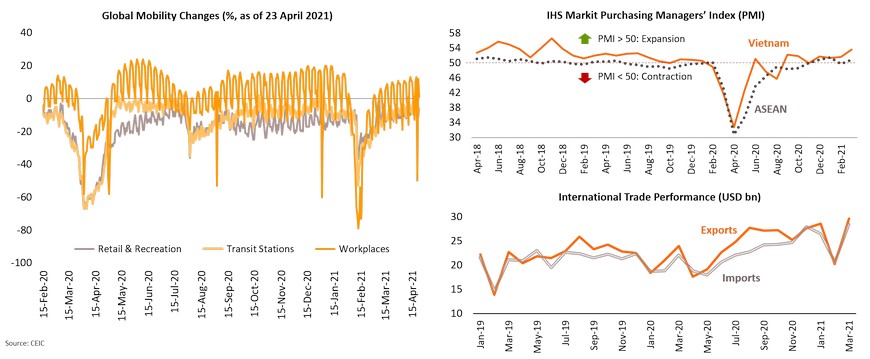

Economic activities in Vietnam have gradually normalized since the onset of the COVID-19 outbreak in 1Q2020 reflected by the high frequency data such as Google Mobility Index. This has been in line with those in the manufacturing sector gauged by the Markit PMI following its record low in April 2020. The pick up in the export and import figures also reflects the overall recovery of the economy.

Resilience in the FDI-led manufacturing sector and exports to major trading partners helps Vietnam cushion the adverse impact of the pandemic in 2020

Based on the recent available quarterly GDP data, it is obvious that the strong performance of the FDI-led and export-oriented industries dominated by consumer electronics and garments has helped weather the negative impact of the COVID-19 pandemic and sustained positive growth momentum for Vietnam. Exports to major markets have resumed following a temporary setback in 1H2020.

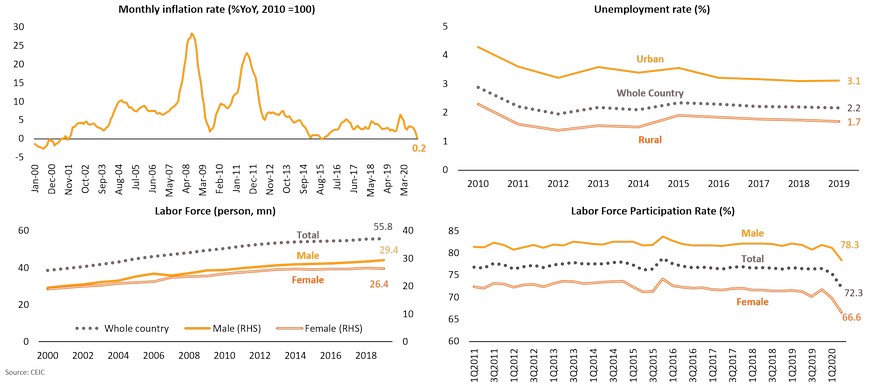

Price stability has been well maintained with a robust labor market

The annual average inflation rate has been well maintained below the annual target of 4% by the State Bank of Vietnam (SBV), the country’s central bank, over the past few years. Price stability used to be critical issues for the SBV over the past decades leading to some negative consequences such as growing dollarization or goldization – the pubic holds gold instead of local currency to protect their wealth. On the labor market, the unemployment rate has been relatively low and stable. The labor participation rate remains high.

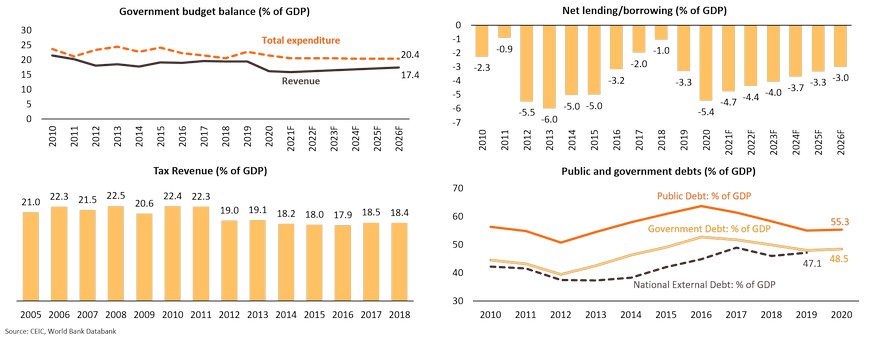

While the government has run prolonged periods of budget deficits, sustained and high economic growth ensures debt sustainability

Debt sustainability remains acceptable by international standards amid high growth prospects in the long term, while the level of public debts remain below the statutory Public and Publicly Guaranteed (PPG) debt ceiling—Vietnam’s fiscal anchor— of 65% of GDP. However, based on the IMF, it is viewed that Vietnam’s tax-to-GDP ratio is relatively low compared with that of emerging market peers; hence, fiscal consolidation is crucial to rebuild fiscal buffers and to meet public investment plans in the post-COVID periods.

On the monetary policy and exchange rate, the State Bank of Vietnam (SBV) has adopted the informal inflation targeting to preserve macroeconomic stability

Against a backdrop of low inflationary pressure, monetary policy has been accommodative to support growth. Since the onset of the pandemic, the SBV has lowered its policy rate to currently reach 4.0% p.a. and inject credits to the economy, with the target of 12% of credit growth in 2021. The VND/USD exchange rate is allowed to fluctuate within the ± 3% band. While this would ensure the exchange rate stability, the depreciation of VND is not in line with fundamentals and this could pose risks of being re-labeled as a currency manipulation by the US.

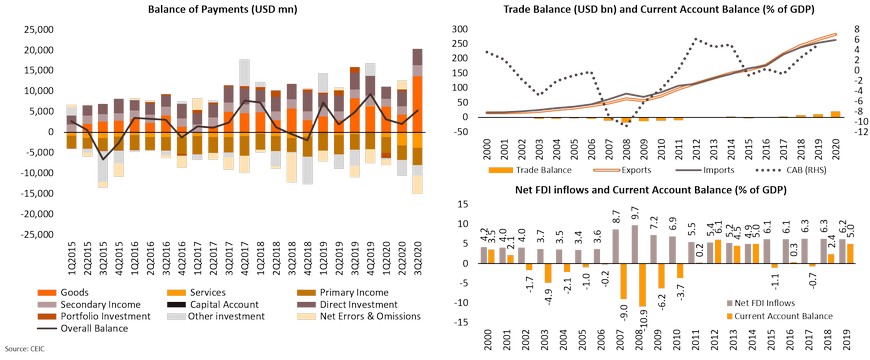

External sector stability has been resilient driven by strong exports and sustained inward FDI

External positions have been resilient supported by trade surplus and sustained direct investment flows which has been around 6% of GDP (net FDI inflows) over the past decade, while the stock of external debts is below 50% of GDP in 2019. This allows the SBV to accumulate foreign exchange reveres and build up external buffers to cushion external shocks.

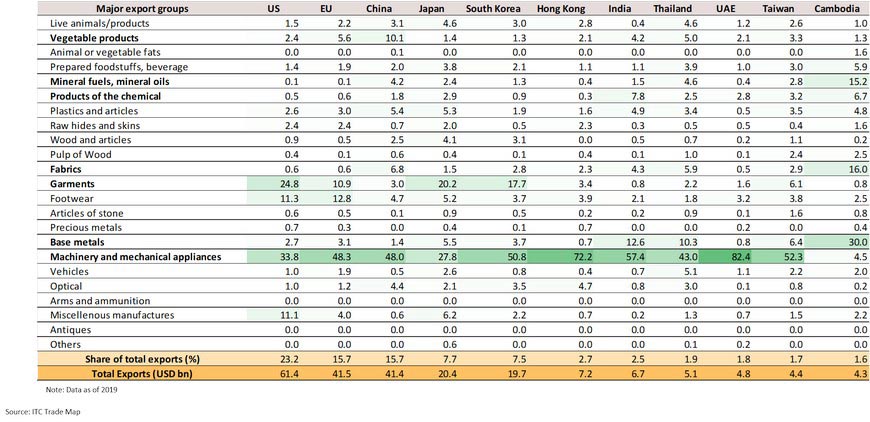

Consumer electronics and garments have emerged to be key exports driven by trade privileges and extensive networks of free trade agreements (FTAs)

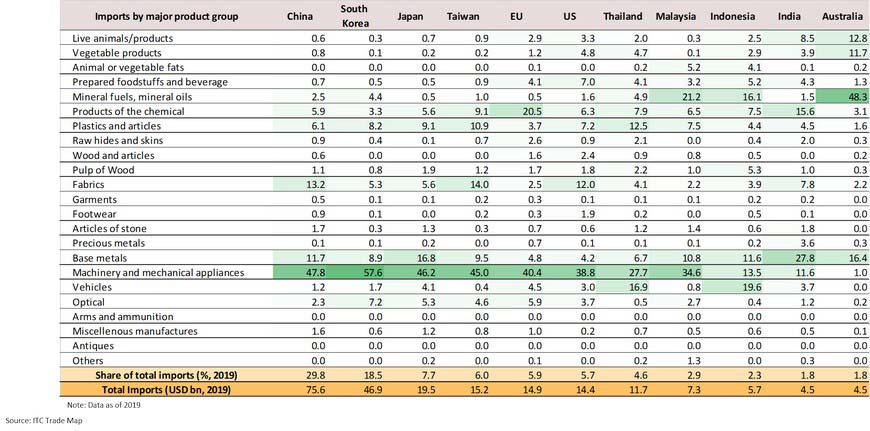

The import structure reflects the integration into regional and global value chains of Vietnam, and China has emerged as its largest trading partner

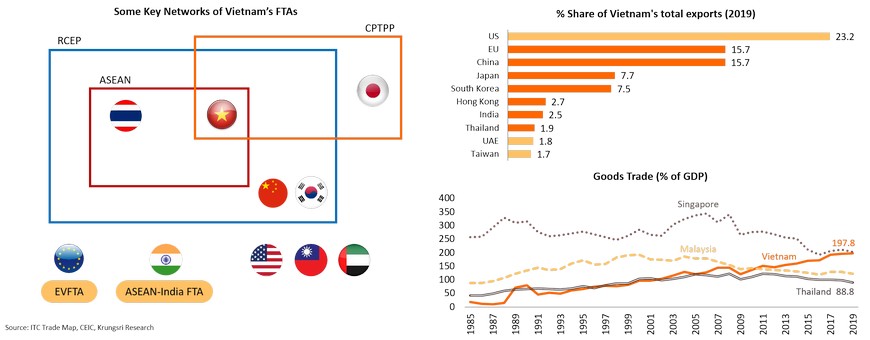

FTAs and trade preferences has paved way for Vietnam not only to gain access to major markets and attract FDI but also to help pursue domestic structural reforms

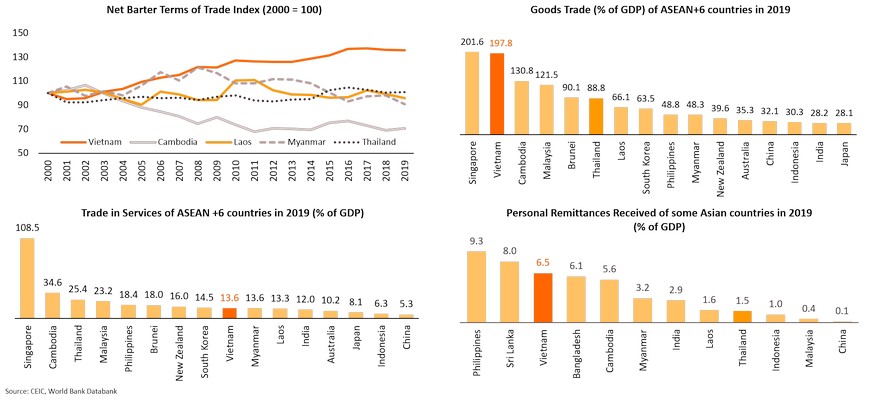

FTAs with key trading partners, whether on a bilateral basis or a multilateral basis, and to some certain extent trade preferences have boosted Vietnam’s export competitiveness in the past decade. Key trade agreements recently jointed by Vietnam include the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), the Regional Comprehensive Economic Partnership (RCEP), and the European Union Vietnam Free Trade Agreement (EVFTA). Active engaging in free trade allows Vietnam to become one of the most open economies with the share of goods trade of GDP of about 200% in 2019, close to the ratio of Singapore.

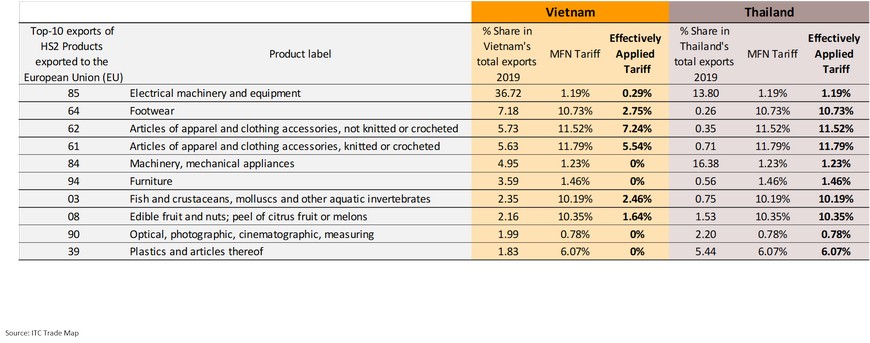

FTAs have been instrumental in boosting Vietnam’s export competitiveness, particularly in gaining access into its major markets like the EU

The table below shows the top-10 export products of Vietnam and we map them with those exported by Thailand to see whether they face the same effective tariff rates imposed by the EU, the second largest export market for Vietnam. It is clear that top-10 export products of Vietnam face much lower tariff rates compared to those of Thailand. Undoubtedly, Vietnam gains more competitiveness over Thailand in the EU market for each category of those products.

External competitiveness of Vietnam has also been reflected by sustained improvement in the terms of trade

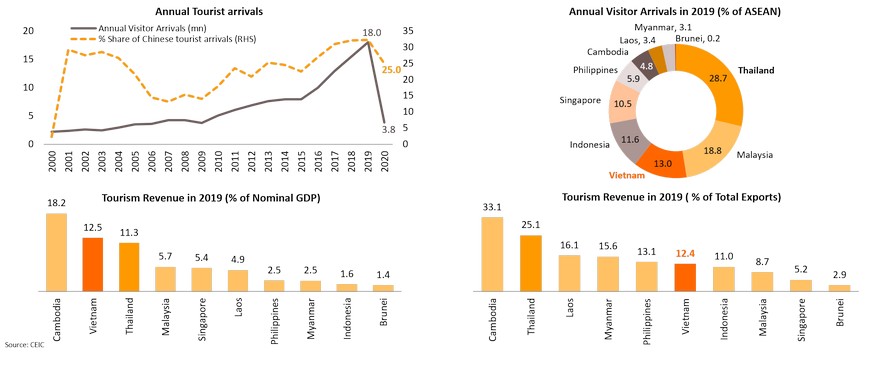

Tourism sector has turned to be another key source of foreign exchange earnings over the past decade

Prior to 2020, Vietnam has experienced booms in its tourism sector similar to regional peers. The booms have been driven by resurge of Chinese tourist arrivals which account for about a third of the country’s total annual tourist arrivals. Currently, Vietnam is the third of largest tourism market in ASEAN with the share of 13% in 2019. The tourism sector generates revenues about 12.5% of GDP in 2019 turning it to become another key source of foreign exchange earnings.

Medium-term prospects

High growth trajectory will be sustained in the long term due to favorable underlying trends

High growth of 6.0% -7.0% p.a. will be sustained, at least until 2030, owing to favorable drivers. They include sizeable and growing domestic demand, foreign investment and exports, reforms and digital initiatives, conducive business environment, as well as political stability. In our view, this offers business opportunities in the sectors such as e-commerce, financial services, healthcare, food and beverage, logistics, and education technology (EdTech).

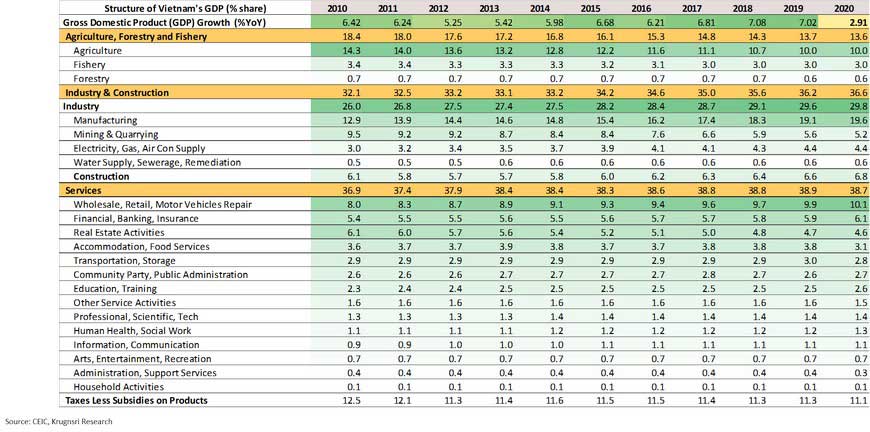

Vietnam’s economy is moving toward manufacturing and services reflected by structural changes in the GDP components

Service sector will grow substantially in line with wealthier consumers and offer business opportunities along with the robust manufacturing sector

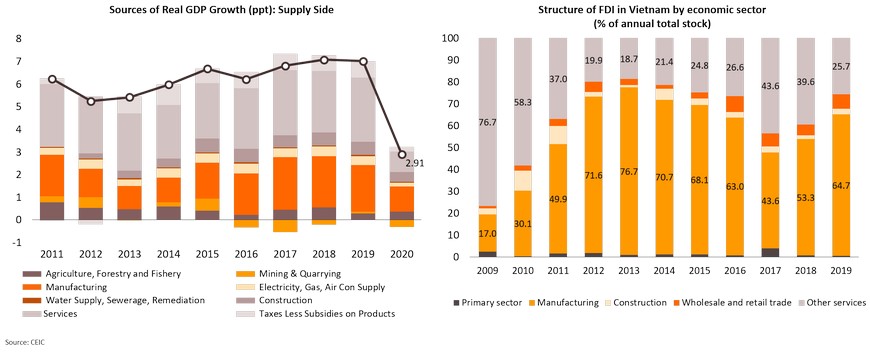

Thanks to rising labor costs, US-China trade tensions and geopolitics, as well as diversification efforts of MNCs to minimize risks of over dependence on China, there has been a great migration of some activities to south and southeast Asia. And Vietnam is currently the largest beneficiary of China’s exit from labor-intensive manufacturing activities. As a result, there are booms in export-oriented manufacturing products such as garments and footwears, and recently, consumer electronics. Manufacturing sector has been the largest recipient of FDI inflows leading to its high growth and large share in Vietnam’s GDP. On the back of growing economy, service activities such as transport, education, and healthcare, as well as ICT are among those with the highest growth rates. In our view, these will play substantial roles in Vietnam’s economy in the periods ahead.

Manufacturing sector will remain a key growth driver for Vietnam in the long term amid the expansion of the service sector

Over the past three decades since the implementation of the Doi Moi initiative in 1986, FDI-driven and export-oriented manufacturing sector has been a backbone of Vietnam’s economy and integrated the country into regional and global value chains. This development is expected to continue as Vietnam is moving up the chains of industrialization following the path of China and other advanced economies in Asia.

FDI will be attracted into Vietnam in the post-COVID era due to its favorable fundamentals

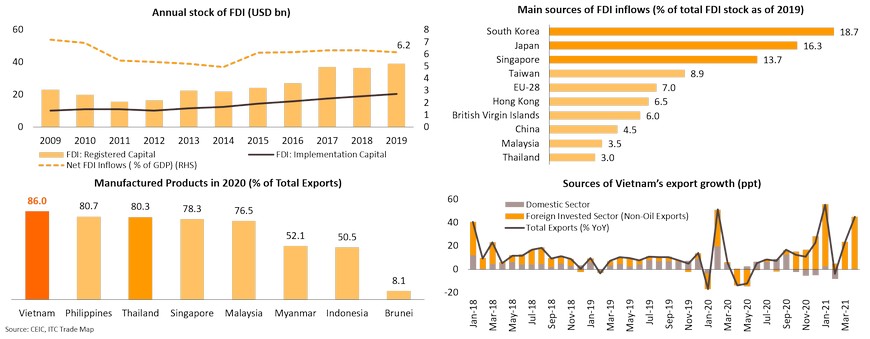

Driven by its attractive fundamentals and external developments including political uncertainty in Myanmar, foreign investment into Vietnam, particularly into the export-oriented manufacturing sector, will be continued. Over the past decades, FDI from North Asia – South Korea, Japan, and China – has played crucial roles in turning Vietnam into a mini China. Job and income opportunities have been generated leading to rising income levels of local young population. In 2020, export of manufactured goods accounts for 86% of the country’s total exports.

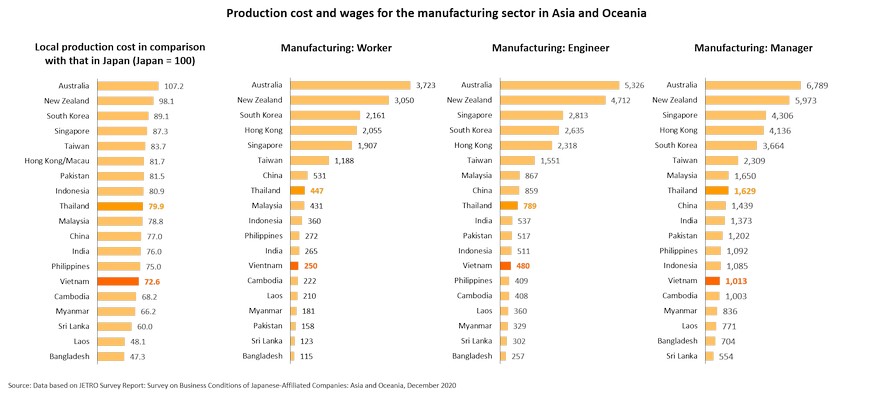

Costs of production is relatively low and provides Vietnam competitive advantage as an investment destination labor-intensive manufacturing sector

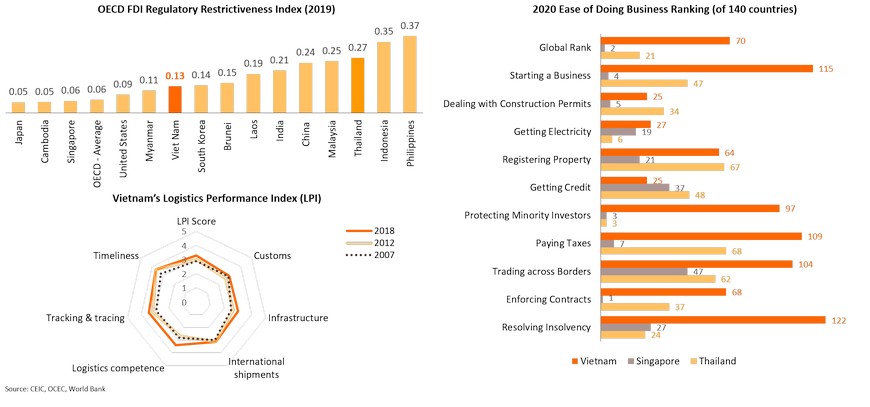

Business environment is becoming more conducive as regulatory restrictiveness has been lowered

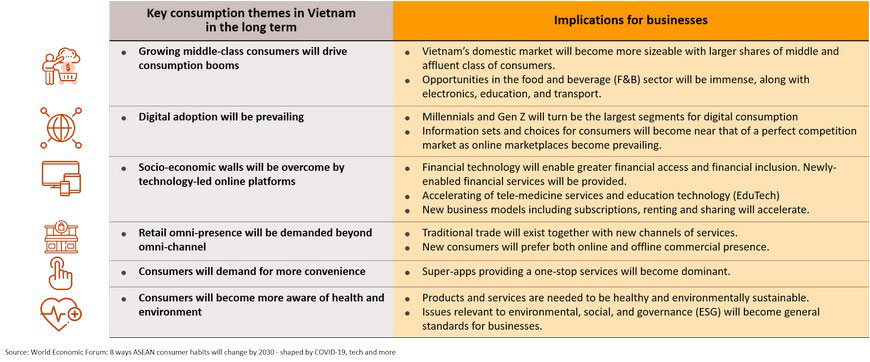

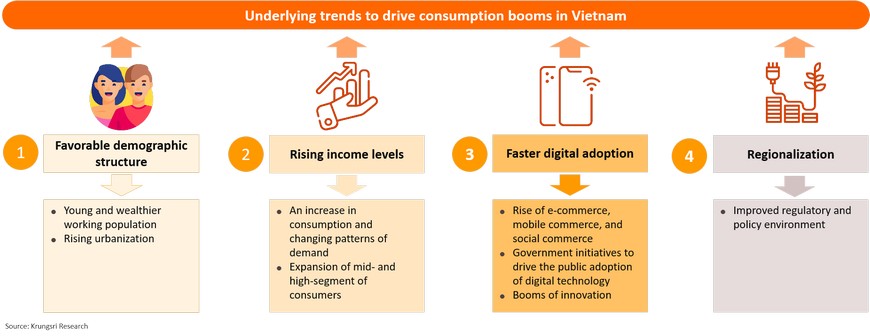

Favorable structural trends will drive consumption booms in Vietnam in the periods ahead

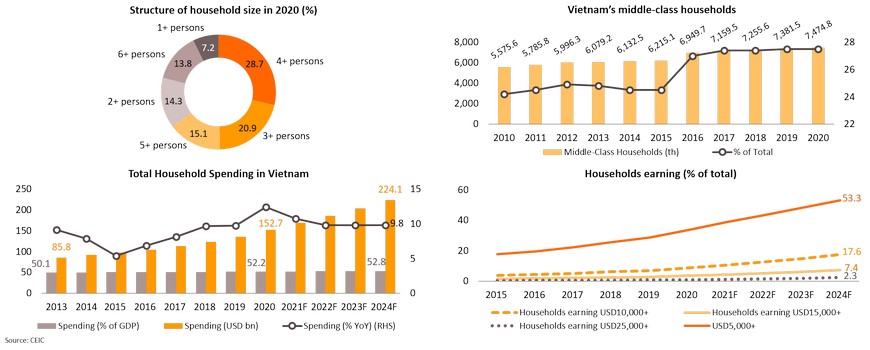

The strong economic growth over the past decades has resulted in growing middle-class consumers in Vietnam. In 2020, it is estimated that the size of Vietnamese middle and affluent class (MAC) population is around two-thirds of that in Thailand. By 2030, the number will certainly increase more than double due to sustained and strong economic expansion. On the back of demographic dividends and rising income levels, we view that faster digital adoption and regionalization will additionally boost consumption booms in Vietnam.

Vietnamese consumer behaviors are changing, and some are accelerated by the COVID-19 pandemic

New consumer habits will emerge in the post-pandemic world including those in Vietnam. In our view, there are six key themes that will shape consumption patterns in Vietnam in this decade.

Household consumption has been one of the key growth driver on the demand side in addition to export and its roles will be pivotal

With the sizeable population, about 98 million in 2020, private consumption has been the key source of growth for Vietnam on the demand side with the share of almost 70% in the GDP. Prior to 2020, growth of consumption had been robust with the average annual growth rate of about 7%. This trend is expected to continue over the long term as young population are becoming wealthier and discretionary spending is likely to rise.

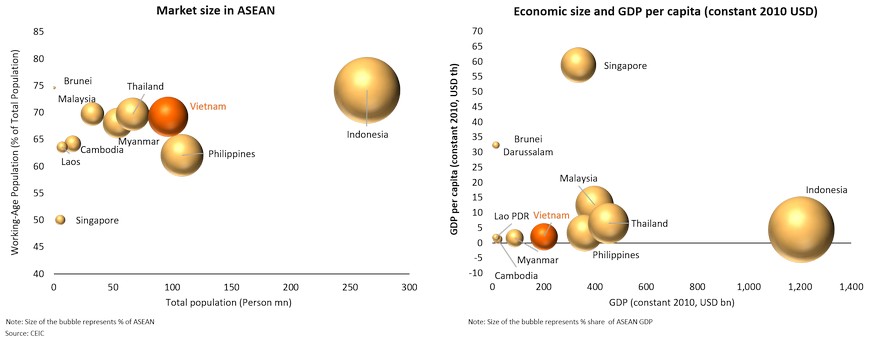

Domestic consumer market is sizeable with high growth potentials as income levels of working-age population are rising

A sizeable and growing domestic consumer market in Vietnam is attractive for not only local businesses but also foreign investors seeking growth opportunities beyond their traditional markets. Vietnam is currently the third largest economy in ASEAN in terms of population following Indonesia and the Philippines. In terms of income per capita, the country is about to catch up with ASEAN peers – the Philippines, Indonesia, Thailand.

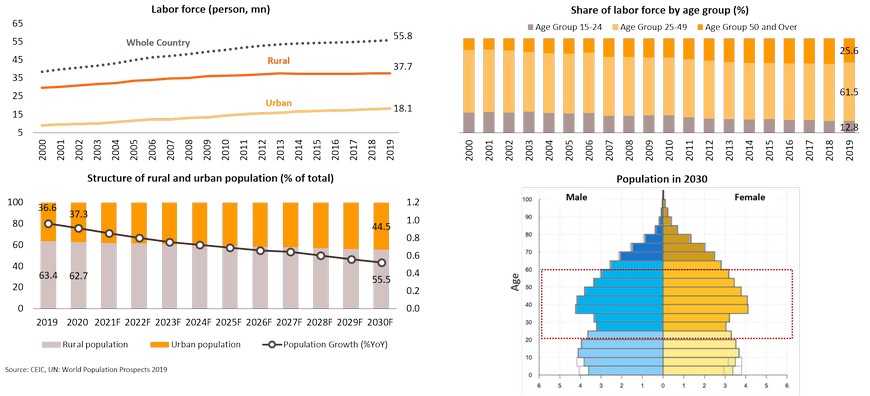

Consumption booms will be boosted by sizeable labor force and large young and wealthier population

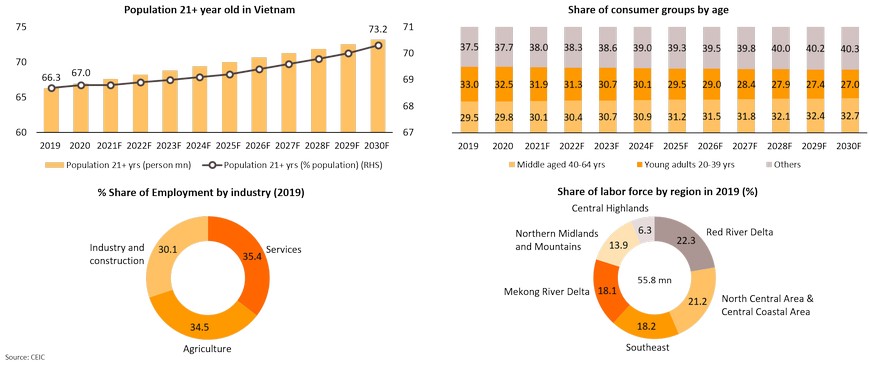

On the back of favorable demographic structure, the current labor force of about 56 million will be a sizeable group of consumers, especially young age groups of 15-24 and 25-49 amid robust economic growth and sustained inflows of foreign investment which will ensure income and job opportunities for the local. A proportion of urban population will gradually rise and by 2030, it is expected to reach 44.5% of the total population. As a result, this will shape new consumption patterns toward more urbanized modes.

Gen Z and Millennials consumers will shape consumption trends in Vietnam

By 2030, the number of population with the age over 21 will reach 73.2 million, which is larger than the population size of Thailand. And the number of new generations of consumers - Gen Z and Millennials - could account for about two-thirds of Vietnamese consumers. As a result, these groups of consumers will play roles in not only driving but also shaping demand patterns and consumption trends, especially in the urbanized cities in the Red River Delta and the Mekong River Delta, going forward.

Rising income levels will drive consumers’ discretionary expenditure

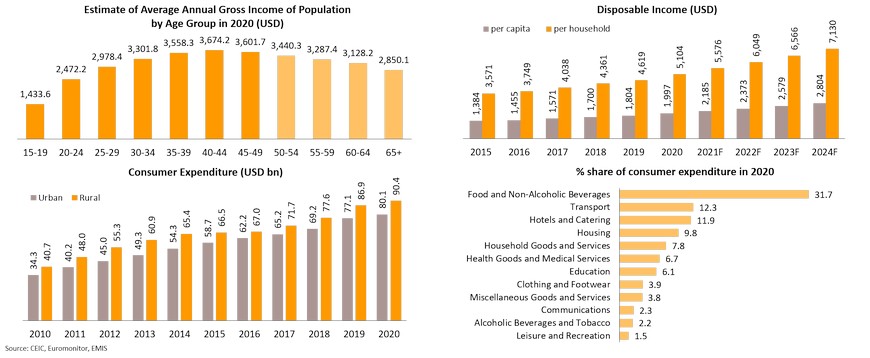

Rising income levels for all generations of consumers are the key factor behind expected consumption booms in Vietnam. In 2020, annual gross income of Gen Z and Gen Millennial consumers ranges from about 2,500 – USD3,600. By 2024, it is projected that annual disposable income per capita and per household will reach USD2,804 and USD7,1230. With higher income, consumer expenditure is rising and shares of spending on discretionary spending are expected to increase.

Size of households will be smaller in the long term driving demand for housing and other related services

Robust economic growth and urbanization trends are likely to cause changes in traditional family patterns in Vietnam amid declining fertility rates and growing international lifestyles. While the average household consists of four people, this will result in smaller size of households, for example, a couple with one child or single-person and couples-without-children households. On the back of rising household income levels and middle-class households, demand for housing and related goods and services such as consumer electronics and housing services will rise in the periods ahead.

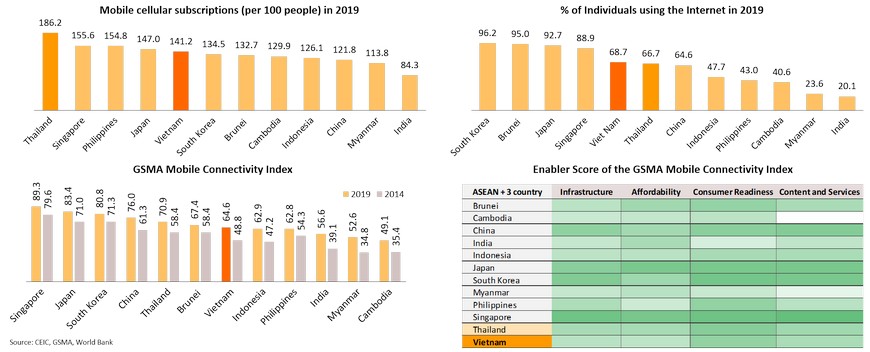

Digital economy will boom as young population tend to embrace new technologies on the back of more conducive enablers

On the back of large young and tech-savvy consumers, Vietnam has conducive and supportive for the digital economy, particularly mobile e-commerce to flourish. While the number of consumers using the internet is already on the rise, the ownership of smartphone and mobile cellular subscriptions are currently among the highest in the region. In terms of infrastructure, it has been improved considerably reflected by higher GSMA Mobile Connectivity Index. Also, Vietnam government has launched policies and initiatives to boost the digital economy including the cashless payment campaign.

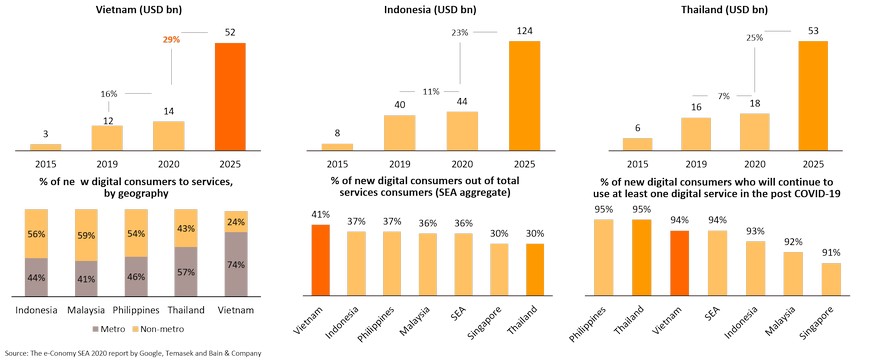

USD52bn will be the size of Vietnam’s digital economy by 2025

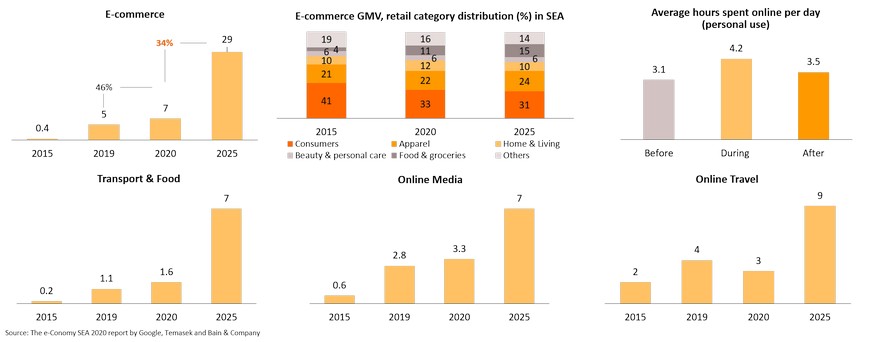

Vietnam’s digital economy will balloon to USD52bn by 2025 from USD14bn in 2020 or with the growth rate of 29%, according to the report by Google, Temasek and Bain & Company in 2020. The high growth has been primarily boosted by the COVID-19 pandemic leading to shifts in consumer behaviors to faster adopt digital services. Digital adoption happens greater in metro regions. Vietnam has the highest percentage of new digital consumers at 41% compared to that of regional peers. The digital adoption is likely to persist in the post-pandemic periods.

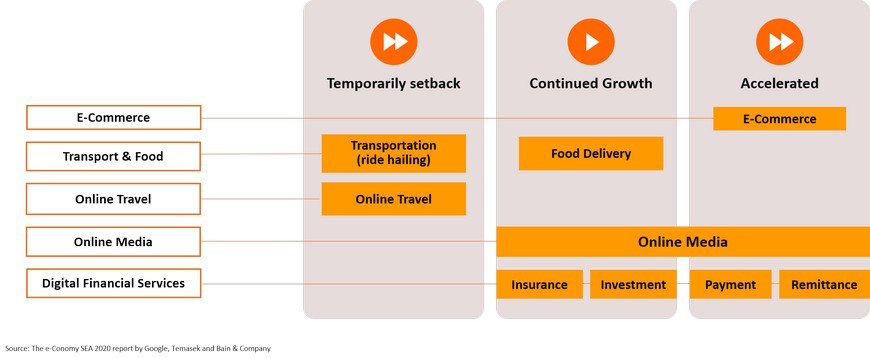

E-commerce and digital financial services will be accelerated by COVID-19 and adoption is expected to grow faster

E-commerce, especially mobile commerce, and digital financial services are among the sectors that will grow rapidly as consumers are adapting to the new normal of the post-pandemic world. While the number of the unbanked population remains large, higher adoption of digital financial services such as e-wallets and mobile money would promote greater access to financial services in Vietnam. And this will in turn fuel the growth of mobile commerce.

E-commerce market size will reach USD29bn in 2025 driven mainly by the growth of consumer products and apparels

USD29bn is the estimate of Vietnam’s e-commerce market size by 2025, which will be among the largest in Southeast Asia. Regarding retail category distribution, it is in line with the regional trends that apparel and consumer electronics/consumer products are the largest two product categories in e-commerce by value sales. This is supported by young tech-savvy consumers who are not only the most prominent online shoppers, but also the most interested in fast fashion trends and new consumer electronics products. In addition, livestream platforms/social media have been introduced by e-commerce players in to increase website traffic and consumer engagement. Thanks to the COVID-19 pandemic, the growth of transport & food, and online media will be impressive.

Exponential growth of e-commerce in Vietnam offer business opportunities within its grand ecosystem

Due to the fast and robust growth of Vietnam’s digital economy, this offers business opportunities for both local and foreign players in the country’s e-commerce ecosystem, particularly supporting activities from training to supply chain solutions as well as financial activities and financial solutions.

Political stability is secured following the recent 5-year reshuffle and policies will continue to support foreign investment

In the 1Q 2021, there was a cabinet reshuffle following the 5-year policy cycle and Vietnam is going to have new leaders. Former Prime Minister Nguyễn Xuân Phúc is now the President, and Mr. Phạm Minh Chính supersedes him as the new Prime Minister. Investors are optimistic that the new administration will pursue policies favorable to foreign investors. It is reported that the new PM will likely to focus on reviving domestic economy and tourism through a swift deployment of vaccination against the pandemic and the adoption of a vaccine passport to reopen the country. In addition, there will be fast implementation of public spending on infrastructure projects to stimulate growth and improve connectivity as well as developments of special economic zones and industrial zones across the country to boost the manufacturing sector.

Appendix: Overview of Online Behaviors in Vietnam

Overview of internet use

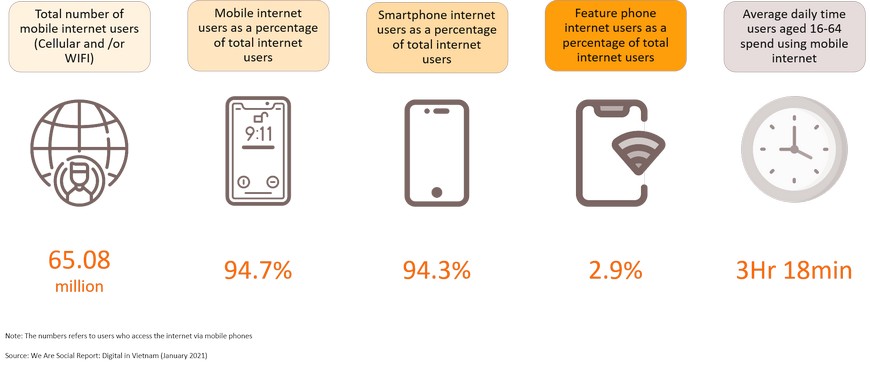

Mobile internet use

Overview of consumer goods e-commerce

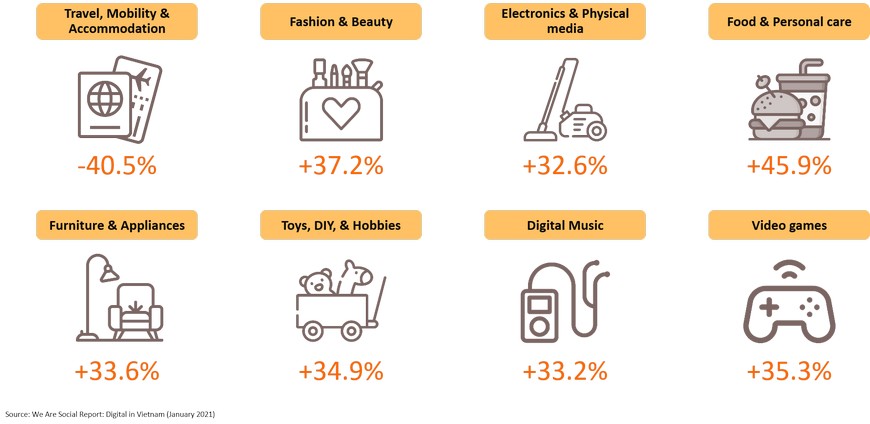

E-commerce growth by category

E-commerce purchases by age group

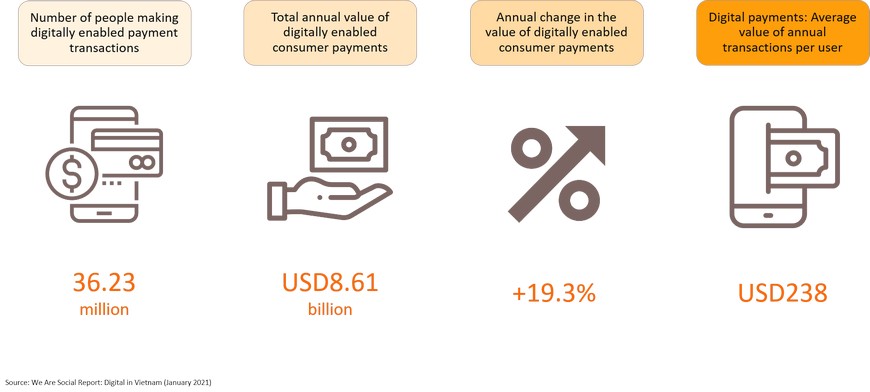

Overview of Vietnam’s digital payments

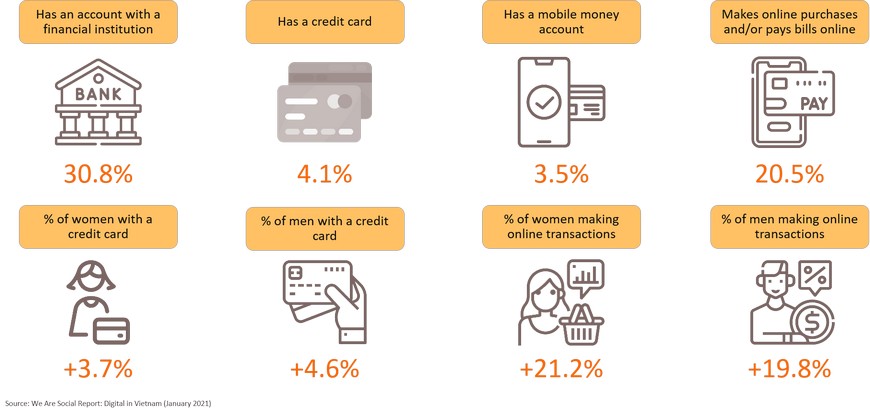

Overview of financial inclusion in Vietnam