Global: Efforts to avoid domino effect

Global activity rose for the first time in 7 months in February, supported by easing supply constraints rather than improving demand

Outlook is uncertain given transitory pent-up demand, a temporary boost from favorable weather, and impending rate-hike effects; there are signs of easing global price pressures

US: SVB collapse may not trigger a widespread contagion but would lead to tightening financial conditions and concerns of a hard landing; risks are tilted to the downside

SVB failure could deter US Fed from faster rate moves; interest rate policy should not be the appropriate tool to address financial contagion risks

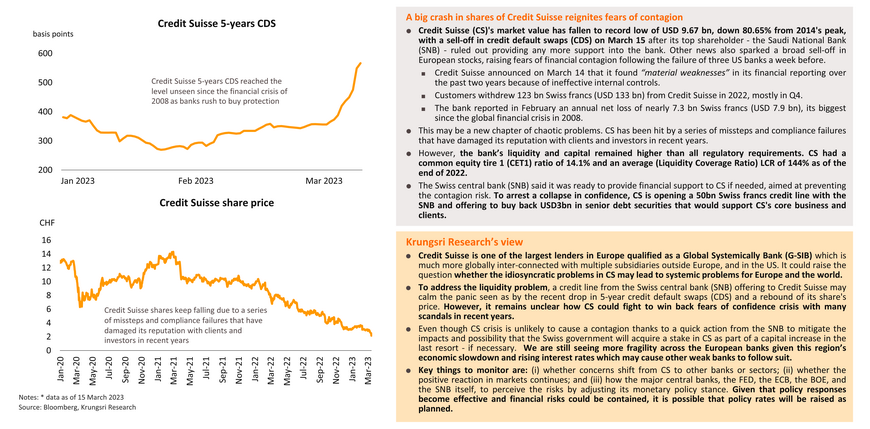

Europe: Credit Suisse reignites banking fears; recent policy response helps to address liquidity problems while confidence crisis becomes a key concern

Still-high core inflation is pressuring ECB monetary policy; Credit Suisse crisis remains a threat to financial stability

China: Recovery continues but there is lingering structural and external risks; 2023 priorities are economic stability and sustainability over rapid growth

Japan: Faster drop in real income poses downside risk to domestic consumption in 1H23

Thailand: Positive momentum but uncertainties heighten

Krungsri Research’s Forecasts for 2023: We trimmed GDP growth projection to +3.3% given disappointing 4Q22 data; still see positive growth momentum

The weaker-than-expected 4Q22 GDP data was driven by a sharp drop in exports and government spending. We revised down 2023 forecast public consumption and public investment to reflect the unwinding of pandemic-related support measures and weak 4Q22 numbers; the multiplier effect of smaller-than-expected public spending also had an impact on our forecasts. Despite the sharp drop in exports in 4Q22, we are keeping 2023 export growth forecast (only +0.5%) given lower risk of a global recession, China reopening effects, and easing global supply chain disruptions. Overall, we still see positive growth momentum this year with no signs of a technical recession in Thailand, although the sharp drop in 4Q22 GDP led us to tone down our economic growth projection for 2023. We still expect Thailand’s GDP (economic activity) to exceed pre-pandemic level this year and register stronger growth than last year.

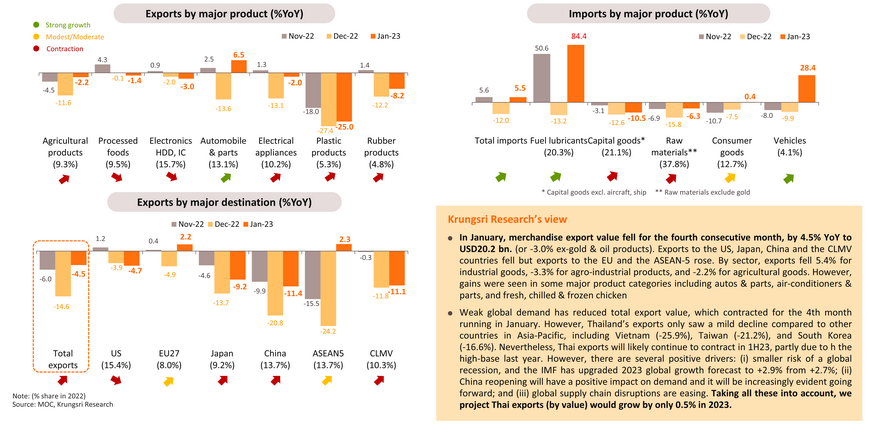

Export value dropped to a near-2-year low in January and would register only anemic growth for the year

Weak global demand caused exports from many Asian countries to tumble but easing global supply chain disruptions helped to boost exports of some Thai products

In January, exports from Asian countries, including Thailand, had dropped substantially because of slowing demand in trading partners’ economies. Looking ahead, Krungsri Research expects China reopening and easing global supply chain disruption to boost demand. In January, Thailand’s current account balance marked a deficit of over USD2 bn attributed to the trade deficit.

Manufacturing production recorded a smaller contraction due to recovering tourism and domestic economic activities

The manufacturing production index contracted for the 4th straight month in January, y 4.4% YoY. But it was an improvement from -8.5% in December. This was supported by stronger production in petroleum, automotive and food & beverages sectors and recovering capacity utilization rates to pre-COVID-19 levels. However, overall capacity utilization remained below pre-pandemic level. Although manufacturing production was hurt by weak exports, there are several tailwinds – recovering tourism activity, rising domestic demand, and ongoing general election-related activities.

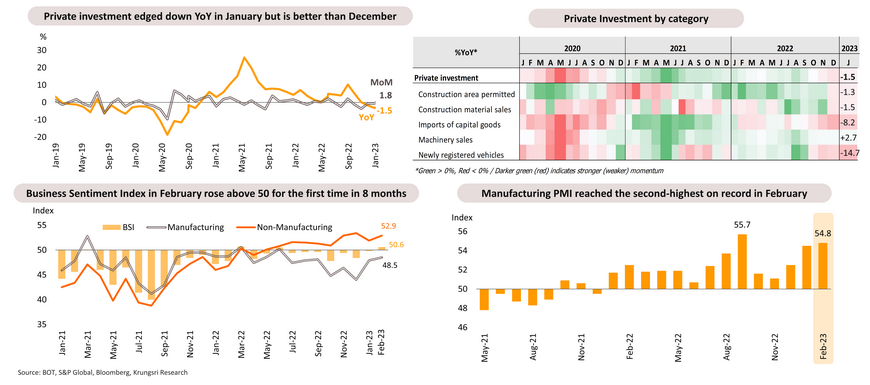

Private investment is improving along with business confidence

The private investment index remained in contraction zone for the third consecutive month in January (-1.5% YoY) as a result of weaker exports in line with slowing global demand. But there was a positive sign from February Business Sentiment which rose to >50 (improvement zone) for the first time since July 2022 and hit an 11-month high. And, February Manufacturing PMI continued to rise to its second highest on record. Nonetheless, we revised down 2023 growth forecast for private investment to +2.7% from (+3.8% previously) after factoring in the impact of delayed public infrastructure projects which resulted in a negative multiplier effect on the economy, which would lead to slower expansion of private investment in 2023.

Foreign Direct Investment (FDI) seems optimistic and would be a key economic growth driver in the medium-to-long term

In 2022, FDI poured into several sectors. The value of FDI in some sectors was greater than before the pandemic, such as in food products, rubber & plastic products, and wholesales & retail trade. This could drive private investment in the periods ahead.

Tourism sector continued to recover; rising number of Chinese and Indian tourists will drive growth in the sector in the near term

During 1 January- 3 March, foreign tourist arrivals in Thailand reached 4.53 mn and generated THB16.1 bn in tourism receipts. The number of inbound Chinese tourists has been rising to make up the 4th largest tourist group at 0.28 mn vs 91,841 in January. We expect the number of Chinese tourists to surge in 2H23, as well as from India after its government removed the requirement for pre-departure RT-PCR test for travelers travelling from or via Thailand since mid- February.

Private consumption would be encouraged by improving confidence, rising farm income, and stimulus measures

We recently revised down 2023 private consumption growth to +3.3% from our previous forecast of +3.5%. This reflects the negative multiplier effect of smaller Covid-19 pandemic-related government expenditures after the situation improved. However, private consumption will remain a key driver of the Thai economy this year. Indeed, it has continued to rise in January and the Consumer Confidence Index rose for the ninth consecutive month in February to its highest since March 2020.

Commercial banks in Thailand are resilient; limited impact from SVB and Credit Suisse

Inflation slowed faster than expected in February, suggesting the MPC might tone down rate hikes

Special Notes: Recession risk in major countries and outlook for Thai exports

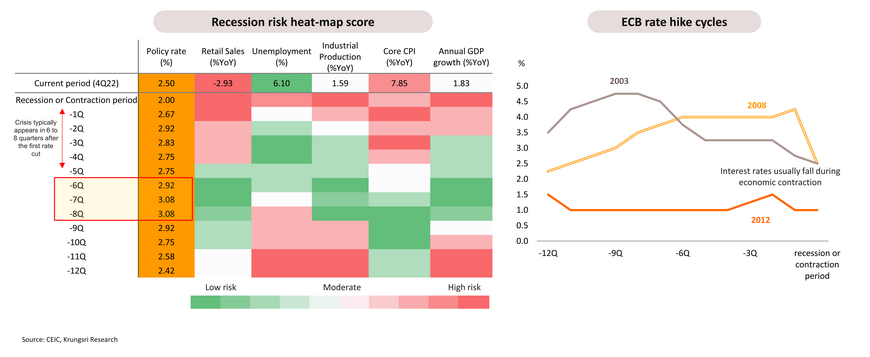

The US normally experienced economic contractions or recession following a series of steep rate hikes, and for approximately 6-8 quarters after the first rate cut

Risk of a recession in the US early this year has been lowered by recent positive data for retail sales, industrial production and unemployment rate

Compared to the economic crises in 1991, 2008, and 2002, the US economy is stronger now, premised on robust 4Q22 data for (i) retail sales; (ii) industrial production, and (iii) unemployment rate, which is at its lowest since 1969. Also, key interest rates have not peaked, with the Fed expected to raise Fed funds rate 3 more times to 5.25-5.50% this year. In past crises, after the Fed started to lower interest rates, economic contractions were spotted in the subsequent 6 to 8 quarters. So, based on the historical data, if policy rates have not peaked and the Fed has not signaled rate cuts, risk of a recession in the US should remain low.

Europe might dodge a recession in early 2023 but the road ahead remains foggy

Despite lower risk of recession, Eurozone growth could be much weaker than last year

Positive GDP growth in 4Q22 rescued Europe from a recession in early 2023. This was driven by falling energy prices, China reopening, a mild winter, and easing supply chain stress, all of which helped to improve economic activities and optimism in the region. Compared to the economic crises in 2003, 2008, and 2012, there is lower risk of a recession this year given a strong labor market (unemployment rate hit a historic low of 6.6%), positive GDP growth in 4Q22, stronger confidence, and a rebound in both the manufacturing and services sectors. However, we expect economic growth to weaken as the bloc’s latest data still show cracks in private consumption (4Q22 retail sales fell 2.93% YoY and consumer confidence fell 13.3% YoY) amid stubbornly high underlying inflation. That might prompt authorities to keep interest rates high to fight inflation and the trade-off could be a stagnant economy on the horizon. In the past, after the ECB started to lower interest rates, economic contractions were spotted in the subsequent 6 to 8 quarters (on average).

Thai exports would be supported by positive growth in global GDP in 2023, albeit it could be weaker

The IMF recently raised its global growth forecast to +2.9% for 2023, 0.2% higher than predicted in October last year, citing surprisingly resilient demand in the US and Europe and sudden reopening by China although risks remains tilted to the downside given excessive global inflation, geopolitical risks, and tighter global financial conditions. Given the elasticity of demand of Thai exports to global GDP is 1.27, every 1% growth in global GDP would boost Thai exports by 1.27%. So, with 2023 global GDP growth projected at 2.9%, Thai exports could register positive growth this year. However, the recent global rout amid SVB collapse and Credit Suisse crisis suggests downside risk to global growth and Thai exports.

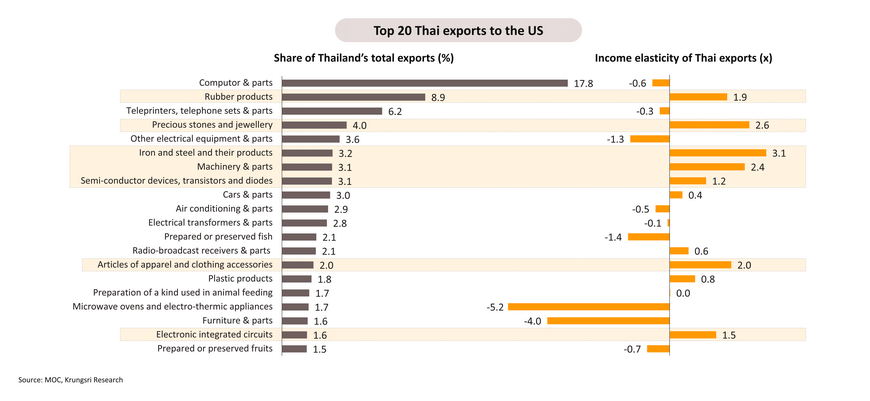

Exports to US could slow down but would not see a sharp contraction

Most of Thailand’s top export products to the US (26% of exports) show strong elasticity to US GDP growth (more than 1). They include Rubber products, Precious stones and jewelry, Iron and steel and related products, Machinery & parts, Semi-conductor devices, transistors and diodes, Apparel and cloth accessories, and Electronic integrated circuits. That means the US economic slowdown would have a significant impact on these products. Although there are expectations slower US growth would drag Thai exports this year, the overall inelastic demand (0.88) for Thai goods implies that Thai exports to the US could slow down but would not see a sharp contraction for the year.

Exports to EU remain challenging despite lower recession risk in that region

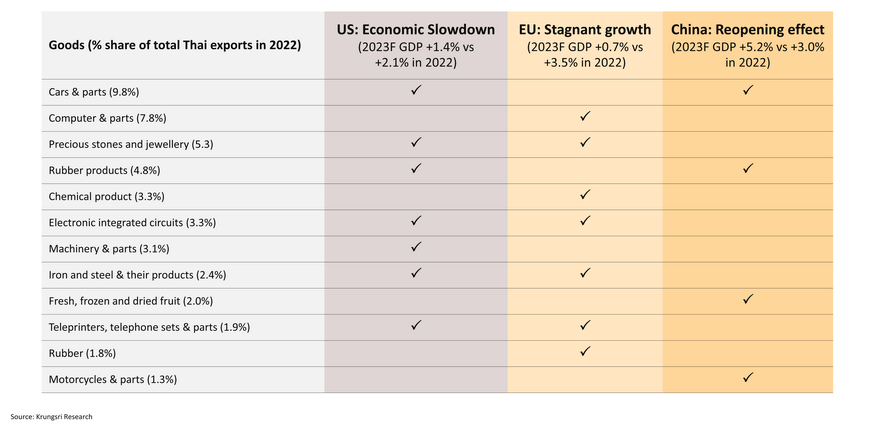

The top Thai exports to Europe (38% of exports) register high elasticity to EU GDP growth (more than 1). They include Computer & parts, Precious stones and jewelry, Electronic integrated circuits, Cars & parts, Rubber products, Electrical transformers and parts, Iron & steel and related products, Other industrial products, Teleprinters, telephone sets & parts, and Chemical products. That means a weak EU economy would have substantial impact on these products. Although there is lower recession risk in Europe early this year, stubbornly-high inflation, tightening financial conditions, and the recent troubles in financial markets will continue to cap overall economic growth. Thai exports are sensitive to EU GDP growth with elasticity of demand at 1.59, which means Europe’s market would be challenging for Thai exports in 2023.

Exports to China should gain traction led by key products, especially those high elasticity to Chinese demand

Thailand’s top exports to China (35% of exports) have registered high elasticity to China GDP growth (more than 1). They include Fresh, frozen and dried fruit, Rubber products, Copper and articles, Other agro-industrial products, Motorcycle & parts, Cars & parts, Chilled or frozen poultry cuts, Board & electric control panels, and Aluminum products. That means if there is rising pent-up demand in China, these products would be the first gain traction. However, in term of total exports or broad-based growth, China reopening will not help much as Thai exports are less sensitive to China’s GDP growth (0.52), which means a 1% growth in China GDP would boost Thai exports to China by only 0.52%.

Key export products to major markets with high elasticity to respective GDP growth (>1)

Key takeaways