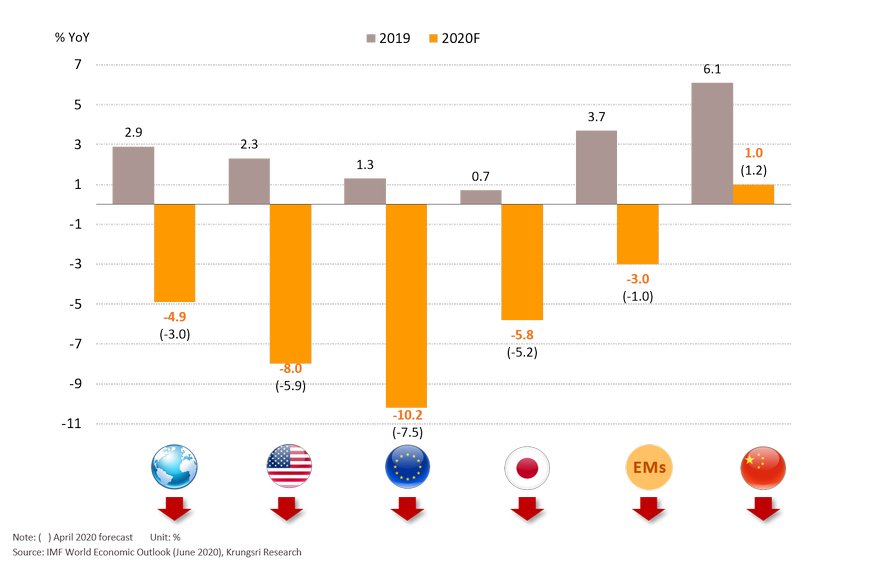

IMF slashes 2020 global growth forecast again to -4.9%, citing “a crisis like no other, an uncertain recovery”

US: Indicators show economy is improving but new cases are rising again and could lead to another lockdown

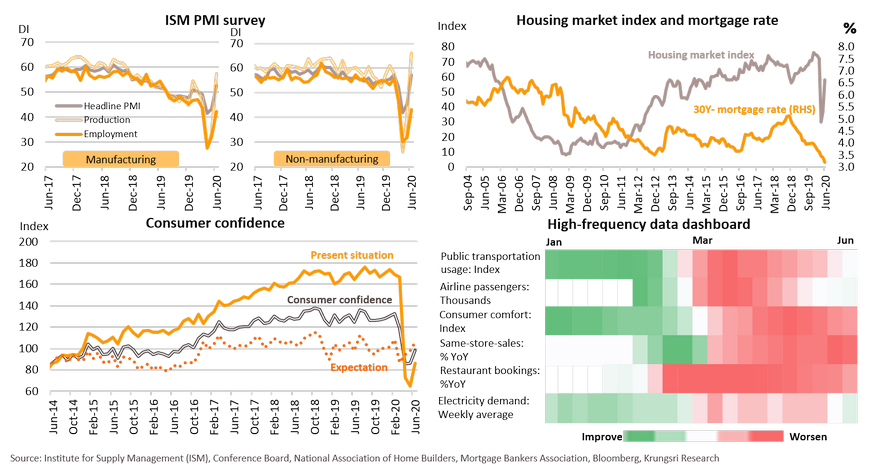

US Manufacturing PMI rose from 43.1 in May to 52.6 in June and non-Manufacturing PMI rose from 45.4 to 57.1, suggesting production activity has resumed. However, employment sub-indices for both sectors contracted for the fourth consecutive month and remain far below production sub-indices. Housing market index improved from 30 during the peak of the outbreak in April to 58 in June, with improvements in housing starts and pending home sales as 30-year mortgage rate has plunged to a new low of 3.1%. Consumer Confidence Index rose 12.2 points to 98.1 in June driven by more optimistic expectations after reopening, but the survey was conducted in mid-June, before fears of a second outbreak and another round of layoffs. On the demand side, high-frequency data show a slight improvement in public transportation, airline passengers, and electricity demand, but retail sales and restaurant bookings remain weak.

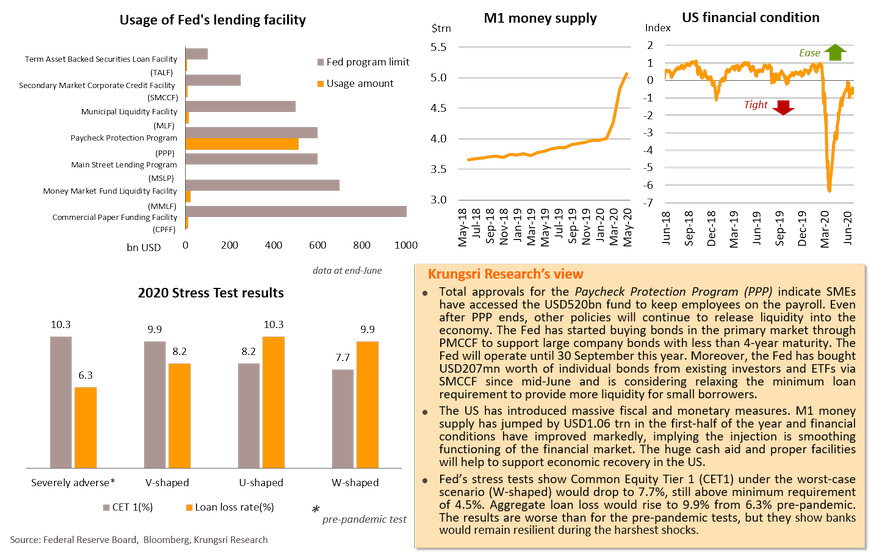

Fed’s lending facility has reached businesses; stress tests show a resilient banking sector

Unemployment, rising debts and external uncertainties could slow the pace of economic recovery

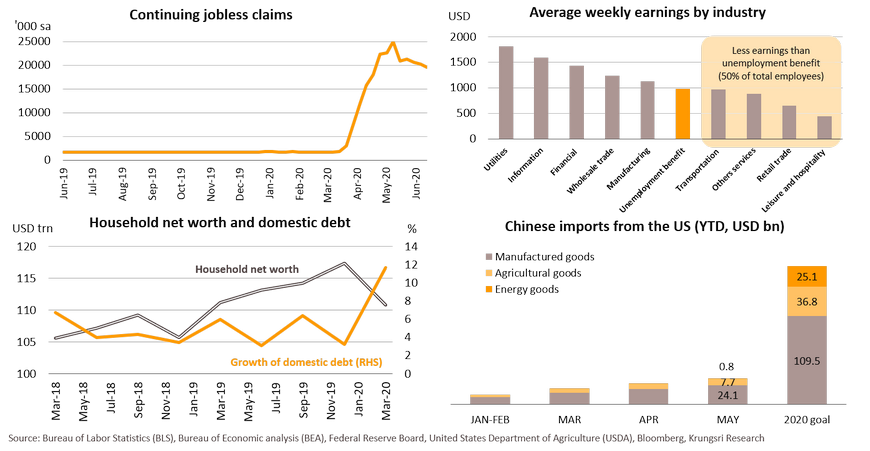

The number of jobless claims have dropped in the US but remain at a record high, with 20 million people losing their jobs and not being recalled. Unemployment benefits have exceeded the average earnings in major sectors, including retail trade, leisure and hospitality. The PPP-funded and unemployment benefit programs that will end on August 8 and July 31, respectively, could dampen recovery prospects and increase risk of a second wave of layoffs when companies run out of funds. This could reduce income and consumption substantially. Household net worth saw the largest single-quarter drop to USD100.8trn, while domestic debt surged 11.7%. There is rising external uncertainty - Chinese imports from the US in the first 5 months only reached USD32.6bn or 20% of targeted items under the deal. China needs to buy USD139bn worth of US items the rest of the year to meet its commitment. These uncertainties could pressure economic recovery. Hence, we expect more fiscal stimulus from Congress to avoid falling off the financial cliff, help the unemployed, lift market sentiment, and support a sustainable rebound in economic activities.

Europe: Activities have resumed but there are risks of a second outbreak and another lockdown

Eurozone PMI data showed a strong recovery in the Services sector, rising from 30.5 in May to 48.3 in June. Manufacturing PMI rose to 47.4 in June. PMI survey by country saw the worst contraction in April, before a marked improvement in May and June as countries eased lockdown restrictions. France is the best performing economy so far, return to modest growth with Composite PMI at 51.7, followed by 49.7 in Spain. Economic sentiment has recovered 30% of the combined losses since the peak of the outbreak, rising from 67.5 in May to 75.7 in June. Employment expectations rose to 82.8 in June but remained 40% below pre-pandemic level. Transit data show that France and German traffic activities have returned to pre-crisis levels and that the economy is recovering. These suggest economic activities have improved since easing restrictions. However, there are still risks of a second outbreak especially in Germany, Spain and Portugal, which would trigger another lockdown.

Unemployment could spike next year; government attempts to expand fiscal support

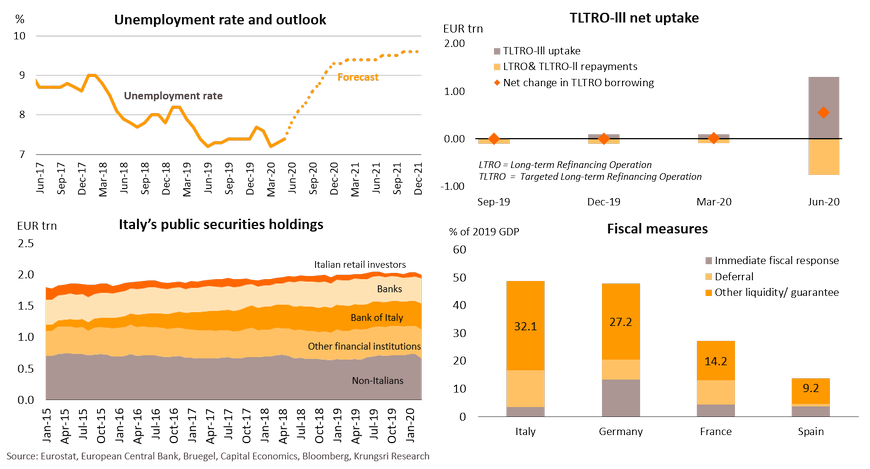

Eurozone unemployment rate only inched up from 7.3% in April to 7.4% in May, reflecting the success of furlough programs. However, unemployment could spike to over 9% next year when the program ends. This means there is a need for greater monetary and fiscal policy supports. In terms of monetary policy, net uptake in TLTRO-lll was EUR548bn in June, much higher than during previous operations, indicating stronger demand for bank lending to the real economy. In terms of fiscal support, Italy’s treasury sold EUR6.12bn (0.3% of GDP) worth of retail securities BTP futura to citizens which now own 3.1% of public securities. This would help finance the government’s economic stimulus measures. Spain is considering plans to expand its EUR100bn loan-guarantee program by EUR50bn due to strong demand from struggling businesses. Spain’s fiscal measures is relatively small compared to that in Europe’s largest economies, suggesting inadequate stimulus in some countries. The longer and larger impact of the outbreak could prompt EU policymakers to expand the stimulus program and accelerate coordinated fiscal support through the EU Recovery Fund (EUR750bn) at the July 17-18 meeting.

UK paints gloomy economic picture, and Brexit uncertainty would result in slower growth

UK GDP contracted by 2.2% QoQ in the coronavirus-ravaged first quarter, and retail sales fell by 1.7% YoY because of muted demand during the lockdown. Public sector debt reached 100% of GDP in May as tax revenue plunged and public spending surged, posing a risk to further funding to support the economy. The BOE kept interest rate at near-zero and increased asset purchases by GBP100bn at the latest meeting, but plans to slow down stimulus measures by cutting weekly asset purchases from GBP14bn in June to GBP4.5 bn throughout this year. This indicates the BOE would no longer bear additional debt created by the government and would require the public sector to finance the deficit again. On Brexit, the UK is ramping up trade negotiations after deciding not to extend the transition period, creating uncertainty in future EU-UK relations and the UK economy. A government report shows that leaving the EU would cost the UK 5% of GDP in the long term even with a free-trade agreement in place, while post-Brexit FTAs with other countries would add only 4% UK GDP. The murky picture could reduce the pace of recovery in the UK and slow its growth trajectory in the long term.

China: Improving supply-side activity indicates GDP would expand in 2Q20, investment will support a recovery

The recovering manufacturing sector indicates the Chinese economy would return to expansion mode in 2Q20. China Composite PMI data has risen more than other key countries, suggesting it is recovering faster. The official Manufacturing PMI data has been rising to reach a 3-month high in June while non-Manufacturing PMI reached a 7-month high. Likewise, the Caixin Composite PMI for June is the highest this year and stronger than the same period last year. The official new export orders sub-index for both manufacturing and non-manufacturing have improved although they remain below-50, implying lingering risk of weaker external demand. The official new orders sub-index for both manufacturing and non-manufacturing have continued to improve and is hovering in expansionary zone (above-50), reflecting stronger domestic demand. The improvement on the demand side can be observed in domestic investment as total fixed asset investment is showing signs of bottoming-out. This has been stimulated by rising public investment which registered positive growth for the second consecutive month and surged 11.4% YoY in May, the strongest growth since November 2017.

Government may ramp up investment; monetary easing gradually benefits the overall economy

The key domestic economic driver over the next period is rising public infrastructure investment, which has rise 8.3% YoY in May. That helped to boost construction activity, as reflected by the improving Construction PMI data. Infrastructure projects could generate money flows into several sectors, including 5G information technology, power lines, and intracity rail. In fact, the National People’s Congress (NPC) has set a target for special bond issuance at 4.6% of GDP or over RMB4 trn, nearly double the previous year’s volume. This implies more stimulus to boost investment further. And, China has eased monetary policy since early this year with a more targeted approach. Recently, the central bank announced it would cut both relending and rediscount rate by 25 bps to ease borrowing costs for commercial banks and boost lending to farmers and SMEs who are vulnerable to the Covid-19 impact, effective 1 July. Falling SHIBOR suggests bank lending rates could drop further. The ongoing monetary stimulus would boost liquidity and reduce borrowing costs, which would ease the debt burden and encourage more investment.

Worsening global trade and lagged improvement of labor market are key risks for economic recovery

China’s exports shrank 3.3% YoY in May, partly due to weaker world trade as a result of COVID-19 impact. May exports were partly boosted by higher demand for surgical face masks, pharmaceutical products, work-from-home-related appliances, personal protective equipment, and medical apparatus. Excluding these items, exports tumbled 12.5% YoY. In fact, those items contributed only 3% of total export value and overall external demand could remain weak, as new export orders sub-index for China PMI was still in a contraction zone. Looking at the labor market which is an indicator of the direction of domestic demand, unemployment rate edged down to 5.9% in May from 6.0% in April. Nonetheless, the urban unemployment survey did not count migrant workers. Based on the National Bureau of Statistics data (2019), there were 290.7 million migrant workers accounting for one third of China’s labor force (850.7 million). However, many migrant workers have yet to return to the cities for work. Using high-frequency data to detect daily traveling activity, only 17.6 million passengers commuted by bus and coach in June compared to 70.9 million in January, prior to the outbreak. As a result, while public infrastructure investment and construction projects would create employment, the labor market needs more time to return to normal.

Japan: Recent data show a deeper economic contraction in 2Q and a slow recovery

Japan lifted the state emergency in mid-May but domestic economic activity remains far below the pre-pandemic level. The continued drop in both industrial production (-25.9% YoY) and retail sales (-12.3%) in May points to a deep economic contraction in 2Q. Unemployment rate rose to 2.9% in May while monthly cash earnings continued to fall by 2.1% YoY, implying weaker purchasing power. In June, the Jibun Manufacturing PMI inched up to 40.1 and Service PMI rose to 45.0, but they are still in contraction territory. The 2Q20 Tankan Business Survey results also reflects worsening business conditions, which could discourage investment; the headline index has plunged from -4 to -31, the worst in 11 years since the 2009 global financial crisis. Looking forward, Japan might register a deeper economic contraction in 2Q20 and economic recovery would be slow even gradually easing restrictions. The economy would likely be depressed for at least a year because the existing fiscal stimulus packages had been late and are insufficient to boost economic growth.

Economy still lacks momentum for a recovery, and it will be a long way back to normal

In terms of monetary stimulus, the Bank of Japan (BOJ) announced in June it would ramp up the relief package by raising the ceiling for loan facilities from JPY55 trn to JPY90 trn because credit demand is escalating. In May, bank lending surged 6.2% YoY driven by tight corporate liquidity. Although the government has adopted the unprecedented fiscal stimulus, the packages only focus on relieving of negative impact on the hardest-hit segments. Most of the measures so far involved cash aid for households and firms to prevent layoffs and bankruptcies, rather than to induce and boost consumption and investment. These packages might not generate sufficient multiplier effect to shore up GDP. Moreover, the stimulus measures which started in April, were late and so were the trickle-down effects on the economy. In the June Economy Watchers Survey report, business sentiment index remained far below pre-Covid level, although it had picked up after the state emergency ended in May. Furthermore, June Tankan survey indicates wholesale and finished goods inventories are pilling up at private businesses due to weak domestic demand. Looking ahead, Japan’s economy still lacks a key recovery driver. The BOJ also indicated it might keep negative interest rates for at least another 3 years, which suggests slow recovery for the Japanese economy back to pre-COVID-19 state.

Thailand: Krungsri Research slashed 2020 GDP growth forecast to a new low of -10.3% from -5.0%

May data revealed weak consumption, investment and exports with zero foreign tourist arrivals

- Easing lockdown measures helped to nudge up confidence but household consumption and business investment continued to tumble in May. Export growth reached a 130-month low dragged by the global lockdown and demand shock. Industrial production contracted further amid rising inventories. There was no foreign tourist arrivals in 2Q20. June core inflation turned negative for the first time in nearly 11 years, implying weak demand and a need for policy support. The BOT maintained policy rates and cut 2020 GDP growth forecast, a sign to improve the effectiveness of policy transmission.

Our analysis suggests a U-shaped recovery ahead, but with higher risk of an L-shaped recovery

- Economic activity is bottoming out but there are signs of behavioral changes. Financial conditions are starting to undermine economic growth despite cutting policy rate to a new low. There is greater downside risk to the Thai economy due to delayed fiscal stimulus measures and inadequate monetary policy. Looking forward, there is uncertainty over the continuity of Thailand’s economic policy. This could lead to more business bankruptcies and and higher NPLs which could heighten risks to the financial sector and of an L-shaped recovery.

Covid-19 pandemic would shave up to 17.5 ppt off 2Q20 Thai GDP growth due to a crippled tourism industry and multiplier effect

- The Thai economy is sliding into the worst-case scenario, driven by three factors. Firstly, the global COVID-19 pandemic seems to be worse than expected as new cases continue to rise in major countries. International travel bans would be around for longer than expected. Foreign tourist arrivals into Thailand would collapse by 83% in 2020. Secondly, economic activities would decline more severely, and the negative feedback loop would be much worse than the previous projection. Workers affected by the Covid-19 impact could have reached 80% of total labor at the peak of the pandemic, and employment will remain at 30% below normal level in the last quarter of 2020. Lastly, the economic policy responses are inadequate, reflected by signs of tightening financial conditions.

Krungsri Research slashed 2020 GDP growth forecast from -5.0% to a new low of -10.3%

- The coronavirus pandemic could reduce Thai GDP growth by up to 10.6 ppt this year. In addition, delays in infrastructure investment and the drought crisis would drag GDP growth by 1.0 ppt and 0.4 ppt, respectively. The stimulus measures are estimated to add 1.7 ppt to economic growth this year. In all, we expect the Thai economy to register -10.3% growth this year (instead of -5.0%), which is worse than during the 1998 Asian Financial Crisis. This suggests Thai GDP growth (seasonally adjusted) will not recover to pre-Covid-19 level before the second half of 2023.

Recent developments: Easing lockdown measures nudged up confidence but domestic demand still tumbled

May export growth at 130-month low, dragged by global lockdown and demand shock

Industrial production continued to drop amid rising inventories and a sharp drop in imports of raw material

Foreign tourist arrivals fell by 100% in 2Q20 and would drop by 83% this year; domestic tourism is unlikely to offset that loss

Core inflation turned negative for the first time in 11 years, implying weak demand and need for policy support

BOT holds rates but cuts 2020 GDP growth projection, signals need to improve policy transmission

COVID-19 and outlook: Global cases exceed 10 million with rising risk of a second outbreak

Since the first reports of COVID-19 in December last year, the virus has spread to 213 countries and infected more than 10 million people. The number of daily new cases are still rising, especially in the US, Brazil, and India. The death toll has exceeded 0.5 million. Meanwhile, several Asian countries had managed to contain the outbreak recently but there is lingering risk of a second outbreak. Health authorities in many countries concur that there could be a second wave of infections until an effective vaccine is available or 60% of the world population has been infected (herd immunity theory). Thus, most countries remain vulnerable because there is unlikely to be a vaccine at least until the end of next year considering most vaccines are still in early trials.

Economic activity is bottoming out but there are signs of behavioral changes after COVID-19 pandemic

The global economy has begun to recover after hitting rock-bottom due to lockdown measures worldwide. Apple Mobility Index suggests people are still reluctant to travel in mass public transportation or go to public areas as the transit sub-index has not rebounded, while he driving sub-index has almost returned to pre-outbreak level. In Thailand, the economic recovery would be slow due partly to the high reliance on the tourism sector, which has been hit severely by the domestic and worldwide lockdown and fear of contracting the virus. Thailand has been recording zero or single-digit new COVID-19 cases and lockdown measures have been relaxed. However, social distancing and some lockdown measures will continue to depress economic activities.

Much weaker labor market might undermine economic recovery in the next period

Current stimulus might be insufficient to weather the crisis and there is rising uncertainty over policy continuity

The THB435bn cash aid has been injected into the economy while only THB15.5bn worth of projects (out of a total budget of THB400bn) to boost economic activity has been approved. And the BOT has disbursed only THB95.8bn of its THB500bn soft loans program. The current pace of liquidity injection into the system might not be large enough to boost domestic spending and investment. The delays and insufficient economic policies could slow the pace of economic recovery. There is also uncertainty over the continuity of economic policy given risk of a cabinet reshuffle.

Financial conditions are starting to undermine economic growth despite cutting policy rate to a new low

Financial conditions in Thailand have been easing by a smaller quantum in 1Q20 even though the Monetary Policy Committee (MPC) had reduced policy rate to a record low. Meanwhile, the financial accelerator has risen steadily over the last few quarters. That implies financial conditions are tightening, which could undermine economic growth and increase risks to the overall economy.

Greater downside risk due to slow policy response and inadequate stimulus measures

Looking ahead, there is greater downside risk even though new COVID-19 cases have peaked in several areas. An economic recovery would depend on the effectiveness of policy response. Thailand’s fiscal policy response have been slow. Monetary stimulus measures have been insufficient and not expansive enough to improve liquidity in the economy and financial system, as financial conditions are starting to undermine economic growth. This could lead to more business bankruptcies and rising NPLs, which will heighten risks to the financial and banking system.

Our analysis suggests a U-shaped recovery ahead, but with greater risk of an L-shaped recovery

Even though the number of new cases in Thailand had peaked in 1H20, the slow and inadequate economic policy responses to battle the COVID-19 crisis would have persistent and substantial impact on the Thai economy. Both the real economy and financial sector would be badly hit, and increase risks of a financial contagion which could lead to an L-shaped recovery.

Thailand might be among the hardest-hit by the coronavirus pandemic

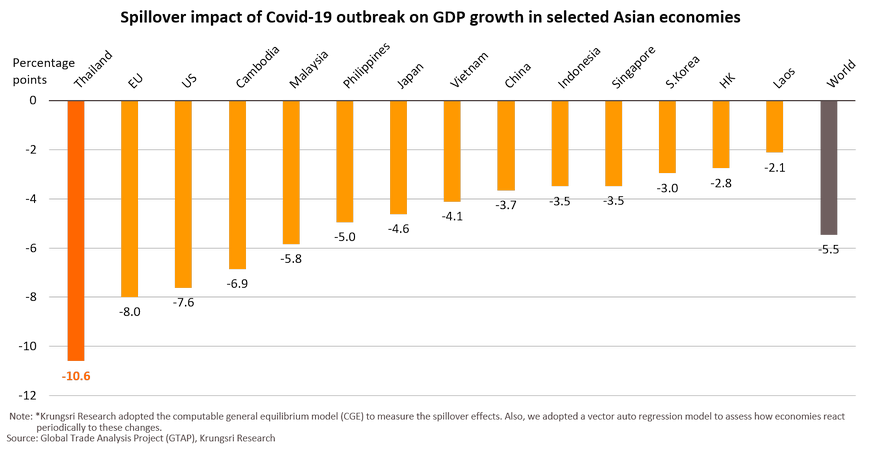

Despite easing restrictions after a two-month lockdown, the Covid-19 pandemic in several key countries and continued social distancing measures would reduce global GDP growth substantially by 5.5 percentage points (ppt) from pre-outbreak level. The pandemic is likely to hit the Thai economy more severe than we previously expected. Krungsri Research now projects the Thai economy would be among the hardest hit, followed by the EU, the US, and Japan. Although the number of new cases in China has started to slow, new cases are still rising in several other key countries. This means worldwide travel restrictions would not be lifted soon, including bans on inbound international flights in Thailand and most countries worldwide. On this note, we estimate Thai GDP would be hurt through the following channels – tourism, supply disruption at home and abroad, and multiplier effect.

Pandemic could slash Thai GDP growth by up to 17.5ppt in 2Q20 due to multiplier effect and stalled tourism industry

The Thai economy is sliding into the worst-case scenario, dragged by three factors.

- First, the global COVID-19 pandemic is more severe than previously expected as new cases continue to rise worldwide, particularly in the US, and has re-emerged in key countries such as China. This means international travel bans will not be lifted so soon. Foreign tourist arrivals in Thailand is projected to collapse by 83% in 2020 (instead of our earlier forecast of -60%). This means there will be almost zero foreign tourist arrivals the rest of the year. The number of tourists under the potential travel bubble scheme would account for less than 1% of last year’s total foreign arrivals.

- Second, economic activities would decline more severely, and the negative feedback loop would be worse than our previous projection. Workers affected by the Covid-19 impact are now estimated to reach 80% of total labor at the peak of the pandemic (vs 50% in the previous forecast), and employment would remain at 30% below normal level in the last quarter of 2020 (vs 10% in the previous forecast).

- Lastly, the economic policy response has been inadequate because financial conditions have continued to tighten.

Our findings suggest the adverse consequences would be worst in 2Q20 but the extended containment measures will cause increase the negative multiplier effect. The Covid-19 pandemic would reduce 2020 Thai GDP growth by 10.6 percentage points (ppt) from baseline with a 17.5ppt decline in 2Q20. The most severe impact in 2Q20 would come from the multiplier effect (-5.8ppt), followed by tourism sector (-5.5ppt), domestic supply disruption (-3.9ppt), and global supply disruption (-2.2ppt). In the second half of the year, even if the worst has passed, there would still be some scars on the Thai economy. Weak sentiment and the remaining containment measures would continue to hurt the tourism sector and the negative multiplier effect would continue to harm overall economic activity.

Krungsri Research has slashed 2020 GDP growth forecast from -5.0% to a record low of -10.3%

- Despite almost-zero new cases in Thailand and easing lockdown restrictions, the pandemic could reduce Thai GDP growth by up to 10.6 percentage points (ppt) this year as continued social distancing and remaining containment measures will hurt the tourism and related sectors harder and longer than we had expected. High unemployment and rising household and business debts would amplify the negative income effects for an extended period. And when supportive measures end, there is is risk of a second round of layoffs and the debt cliff could worsen the vicious cycle between confidence and economic growth.

- Delays in infrastructure investment and drought crisis would reduce GDP growth by 1.0 and 0.4 ppt, respectively.

- Stimulus measures might add only 1.7 ppt to economic growth this year. However, fiscal measures and monetary easing would likely be insufficient to fend off an economic recession and to encourage household spending and business investment.

To conclude, Krungsri Research slashed 2020 GDP growth forecast from -5.0% to -10.3%, worse than the 1998 Asian Financial Crisis. Thai GDP growth (seasonally adjusted) would not recover to pre-Covid-19 level before the second half of 2023

Krungsri Research Forecast

ASEAN expects to sign the RCEP by November; this would strengthen intra-Asia trade and investment relations

- At the 36th ASEAN Summit in June 2020, the ASEAN and its five partners – China, Japan, South Korea, Australia and New Zealand – have planned to sign the Regional Comprehensive Economic Partnership (RCEP) agreement by November. India had participated in initial talks but withdrew from the deal in November 2019.

- The 15 participating countries account for almost half of the world’s population and contribute 30% of global GDP and about a quarter of global exports. Since the ASEAN and the five partners opened up their markets under the ASEAN Plus scheme in 2010, several countries have seen a significant increase in trade with RCEP countries, especially Myanmar, Philippines, and Cambodia. And, the combined value of FDI from the RCEP participating countries accounts for more than a half of each countries’ FDI.

- We are optimistic that the RCEP will bring more significant benefits to the signatory countries, by expanding trade and investment opportunities across the Asian region. It will not only allow member countries easier access to this large market, but ASEAN countries could also integrate deeper with the global value chain. Although there may be limited additional benefits from a tariff reduction under the prevailing ASEAN Plus trade pact, they are expected to gain from the more flexible Rules of Origin (RoO) to reduce implicit costs in the supply chain, which would facilitate easier trade. In addition, the RCEP will also encourage more significant bilateral FTAs between members, for example the China-Japan and Japan-South Korea FTAs. This would enhance economic development in the region. In addition, the pact would also lure more investment from the RCEP partners through a more relaxed investment environment and strengthen investment relations between member countries.

Manufacturing activities show signs of early-stage recovery; Vietnam has shown strongest improvement

- Following the easing lockdown measures, production activities in ASEAN countries registered broad improvements in June, although the indices remain in contraction territory. The exception was Vietnam, the only ASEAN country to register an expansion in the Purchasing Manager’s Index (PMI). The improvements in Manufacturing PMI are also in line with retail sales trends in the respective countries.

- Given a deeper-than-expected global recession, external demand should contract this year and dampen prospects for trade-dependent SE Asian economies, especially Vietnam and Cambodia which trade value accounts for over 200% and 130% of GDP, respectively.

- This will continue to deter manufacturing activities across ASEAN. Given the SE Asia nations’ manufacturing sector employs 20-25% of the total labor force in the respective countries, the weak recovery in manufacturing activities would drag household spending the rest of this year, especially in countries with still-fragile domestic consumption like Indonesia and Philippines. Retails sales in both these countries have tumbled in recent months amid extended lockdown measures.

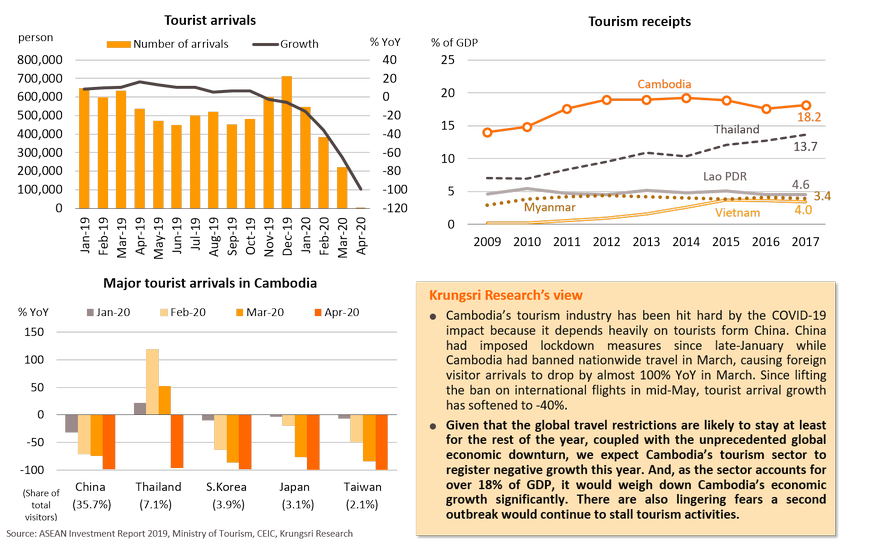

Cambodia: Tourist arrivals will tumble in 2020 given restrictive measures and global downturn

Myanmar: Macroeconomic stability remains weak although FDI inflows would reduce the pressure.

Myanmar’s core inflation remains high at about 13% YoY, which reflects still-high cost of living amid lower income. The Covid-19 impact could widen the country’s trade deficit. Myanmar’s exports would drop further because of weak global demand, while imports are expected to recover gradually (but continue to post negative YoY growth) led by the resumption of construction activities. This would result in a still-large current account deficit (CAD), which would, in turn, put downward pressure on the MMK which is currently stable. However, the continued growth in FDI inflows would partly help finance the CAD and reduce pressure on external stability.

Lao PDR: March trade data show pandemic impact; expect further trade deficit to worsen

Vietnam: Investment should improve in 2H20 because the EVFTA would attract more FDI

Indonesia: Government and BI agree on USD40bn burden-sharing scheme, the largest monetization program in ASEAN

May retail sales post largest drop since 2008; expect domestic consumption to deteriorate further

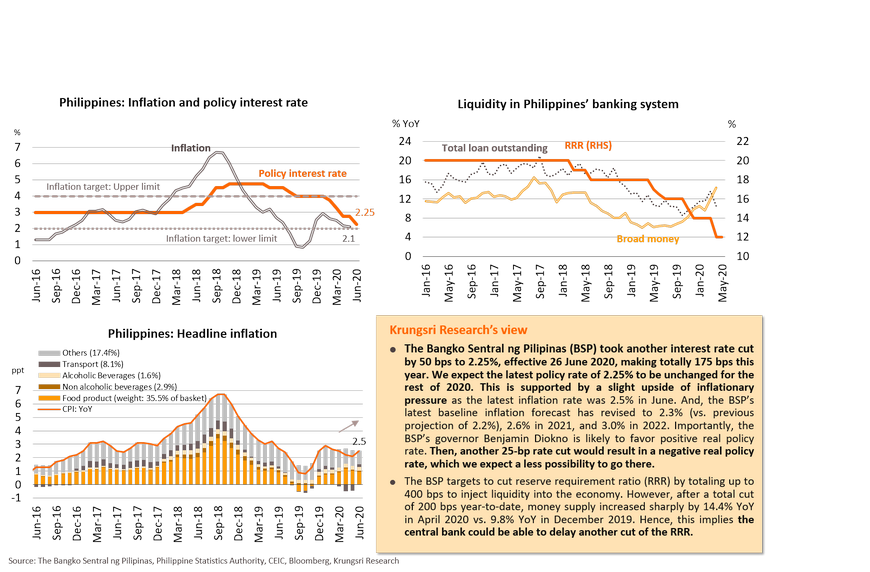

Philippines: After delivering deep interest rate cut by 175 bps, BSP would keep its key rates as it prefers positive real rate